Global| Jun 14 2017

Global| Jun 14 2017IP Gains But EMU PMI Points to Even Stronger Gains

Summary

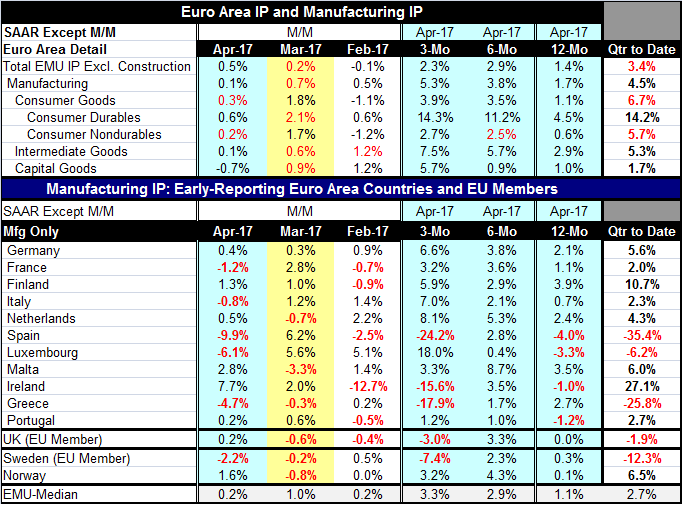

Industrial output in the EMU gained 0.5% in April after a 0.2% increase in March. Sequential growth rates show growth and do not signal any new growth trend. But in the quarter-to-date, IP (IP excluding construction) is advancing at a [...]

Industrial output in the EMU gained 0.5% in April after a 0.2% increase in March. Sequential growth rates show growth and do not signal any new growth trend. But in the quarter-to-date, IP (IP excluding construction) is advancing at a strong 3.4% pace.

Industrial output in the EMU gained 0.5% in April after a 0.2% increase in March. Sequential growth rates show growth and do not signal any new growth trend. But in the quarter-to-date, IP (IP excluding construction) is advancing at a strong 3.4% pace.

Manufacturing IP is up at a strong 4.5% pace in the quarter-to-date (QTD) and it shows sequential acceleration in progress, with growth rates rising steadily from 12-month to six-month to three-month. Consumer durables are strongly pushing manufacturing higher as its QTD growth rate is 14.2% and its sequential growth rate is surging; its acceleration shows 12-month growth at 4.5% stepping up to an 11.2% annualized pace over six months and to a 14.3% pace over three months. Consumer nondurables also exhibit an accelerating trend but one that is more modest with quarter-to-date growth still quite strong at a 5.7% pace. Intermediate goods log a 5.3% QTD pace and show accelerating output growth that rises from 2.9% over 12 months to an annualized pace of 7.5% over three months. Finally, capital goods with a very modest 1.7% QTD growth rate exhibit a slight pull back from sequential acceleration as six-month growth comes up slightly short of the year-over-year pace breaking the chain of accelerating growth. Still, capital goods output does accelerate to a three-month pace of 5.7% annualized.

These growth rates for EMU IP show a breadth of gains in output that spans all sectors. The overall results look very solid.

Germany, France, Finland, Italy, the Netherlands, Luxembourg and Portugal each individually experience accelerating manufacturing output from 12-month to six-month to three-month. This grouping includes three of the EMU four largest economies. It encompasses seven of the eleven EMU members whose data are memorialized in the table and provides a solid basis for the belief that manufacturing output is advancing on a geographically broad basis as well as on a broad sector basis - a potent combination.

However, five countries still manage to log IP drops in April, including three that are on the list of those with sequentially accelerating output (i.e., France, Luxembourg and Italy). Moreover, the smallest month-on-month IP falls came from Italy at -0.8% while manufacturing IP declines were as large as 4.7% in Greece, 6.1% in Luxembourg and 9.9% in Spain. Despite the statistics on the growing breadth of output that is also endorsed by the Market PMI readings, there are still considerable pockets of severe monthly weakness that come into play.

The sequential growth rates show only three EMU nations with IP declining over three months (Spain, Ireland and Greece). But broadened to an EU framework, two more decliners appear on the list, Sweden and the U.K. While short-term growth rates do show some pop with five of eleven reports showing growth of better than 5% over three months, Spain, Ireland and Greece each have negative three-month growth rates in excess of a 15% annual rate. In some cases, this is just volatility and represents great difficulty with seasonal adjustment; Ireland and Spain are two examples of that. But more broadly, we would be wise to not try to look past the various clustering of weakness just because we can also find a somewhat larger clustering of strength.

Despite the fact that the Markit EMU PMI gauge has ramped up in 2017, the average IP gain is still weaker than it was in 2015 when the PMI gauge generally was lower. The PMI gauge has yet to prove its stuff as a harbinger of stronger growth.

There are a number of reasons to be positive on growth continuing, but the prospect for continued acceleration may not be quite so bright. Ongoing weakness with inflation may be an indicator of still limping consumer spending. The U.K., for example, has posted some recent poor spending barometers even though its unemployment rate is at a 42-year low. Wages in the U.K., like wages in the U.S., are not rising despite the low unemployment rate. New price data, in fact, show that real wages in the U.K. are being eroded.

Europe continues to have cross currents. Even though the U.K. is still only in the EU and looking to exit, it is still Europe's second largest economy and a growth set back there will have adverse consequences for the rest of Europe. After that, there is still the question of Brexit negotiations and how they will affect the rest of Europe. While the ECB is being pressured to hike rates by the German finance ministry, Germany reported out today its weakest inflation reading in six months. Conditions in Europe remain hard to pin down as they do in the U.S. with such an unexpectedly weak CPI report released today on top of a weaker-than-expected report on retail sales. Central banks are still trying to get a grip on the policy process and the data are not making it an easy thing to do. The risk of a policy misstep is still substantial.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief