Global| Jul 10 2015

Global| Jul 10 2015IP in France and Italy Advances

Summary

Both Italy and France show that broad IP trends are improving based on year-over-year growth rates, as the chart clearly demonstrates. But their short-term trends show very different dynamics. Even the year-over-year trends show very [...]

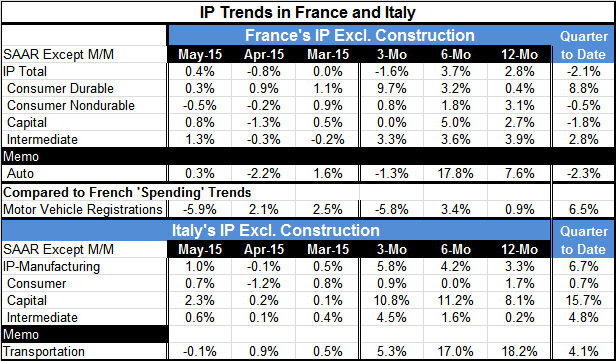

Both Italy and France show that broad IP trends are improving based on year-over-year growth rates, as the chart clearly demonstrates. But their short-term trends show very different dynamics.

Both Italy and France show that broad IP trends are improving based on year-over-year growth rates, as the chart clearly demonstrates. But their short-term trends show very different dynamics.

Even the year-over-year trends show very different forces at work in the French and Italian economies. Both show IP up in the neighborhood of 3% over 12 months. But French IP is boosted by the output of consumer nondurable goods followed by intermediate goods and capital goods. Italy's output is led heavily by capital goods followed by consumer goods with intermediate goods output barely higher year-over-year.

Over the shorter sequential periods, Italy is driven still by capital goods but with intermediate goods output picking up and consumer goods output listless. In France, the strength switches in more recent periods to durable consumer goods with capital goods and consumer nondurables weakening and with intermediate goods output saying firm. French auto output and domestic spending on autos have weakened. For Italy, auto output has been firm to strong.

While both Italy and France show different areas of strength, each economy is showing continuing strength in output. Italy's strength remains centered in capital goods with intermediate goods catching on. In France, consumer goods and intermediate goods are more consistently strong. The quarter-to-date shows that these trends remain in force.

Perhaps the best news for France and Italy is that Greece appears to be making a deal with the EU. If this progresses, it will likely means that speculative pressures will not develop on other economies in the euro area that have been struggling with austerity to some degree. But it also underlines the principle that the EU expects compliance with austerity goals as Greece appears to be giving in to many of the EU demands (capitulation). In the end, the message from the EU is this: my way or the highway. We will first of all see if this Greek deal does go through as it must be struck then approved by member parliaments. Next we will see what impact this set of negotiations will have on anti-austerity parties in other EMU nations as they were at first emboldened by Greece's actions but must now be cowered by its capitulation. What a difference a week makes!

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief