Global| Feb 24 2017

Global| Feb 24 2017Italian Confidence Registers Split-Decision

Summary

Confidence measures 'go their own way' but wind up in the same place In February, Italian consumer confidence trolled a five-month low while business confidence perked up. At the end of the day, both confidence indexes sit in their [...]

Confidence measures 'go their own way' but wind up in the same place

Confidence measures 'go their own way' but wind up in the same place

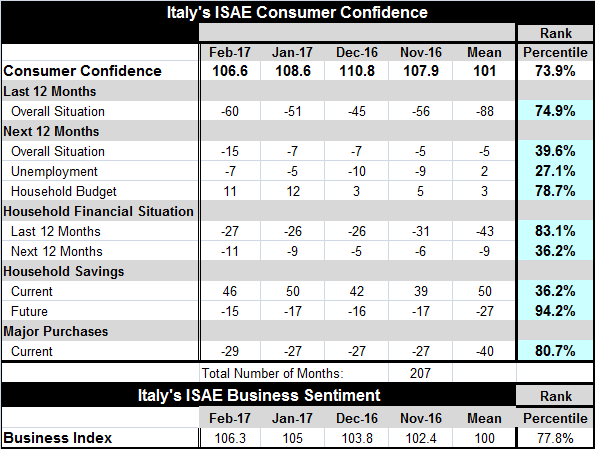

In February, Italian consumer confidence trolled a five-month low while business confidence perked up. At the end of the day, both confidence indexes sit in their respective 70th percentile deciles with consumer confidence at its 73.9% queue standing and business confidence at its 77.8 percentile queue standing. The momentum for the two series is different, but the levels of contentedness being experienced by Italian businesses and consumers are roughly similar and basically quite comfortable.

Momentum disparities nag

However, momentum is always something to worry about since what consumers feel today could be a passing fancy. Consumer confidence has risen quite a bit more strongly than business confidence since mid-2014, but it reached its pinnacle then came off just as fast as it had risen. In 2016 the winding stopped and consumer sentiment had a brief rally, but now it is weakening again. While consumer confidence was experiencing that wild and woolly ride, business confidence was more or less steady and now both indexes find themselves at similar relative readings.

Good performance...considering

All these machinations are important since Italy is still a troubled economy. It continues to battle to keep its budget deficit in line with EU mandates; its banking sector is weak and still in need of more capital infusions; and the Five Star Movement, a political movement that controls several large Italian cities, has gained momentum at a time that the Italian government is again on shaky ground. While surveys of the Italian people usually find that people do not want to exit the euro area, doing just that is one of the planks of the 'Five Star' platform. With so much turmoil in their political and everyday lives as well as the presence of a shaky banking sector, it is surprising that consumer and business confidence hangs in there so well.

Consumer confidence

The consumer confidence gauge dropped to 106.6 in February after falling to 108.6 in January. However December had marked a pick up, so while we have several months of decline on our hands with this report, it is not simply falling-out-of-bed. The overall gauge sits at the 73.9 percentile of its historic queue of data, marking the reading as higher about 26% of the time- a reasonably firm position nested near the upper quartile of its historic queue of values.

The overall situation for the past 12 months deteriorated in February from January, falling to a -60 reading from -51 previously. This left the index standing in its 74th percentile. Looking ahead to the next 12 months, the overall situation is assessed at a -15 reading, down from -7 in January and at a much lower 39th percentile reading below that index's median (which occurs at the 50th percentile on this metric by design).

Importantly, the 12-month ahead assessment of unemployment is lower at a -7 reading compared to January's -5. This is still slightly higher than it was in November/December, importantly marking a reversal in the deterioration. While the overall situation may have worsened, fears of 'the worst' that could happen (job loss) have not gone South along with it. Unemployment expectations stand in the lower 27th percentile of their historic que of data. This ranking of a 'bad event' is symmetrically just off the lower quartile of its historic queue, a similar relative position in consumer welfare terms to the headline and to the overall past-situation ranking.

The household budget assessment had jumped in January and it gave back only one point of that nine-point jump in February. Households' own budget assessment sits in the top 22 percentile of its historic queue of data, marking it as another relatively firm reading and this one with some recent positive upward momentum.

The households' financial situation sits on shifting sands. Both the current and the next 12-month assessments are slightly weaker in February than they were in January. But the backward looking assessment is still slightly improved compared to previous months' assessments. The outlook reading represents ongoing slippage after a stepped up deterioration in January. The backward (or current) assessment has a strong 83rd percentile standing while the forward looking assessment, beset with slippage, has a 36th percentile assessment.

Despite the slippery slope of the financial situation, current savings score as a bit harder to achieve while in the outlook savings are expected to be easier to achieve. And the outlook standing for expected saving is better than this assessment only 6% of the time while current measures of savings generate a lower third-of-queue ranking at its 36th percentile.

The environment for making major purchases currently is slightly weaker on the month; but it also is little-changed from recent readings and logs an 80.7 percentile queue standing. The all-important major purchase environment is better only about 20% of the time.

Business confidence

By comparison, the business confidence index is rising on a series of monthly gains to its 77.8 percentile standing. In their survey, businesses have seen their order books expand to strong readings that are better only about 15% of the time. In a separate report of actual order volumes, Italy's industrial orders increased at the fastest pace in four months in December on strong domestic demand. Industrial orders grew 2.8% on a monthly basis in December, following a 1.7% rise in November. The orders data bear out the optimism in the survey; note that the harder order count data are up to date only through December while the survey stretches our horizon to February. That is one of the main reasons to do surveys: that they can be conducted more topically.

Summing up

On balance, Italy's consumer and business confidence readings are somewhat reassuring. The respective levels of the indices are solid, but for the consumers the trend is a bit troubling. In the background, the Italian economy and political scene provide a backdrop with some important issues festering. It is important to view the Italian confidence reports as being so-far-so good since a thoughtful take on the responses leave us wondering why some of the unresolved issues in the economy have not taken a toll on business or consumer confidence to a greater extent. Since there are problems in need of a solution and since no solutions are in train, a somewhat skeptical embracement of these assessments is encouraged. There is still a lot in the Italian economy that could go wrong and unhinge the current and expected responses in the confidence survey.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief