Global| Jan 22 2018

Global| Jan 22 2018Irish PPI Shows Mixed Trends; Which Ones Do We Believe?

Summary

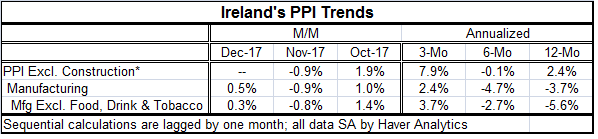

Ireland's manufacturing PPI fell by 3.7% year-over-year. However, the headline whose December observation is not available shows more pressure through November as its three-month pace hops up to 7.9% and whose year-on-year pace is [...]

Ireland's manufacturing PPI fell by 3.7% year-over-year. However, the headline whose December observation is not available shows more pressure through November as its three-month pace hops up to 7.9% and whose year-on-year pace is solidly positive at 2.4%.

Ireland's manufacturing PPI fell by 3.7% year-over-year. However, the headline whose December observation is not available shows more pressure through November as its three-month pace hops up to 7.9% and whose year-on-year pace is solidly positive at 2.4%.

The sequential pattern for manufacturing also shows more pressure over three months on a gain of 2.4%, up sharply from its six-month pace of -4.7%.

But it is for manufacturing excluding food, drink and tobacco that we see a clear pattern of acceleration emerge. On the sequential timeline, this measure shows a 5.6% drop over 12 months, a 2.7% pace of decline over six months, and an annualized gain of 3.7% over three months.

On the year-over-year chart, Irish inflation for manufacturing excluding food drink and tobacco shows a decline; yet, on the sequential timeline it shows a relatively sharp reversal and acceleration taking place at the same time. This sequential chart shows short-term Irish inflation momentum using manufacturing prices excluding food, drink and tobacco. Overall year-on-year prices are dropping, but over shorter periods the transition is to prices that are rising at a significant pace, 3.7% annualized over three months.

This sequential chart shows short-term Irish inflation momentum using manufacturing prices excluding food, drink and tobacco. Overall year-on-year prices are dropping, but over shorter periods the transition is to prices that are rising at a significant pace, 3.7% annualized over three months.

Of course the real issue here is oil prices. We covered the impact of oil prices in our earlier report (See January 19) on German prices showing the impact of oil on consumer and producer level prices there. Ireland too is feeling the impact of rising oil. And there are different interpretations of what that means.

Oil

But it is well known that oil does not play nice in markets. It is cantankerous. It overshoots and it undershoots and it is rarely well behaved. For the moment, with global growth looking better and oil up, there is fodder for those who (finally) see inflation rising. But inflation isn't really rising. And wage gains remain largely under wraps despite what in some places are very tight labor markets. All the risk factors for inflation are there: tight labor markets, rising oil prices, and economic growth is still kicking in... except inflation itself remains missing.

The evolving global scene

In the U.S., there is a sharp bond market sell-off that has been in progress on speculation over either coming Fed rate hikes, stronger growth or rising inflation or some combination of the three. Europe has similar fears in place. Oil prices are certainly part of that equation. And although fracking activity in the U.S. continues to step up, some are impressed that OPEC has held its agreement together for so long and has been able to extend it as well including Russia as a key participant. Still, what has not been determined is why the U.S. bond market fall off has occurred. And recent data have begun to show that growth may not be so strong and that inflation expectations are still well under wraps. And at some point, if those trends continue, that will raise second thoughts about inflation, oil prices and monetary policy. The second set of linkages is not yet in play. And all those trends will be important for Ireland either because the U.S. is an important country or because it will be reflecting global trends as well. But for the near term, markets will probably sit back and focus on what European policy decisions are going to look like since they are more in flux and less certain.

Ireland shows tightness, but does it matter

Ireland, with an unemployment rate of 6.1%, has the fifth lowest unemployment rate among original EMU members. Its rate has been lower only 35% of the time since end-1990. The unemployment rate in Ireland has fallen by 1.4% over the last 12 months.

Old vs. new inflation fundamentals

While many are focused on what I will call old inflation fundamentals (which have deteriorated), the new inflation fundamentals are still positive and holding actual inflation at bay. The new fundamentals include inflation expectations, technology and global trade competition. They also include new corporate practices in which firms look to keep prices low to get and keep business and a public with a much better understanding of price largely because of the internet and cell phones which function as excellent price discovery devices. Domestic tightness in the labor market does not matter as much anymore since labor services can be gotten overseas or tasks can be space-shifted by the internet or otherwise dealt with using technology. If that is not enough, there is always outsourcing to foreign markets which still have a lot of slack. China still has a need to grow rapidly and absorb its excess resources. These options all of which are relatively new have caused the old Keynesian metrics on inflation pressures to be overstated or misstated. And Ireland, as a small country, is not in any position to dictate what the global wage rate will be. On balance, I think inflation trends are not much use unless we extract oil prices from them. And I continue to believe the outlook for oil is for considerably weaker, not stronger, prices. Fracking is going to contain oil prices and probably drive them back. The IEA estimates that the U.S. will out-produce Saudi Arabia in oil before the end of 2018. If oil pressures are alleviated lot, a lot of the fear about inflation will dissipate. But the true fundamentals are about a lot more than oil. And they remain very positive for the outlook for continued inflation moderation.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief