Global| Apr 24 2018

Global| Apr 24 2018Italian Confidence Backtracks But Remains High-Valued As It Is for France and Germany

Summary

Italy can be a difficult country to understand. Its GDP has lagged badly since the great global recession. From Q1 2008 to date, Italian GDP actually has failed to grow and has declined by 5.8%. That’s a period of 10 years without net [...]

Italy can be a difficult country to understand. Its GDP has lagged badly since the great global recession. From Q1 2008 to date, Italian GDP actually has failed to grow and has declined by 5.8%. That’s a period of 10 years without net GDP growth and instead with some net GDP shrinkage averaging about -0.5% each year. Italian banks remain in terrible shape. The Italian unemployment rate is the second highest in the EMU among original EMU members at 10.6%. Italy is one of only three EMU members with its unemployment rate above its median rate after the long period of ‘European’ recovery. On top of that, Italy still can’t seem to form a government. And yet Italian confidence over the past 17 years currently ranks as being in the top 3% of all those confidence measures; business confidence is in the top 17% of all such metrics. How can that be?

Italy can be a difficult country to understand. Its GDP has lagged badly since the great global recession. From Q1 2008 to date, Italian GDP actually has failed to grow and has declined by 5.8%. That’s a period of 10 years without net GDP growth and instead with some net GDP shrinkage averaging about -0.5% each year. Italian banks remain in terrible shape. The Italian unemployment rate is the second highest in the EMU among original EMU members at 10.6%. Italy is one of only three EMU members with its unemployment rate above its median rate after the long period of ‘European’ recovery. On top of that, Italy still can’t seem to form a government. And yet Italian confidence over the past 17 years currently ranks as being in the top 3% of all those confidence measures; business confidence is in the top 17% of all such metrics. How can that be?

Confidence in Italy has slipped in April. For business confidence, it is the second monthly setback in a row. For consumer confidence, it is a one month only slip. But the real story is how well Italian confidence has held up and how high it is in the face of all sorts of political and economic adversity especially after 10 years of economic slippage.

And Italy is not alone in its current slippage. The German IFO index backtracked in April with the IFO President, Clemens Fuest, saying that the German economy is slowing down. Just a week ago, the IMF had lifted its global outlook (by a very small amount). Certainly, the German economy faces some uphill struggles as further sanctions have been placed on Russia, a country that German’s have done significant trading with. And the U.S. steel and aluminum tariffs have been announced and thus far Germany has not gotten an exemption. German exports are 48% of GDP and imports are 40% of GDP; thus, marking Germany as extremely sensitive to trade issues although much of this ‘international trade’ occurs under the framework of a single currency. Still, a slowdown in Germany is not good news. Note the low reading for German expectations compared to the specific sectors and current conditions.

Full results of the monthly IFO survey are not yet available; services are missing.

France has also issued a survey pointing to a weaker manufacturing environment in April.

However, there are surveys and there are surveys... The Markit flash PMI survey for April released just yesterday showed only the smallest tick lower for German manufacturing in April and a modest decline for manufacturing in France.

Still, this is a lot of news about ‘weaker’ at a time that the IMF has been trumpeting ‘stronger.’ And in the U.S., the Trump tax cuts and fiscal plan were supposed to be pushing growth up and allegedly were an important reason for the Federal Reserve to have become the global champion for higher interest rates. Oil prices have been surging to the $70/barrel level on a combination of growth, special factors and outright manipulation. In the U.S., the ten-year note rate has come within a hair’s breadth of the 3% yield mark. So which is it? Is the global economy tightening or isn’t it? I have been noting weakening data reports for some time. But this is an age when central banks with the bit in their teeth run with their forecast where they wish and the hard tug of data in a different direction seems to make little difference to them. Is that about to change?

What we do see is some substantial evidence of weakening. That weakening is a slow starting process. Manufacturing and other economic gauges are still very high valued even after falling in the month.

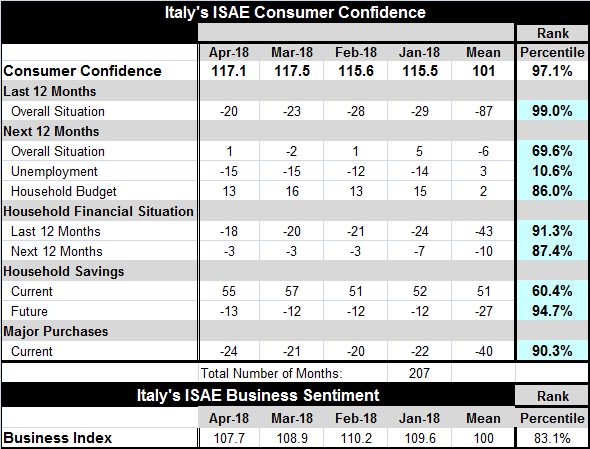

The Italian survey is a good example of this.

Consumer confidence stepped back in Italy to its 6th highest reading in the last 17 years as of April. The overall situation for the 12-month period just concluded ranked in the top 1% of all such historic responses. So lesson number one is that people are coming off a time that they believe to have been quite good. Over the next 12 months, the current overall situation has a 69% percentile standing. It has been assessed as better about 30% of the time. That’s not shabby, but it is far from excellent.

Unemployment prospects fell in March and stayed at that low reading in April. Unemployment fears have been lower historically only about 10.6% of the time. That is a good reason to have boosted confidence. However, the expected household budget situation eroded for the outlook over the next 12 months, falling back to a still strong 86th percentile standing.

The last 12-month household financial situation improved in April to a 91st percentile standing for the response and the outlook for the next 12 months remained steady at its value of the last three months; it had moved sharply higher in February. As a result, the outlook for the next 12 months is still very strong at a 87th percentile standing.

The current environment for savings is assessed at a modest 60th percentile standing, but for the future, savings prospects are at a strong 94th percentile standing.

The spending environment has deteriorated for the second month in a row, but it still maintains a 90th percentile standing.

The April Italian snap shot tells us that consumers have good feelings from the economic performance of the past year and because unemployment prospects are considered to be quite low. Households view their budget situation as having been in good shape with a strong ability to save in the period ahead. The ability to make a major purchase is well enabled. The responses to the survey in their way are clear enough, but the rationale for them remains somewhat obscure. The Italian populist parties gained in the election but have been unable to form a government. Nothing in that is reassuring unless it is extremely good news that government is crippled.

France has protests underway nationally to resist President Macron’s labor market reforms. Mr. Macron is in the U.S. trying to convince U.S. President Trump not to cancel the Iran nuclear deal. World leaders really have their focus split between the economics and geopolitics. It remains surprising how little all the turbulence and uncertainty as well as economic dislocation have affected consumer attitudes.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief