Global| Dec 29 2017

Global| Dec 29 2017Italian Confidences Hold Strong at Yearend and 2018 Beckons

Summary

The Italian bond market sold off in end of year trading as Italian investors began to think ahead to 2018 elections. Silvio Berlusconi is in the news again and extoling the virtues and standing of his party as the main rival to the [...]

The Italian bond market sold off in end of year trading as Italian investors began to think ahead to 2018 elections. Silvio Berlusconi is in the news again and extoling the virtues and standing of his party as the main rival to the Five-star Movement. Welcome to the new worries of 2018 in 2017.

The Italian bond market sold off in end of year trading as Italian investors began to think ahead to 2018 elections. Silvio Berlusconi is in the news again and extoling the virtues and standing of his party as the main rival to the Five-star Movement. Welcome to the new worries of 2018 in 2017.

There is no doubt that 2018 will bring some different stresses to the table than 2017. And if you are running a mile on an oval track, the second 440 yards is different from the first 440 yards but they are all part of the same journey and is track you been over before. I think we can oversell the extent to which 2018 will be different. Some of it will be different in a trivial way. How much of it will be different in an important way?

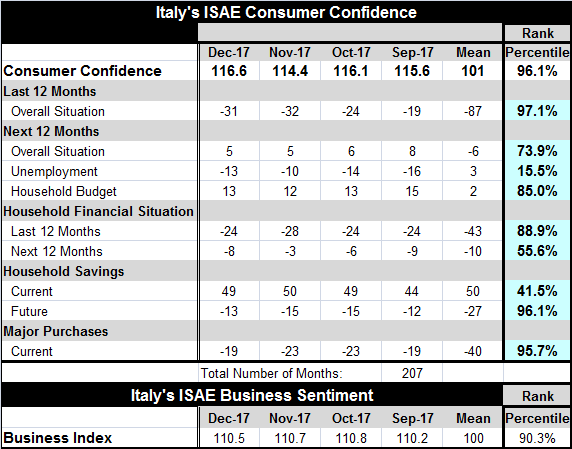

The surveys for Italy show that consumer and business confidence both are strong at yearend. However, the ranking of the past 12-month overall situation has a 97th percentile standing and the ranking for the next 12-month overall situation has only a 73rd percentile standing. Fears of unemployment, however, continue to fade as the unemployment prospect gauge has been lower only about 15% of the time. Households rate their budgets as being in this strong shape or better only about 15% of the time.

Despite that, households rate their financial situation over the last 12 months with an 88th percentile standing. Looking ahead to the next 12 months, the financial situation drops to a 55th percentile standing - a big difference and downgrade. The environment to make major purchases has been better less than 5% of the time and that reading has been moving up strongly in recent months including this month.

Italian consumers have somewhat mixed assessments of where they are and where they are going. But overall the scores in the confidence survey seem to tick the right boxes and nothing important is truly weak- just somethings are less strong than they were over the past 12 months. And importantly the big fear of unemployment is really being pushed to the background. Italian business confidence jumped in September to 110.2 from 108.4 after beginning the year at 105.1. But since that September jump, business confidence has moved mostly sideways, holding gains but not extending them.

But things are changing for 2018 in the EMU. Italy will have elections. Catalonia is preparing a new parliament in Spain. Today's data showed less of a drop in German inflation and not surprisingly we will hear more of Germans complaining about inflation as their own home inflation rate rises faster since it has the most overheated economy in Europe. Still, EMU conditions are simply not that strong. Hopes are high for growth acceleration in the U.S. and President Trump is cheering on the optimism, but the U.S. lacks some important ingredients for growth to step up. Better-paying jobs still are not being created. Jobs are plentiful, but they are not high-skill jobs. And the consumer savings rate is depressed as 2017 draws to a close, something that will make it hard- if not impossible- for spending in the U.S. to outgrow income.

The geopolitical scene is unsettled with Russia unhappy that Japan is bolstering its missile defense system and also unhappy that the U.S. is selling some upgraded armaments to Ukraine. The U.S. has accused China of making illicit oil sales to North Korea. Palestinians are protesting Donald Trump's recognition of Jerusalem as the capital of Israel, a position that has left the U.S. isolated internationally. The oil markets are still unstable as fracking in the U.S. progresses. The future is less certain than markets seem to pretend. All continents face new risks or the extensions of the risks they avoided last year. The economy's path is still uncertain, but the path of policy as 2018 begins is quite certain as central bankers largely have made their choice. Are they the right ones?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief