Global| Feb 23 2018

Global| Feb 23 2018Inflation Trends in EMU...NOT Cooperating

Summary

I know that I have created some dissonance here. The title says that inflation trends are not cooperating, but the chart clearly shows inflation is falling more places than where it is rising. So what is 'not cooperating' about that? [...]

I know that I have created some dissonance here. The title says that inflation trends are not cooperating, but the chart clearly shows inflation is falling more places than where it is rising. So what is 'not cooperating' about that?

I know that I have created some dissonance here. The title says that inflation trends are not cooperating, but the chart clearly shows inflation is falling more places than where it is rising. So what is 'not cooperating' about that?

Welcome to the 'New business cycle.' Central banks are still trying to figure it out. With growth widely believed to be 'on an upswing' and interest rates around the world still largely at subnormal levels, central bankers are worried about creating an inflation impulse and are at some stage of doing something about it, ranging from 'planning to doing.' With growth picking up, inflation is supposed to pick up too. And as those events go hand in hand, they create a clear path for central bank action. And THAT is what is not happening. There is no clear path and that is what creates the dissonance and division on policy at various central banks to various extents.

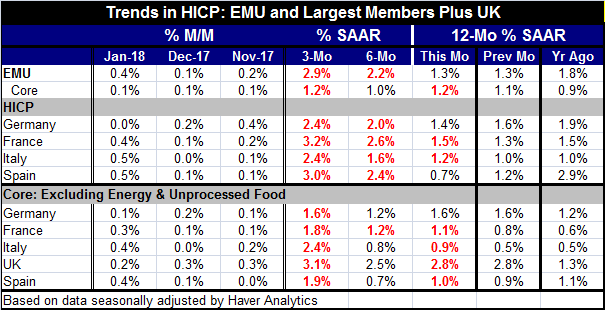

As the chart and table show, inflation in the EMU is well under its objective of just under 2%. The chart that plots a time series of year-on-year inflation rates shows that only France is seeing any sort of clear upward growth in the rate of inflation: not Germany, not Italy and not the EMU.

The table provides a close-up view of the numbers and has separate panels on headline and core inflation as it digs down into intra-yearly patterns that can be more revealing but are certainly more volatile and less reliable. The first thing we notice (12-Mo % SAAR: This Mo vs. Prev Mo) is that year-on-year and core inflation rates for the EMU are little change month-to-month if we compare 12-month percentage changes. Headline inflation is steady month-to-month, at 1.3%, in January; it is even lower than it was one year ago when year-on-year inflation was running at a pace of 1.8%. However, over six months headline inflation is up to a 2.2% pace (too hot!) and over three months it is hotter still at a 2.9% pace. The core HICP does not reinforce that trend as it is little changed in any of its annualized figures in the table on any horizon and remains close to a 1% annualized pace.

In the table, the bold red figures identify inflation acceleration between adjacent periods from six-month to three-month and 12-month to six-month and over 12-month for this month compared to the previous month. There is still a proliferation of 'red figures' in the table showing that while year-on-year inflation and trends may still be very well-behaved and described as too low, the intra-yearly patterns show some pressures are building in the economies of the largest EMU members.

In the core figures, we include the U.K. results for comparison; the U.K. is an important regional competitor that operates under a different currency regime. It is having a real problem with inflation since it has been trying to deal with the implications of the onset of Brexit. A super-stimulated monetary policy drove the pound lower and that has driven inflation higher which in turn put the Bank of England back on a tightening path. The BOE is learning the hard way that monetary policy may be adjustable, but that does always mean you want to turn the dial and adjust it. Adjustments have consequences.

Away from the U.K. results, core trends show only Italy with 'excessive core inflation,' as its three-month pace is 2.4% over three months. Only France shows any acceleration over six months. Most of the red numbers that are indicating inflation acceleration for a period are in the less reliable three-month column or apply to the headline where oil prices wreak havoc with trends. Other than that where core inflation trends are accelerating, it is for the 12-month pace of inflation compared the previous month and the uptick is minor.

Moreover, global oil prices that have been on a tear now are cycling lower as the fracking output in the U.S. continues to ramp up. In short, inflation dynamics are not taking hold.

In unrelated reports today, Germany reported out its GDP details and they show the strong role played by external demand in driving German growth. Germany shows all the classical tendencies of being a free rider. Is its inflation rate low and its fiscal situation solid? Yes. But how has it accomplished this? It has done it by being a poor international citizen. Foreign demand is driving growth in Germany not domestic demand despite Germany's enviable financial position. German military readiness was just assessed as being very poor. Not only is Donald Trump cajoling Germany and others to pay their fair share in NATO, Germany has been saving money by not maintaining military preparedness. Maybe that is why Angela Merkel got so hot when she thought Donald Trump was not going to be there to defend her. Trump was sending a message much more than he was threatening abandonment. Germany must step up its efforts. Germany has no qualms about running a Germany-first policy, but an America-first policy for the U.S. is apparently out of bounds and wrong. How does that add up?

Also on the international scene, General Motors was making news as it is trying to contain costs in South Korea. If anyone thinks that tight labor markets in the U.S. are going to quickly lead to wage pressures, I think you need to cast your gaze to Asia where growth has been weaker relative to targets and efforts are being redoubled for them to keep their competitiveness.

On balance, the reflation game seems like a wholly different game in this cycle. Dallas Federal Reserve Bank President Steven Kaplan has called this one of the most difficult periods he has ever seen for pricing power. The lack of inflation and the still-low pitch of inflation expectations are realities. Central banks are still raising rates in this cycle or planning to do so soon. With the Fed hiking rates in the U.S., some of the forward-looking measures on inflation and interest rate expectations have produced muddied signals. But it is still not clear that investors have lost any of their belief in still-low inflation. Inflation expectation surveys remain powerfully weak. And while we have had a lot of chatter about higher prices and wages, in the macro data these trends remain substantially muted. Kaplan has said that inflation is not going to turn up like a hockey stick. Maybe the Fed and other central banks should reconsider their slap-shot policies geared to remove accommodation from a distance before they know if that is a sensible thing to do or not.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief