Global| May 27 2020

Global| May 27 2020INSEE Surveys Show Ongoing Weakness in France

Summary

Overview: The French economy shows the ongoing impact from the coronavirus and the steps taken to curtail it. The manufacturing climate gauge has a 1.3 percentile standing (rarely weaker). Manufacturing production expectations have a [...]

Overview: The French economy shows the ongoing impact from the coronavirus and the steps taken to curtail it. The manufacturing climate gauge has a 1.3 percentile standing (rarely weaker). Manufacturing production expectations have a 5.7 percentile standing. The climate indicator for services has a 0.4 percentile standing, the same standing as the outlook gauge. The household sector is seemingly less impacted perhaps because of the government support efforts. But household confidence has a 24.2 percentile standing, still very weak but not quite the exceptional weakness of the sector surveys. That is even with the expectations for unemployment at a 99.2 percentile standing. Households' assessment for their own financial standing has swung from a 96.7 percentile assessment over the past 12 months to an 11.3 percentile assessment over the coming 12 months. No survey is untouched.

Overview: The French economy shows the ongoing impact from the coronavirus and the steps taken to curtail it. The manufacturing climate gauge has a 1.3 percentile standing (rarely weaker). Manufacturing production expectations have a 5.7 percentile standing. The climate indicator for services has a 0.4 percentile standing, the same standing as the outlook gauge. The household sector is seemingly less impacted perhaps because of the government support efforts. But household confidence has a 24.2 percentile standing, still very weak but not quite the exceptional weakness of the sector surveys. That is even with the expectations for unemployment at a 99.2 percentile standing. Households' assessment for their own financial standing has swung from a 96.7 percentile assessment over the past 12 months to an 11.3 percentile assessment over the coming 12 months. No survey is untouched.

Timing is everything...

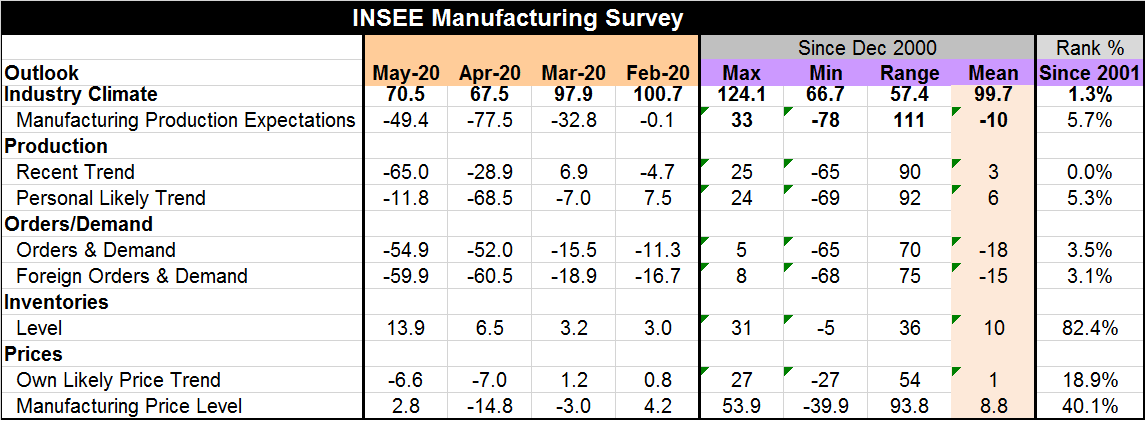

The table shows the timing of the impact of the virus and constraints imposed to contain it month-by-month. In February, manufacturing production expectations are at a -0.1 level. That deteriorated sharply to -32.8 in March and again to -77.5 in April. The new numbers from May show some mitigation with a reading of -49.4, nearly halfway between the March and April readings – but still quite weak. Production shows roughly the same progression. However, orders and demand have continued to slip without sign of rebound. That suggests to me that raw expectations are willing to see progress ahead but that firms are not actually acting that way yet and not committing to placing orders. This reinforces the primacy of the orders data as being powerful indicators. Inventory levels are rising and prices generally are showing increasing weakness. All of the rank or queue standings are low except for inventories that are accumulating. Price ranks are sub-median but not as weak as for other components.

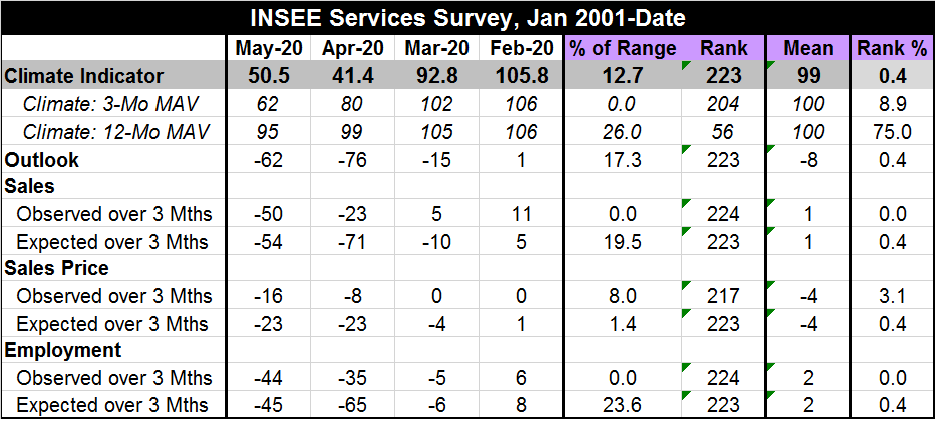

The service sector progression is quite similar to the one for manufacturing. This underscore that the weakness is not be led by one sector but represents common sector responses to an overarching government edict. The headline indicator and the outlook both have deteriorated and then recovered some ground in May as is the case in manufacturing too. However, sales continue weaken although expected sales hit their trough in April and rebounded smartly in May. Both observed and expected prices are weakening much more than for manufacturing (based on rankings).

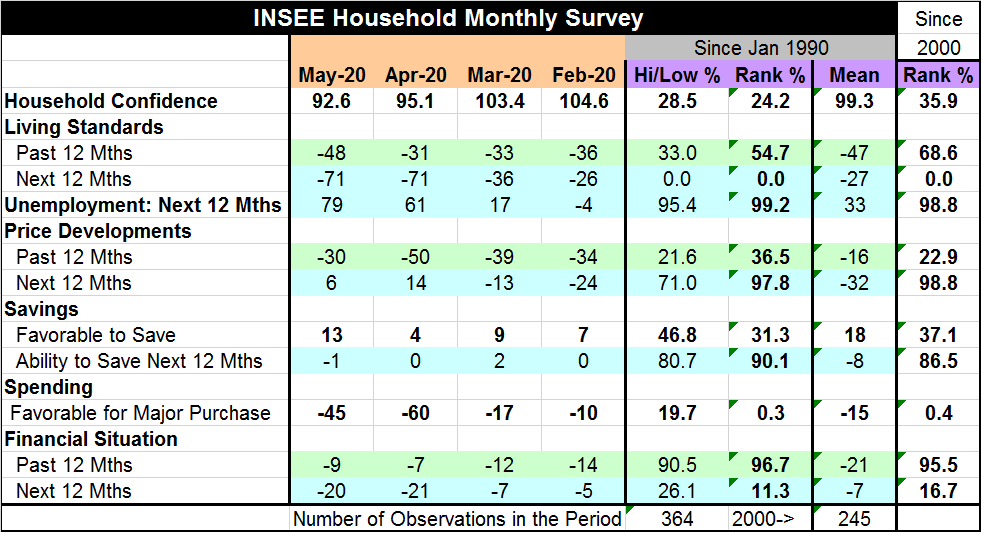

The household data show ranking on two different timelines, a long one back to 1990 and a shorter one to 2000 to accord with the two sector surveys above. The household sector's overall ranking is not as low as for the two sectors. But important elements of this survey are just as weak. For example, the living standards for the next 12-months rank as low as they ever have been. And the response to the question 'is it a favorable time for major purchases' also ranks very low, in the bottom one percentile of its historic queue of data. At least this category showed some rebound in May. Living standards, the financial situation and unemployment prospects all simply erode and stay low. In that sense, the household sector may be in worse shape than the business sectors that are showing some rebound on the same timeline.

Governments are going to have to figure this out. Europe is more used to social welfare support schemes. The U.S. is foreign to those except as support for the very poorest. Still, it is clear that governments cannot make life in a pandemic easy for everybody or treat everyone equally (fairly). When a support scheme is implemented, someone always seems to fall through the cracks. Someone stays home; someone else works and is exposed. That aspect makes the idea of extending lockdowns or waiting for a vaccine quite unpalatable and unfair. But that tact still has a strong voice of support globally. Global data from Johns Hopkins today showed that based on global infections and deaths the morbidity rate from the COVID-19 is about at 0.6%. It is higher than for the flu, but it is also very highly concentrated in the sub-population with other health ailments. NYC data suggest that people with underlying medical conditions are about 140 times more likely to dies from the virus than people with no underlying issues. That makes the morbidity rates for the healthy and the unhealthy extremely different and exceptionally low for the healthy.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief