Global| Aug 24 2017

Global| Aug 24 2017INSEE Industry Indicator Reaches Near Decade High

Summary

The French industry climate gauge at 111.3 in August is up from 108.1 in July and at its highest reading since December 2007, logging its highest reading in nearly a decade. The industrial climate gauge standing is in the 77th [...]

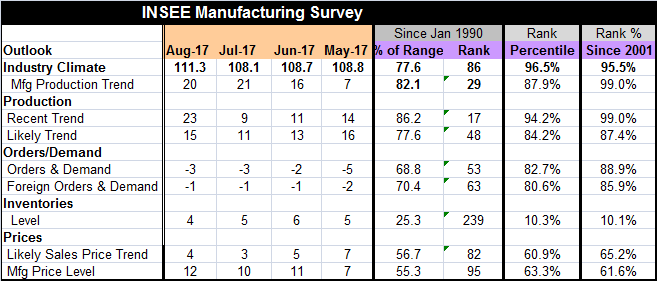

The French industry climate gauge at 111.3 in August is up from 108.1 in July and at its highest reading since December 2007, logging its highest reading in nearly a decade. The industrial climate gauge standing is in the 77th percentile of its historic range of values since 1990 and at the 86th queue standing percentile over that period. Over the shorter period, since 2001, the queue standing is at its 95.5 percentile. Any way you slice it, the current reading is strong and represents strong momentum for French manufacturing. This survey and the diffusion index survey conducted by Markit produce similar strong readings with solid momentum for French industry and manufacturing.

The French industry climate gauge at 111.3 in August is up from 108.1 in July and at its highest reading since December 2007, logging its highest reading in nearly a decade. The industrial climate gauge standing is in the 77th percentile of its historic range of values since 1990 and at the 86th queue standing percentile over that period. Over the shorter period, since 2001, the queue standing is at its 95.5 percentile. Any way you slice it, the current reading is strong and represents strong momentum for French manufacturing. This survey and the diffusion index survey conducted by Markit produce similar strong readings with solid momentum for French industry and manufacturing.

The manufacturing production trend eased slightly by one point in August after a five-point jump in July on the heels of a nine-point jump in June. Because of this recent surge, it is not clear that the August backtracking is any kind of a cooling signal. The queue ranking since 2001 for the production trend is in its 99th percentile - impressive.

Production trends are rising. Not surprisingly, the recent trend is rated much higher than the likely trend since the recent trend has moved up so strongly - it is clearly so strong that it is not at a sustainable pace. The recent trend has ratchet up to a reading of 23 in August from 14 in May, compared to the likely trend which stands at 15 in August compared to 16 in May. The recent trend has a 99th percentile standing since 2001 while the likely trend standing is at its 87th percentile - a still strong reading.

Orders and demand as well as foreign orders and demand have chronically negative readings. This month's readings for each category are unchanged and little-changed over the last three months. Still, orders and demand rate an 88th percentile standing and foreign orders and demand rate an 85th percentile standing, very solid underpinnings for the index.

Inventory levels have been cruising in the range of 4 to 6 since May and have been low, in the 10th percentile queue standing; that tells us little about industry dynamics.

The manufacturing price level trend is slightly stronger than the likely sales price trend. But both of these gauges have moderate standings with the likely trend at a 65th queue standing and the actual price trend at a 61st percentile standing.

On balance, French manufacturing trends are strong and solid. The level of activity is high and momentum is impressive and still in high gear. The underpinning for the sector in terms of sources of demand draws from relatively strong domestic and international sources of strength. Prices, however, remain very moderate with little indication that any of the pick-up in the sector is going to contribute importantly to rising price pressures.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief