Global| Jul 21 2017

Global| Jul 21 2017Is Canada Showing the G7 How to Do It?

Summary

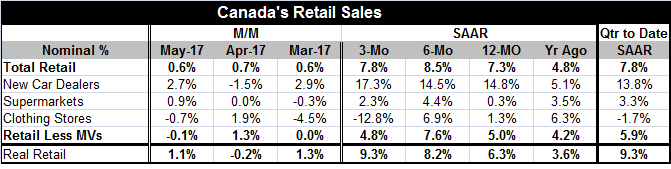

The chart and table present data in slightly different formats. Nonetheless, they come to the same conclusion that Canada's retail sector is on very solid ground. This is something that most G7 countries cannot say. U.S., EMU and [...]

The chart and table present data in slightly different formats. Nonetheless, they come to the same conclusion that Canada's retail sector is on very solid ground.

The chart and table present data in slightly different formats. Nonetheless, they come to the same conclusion that Canada's retail sector is on very solid ground.

This is something that most G7 countries cannot say. U.S., EMU and Japan's retail sales have become irregular. In the U.S., auto sales, long a staple of strength in its recovery, have finally started to flounder revealing serious problems in the sector. But Canada's retail sales are in very good shape with or without autos. With autos, sales and real sales are accelerating steadily. Without autos, sales are not accelerating, but they are growing at a solid pace.

At the same time, Canada is without an inflation problem as its principle inflation measures are all well below 2% and yet cruising at speeds that do not suggest deflation is encroaching either. Canada is in the catbird's seat.

Among NAFTA members, Canada has the best performing manufacturing sector and this is even with all the problems in the oil patch and Canada's dependence on oil extraction and on other natural resource intensive industries. The U.S. and Canada do have a timber dispute. And their NAFTA relationship is being addressed for renegotiation. However, on balance, Canada's economy is really firing on all cylinders and seems to be generating balanced growth. It is even logging an unemployment rate quite close to what is being reported in the U.S.

Among NAFTA members, Canada has the best performing manufacturing sector and this is even with all the problems in the oil patch and Canada's dependence on oil extraction and on other natural resource intensive industries. The U.S. and Canada do have a timber dispute. And their NAFTA relationship is being addressed for renegotiation. However, on balance, Canada's economy is really firing on all cylinders and seems to be generating balanced growth. It is even logging an unemployment rate quite close to what is being reported in the U.S.

Canada in Context

I hesitate to open this issue and raise the possibility of sending 'bad luck' in Canada's direction, but the economy really may be the best performing economy in the G7. Not even Germany shows the stability that Canada has and Germany is going to be caught up in Brexit plus it has issues with migrants in its economy that Canada largely does not have, although Canada has absorbed asylum-seekers too.

Balanced growth but not wholly in charge of its own fate

Canada has logged strong retail sales in the past few months. Its quarter-to-date retail sales growth is strong as well, with one month left to be recorded in Q2. Its inflation is moderate; its unemployment rate is low. Canada for the time being is a model G7 economy. How long can that last? So far, we see no excesses and no end in sight. Canada will have to renegotiate NAFTA and that may not prove to be too painful. Canada is not really the focus of NAFTA renegotiation; Mexico is. Canada's growth environment will depend importantly on global growth with the importance of natural resources in the Canadian economy. But for now, global growth is progressing. The brand new ECB 'Survey of Professional Forecasters' has just kicked up its outlook for EMU growth over the next two years. The biggest risk to the global environment is whether central banks can manage their inflation shortfalls. Can they?

Are central banks the biggest risk to stability?

Central banks may actually be the biggest risk to the growth environment. They have not made peace with trend inflation, plus there is OPEC trying to boost oil prices, a process that should send a one-time lump of inflation through the system that central banks (once again) could misinterpret as either inflation progress or as the long feared inflation acceleration. The simple fact is that, oil aside, global growth is persevering even on sub-par inflation. Central banks have options to deal with this. They could (1) enjoy it and put policy changes on hold (2) become more aggressive to boost inflation back up to a target that they have long missed (3) ignore inflation and boost interest rates back to normal because they continue to believe that inflation will accelerate and catch them with rates that are too low. Basically most central banks are not actually pursuing any of these options in their pure form.

Canada

The Bank of Canada has been close to pursing option (1) which is the enlightened option of the moment. However it recently stepped off this band wagon to initiate a rate hike and it may be transitioning to option (3) which I regard as the dangerous option of the moment. Whether this shift is in gear or not, depends on how the Bank of Canada policy unfolds from here on out. A 'program' of rate hikes would put the bank of Canada solidly in option (3). A one-and-done hike with watchful waiting could keep its membership in option (1). For all of its appeal on grounds of pure logic, option (1) still is not in favor among central banks at the moment. They are mostly busy worrying about the future and implementing - or ready to implement- option (3).

The U.S. stance

In the U.S., the Fed is pursing option (3) actually fearing that interest rates are too low, boosting them and planning to shrink its balance sheet even as inflation undershoots and growth has even turned up uneven. Federal Reserve policy is much more about the bank arrogantly making policy for what it forecasts and fears instead of taking its cue from an unexpected and poorly understood reality.

The ECB in action

Europe is somewhere between options (2) and (3). It is focused on hitting its target (option 2) or of the belief that getting up to it will not be a problem (option 3). The ECB is still using accommodative policies and yet it is expecting to transition away from them and these expectations have been focused on an environment that is different from current fundamentals. So the ECB has one foot solidly in option (2) and the placement of the other is in flux but seems headed for (3).

Japan is Japan is Japan

Japan is solidly in option (2) but without becoming more aggressive. Japan has aggressive rhetoric, but it seems to harbor fears reminiscent of option (3). Still, Japan policy can only be described at the moment as committed to option (2).

The Bank of England on the cusp

The BOE, however, is the best example of full throttle option (2). But with that option exercised in the wake of the Brexit vote, sterling crashed and now import price inflation is rising and factions on the BOE have transitioned to option (3) but with some support from incoming data (rising import prices). Still, imported inflation has not yet spread in the U.K., and growth is not strong and a negative growth hit from Brexit is still in the pipeline. While there may be better ways to implement option (2), the U.K. approach shows that exchange rates may not be a fruitful channel to explore. The BOE is in the most complicated predicament of all the central banks.

Canada's success

Against this background, you can see why I view Canada as an island of stability in a mucked up global economy. But the Bank of Canada has yet to show its real colors. Even where economies are doing well or riding improving trends there are policy issues. Central banks are simply not prepared to deal with the challenges of too low inflation. It is not surprising that they are so willing to put current trends aside and to continue to make policy as if the re-emergence of inflation is the next challenge. It's all they know. But what if it isn't part of this reality?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief