Global| Dec 12 2017

Global| Dec 12 2017Inflation Hammers Away in the PPI Report, But the PPI Is a Square Peg Report in a Round-Hole World

Summary

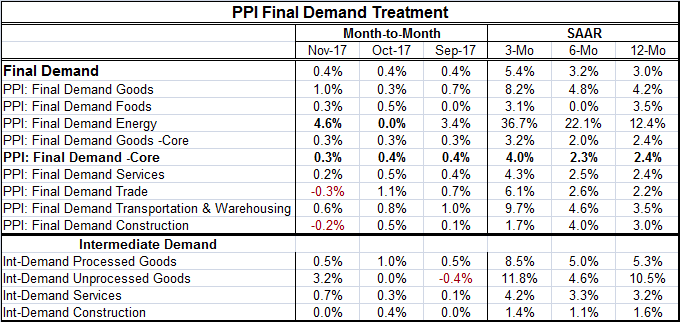

Core and headline PPI 'Final Demand' inflation are now moving up together. Both series are more or less sequentially. Headline inflation rises from 3% over 12 months to 3.2% over six months to 5.4% over three months. Core inflation [...]

Core and headline PPI 'Final Demand' inflation are now moving up together. Both series are more or less sequentially. Headline inflation rises from 3% over 12 months to 3.2% over six months to 5.4% over three months. Core inflation logs 2.4% over 12 months, then is more or less steady at 2.3% over six months and then rises to a pace of 4% over three months. The main question of interest is this: "will the Fed find this vexing?" The correlation between the PPI and the CPI yields an R-Square fit of 0.88 which means that PPI can explain 88% of the variance is the CPI headline- impressive. But there the magic ends. When we compare the core PPI to the core CPI, the R-Square falls to essentially zero- no explanatory power of the PPI core for the CPI core.

Square peg in a round-hole world

Still, I doubt that the FOMC will write off the PPI completely. And remember that the Fed actually targets the PCE where inflation is even lower than in the CPI framework. However, in the U of M consumer confidence report this month, there was a slight uptick detected in inflation expectations (which are nonetheless at extremely low historical levels). And in the last employment report, we saw that even with continued and unexpectedly strong job gains average hourly earnings trends remain remarkable docile. On balance, the PPI simply does not fit into the main inflation picture painted by other variables. It is a square peg in a round-hole world. It simply does not fit anywhere.

Special pressures in gear

One additional reason to 'write off', the PPI is the transitional behavior of oil prices which are on the rise again with energy costs busting higher by 4.6% in November and gaining at a 36% annual rate over three months. When there is such clear distortion to the trend, it is good to step back and gain some perspective. Final demand goods core inflation is actually showing less acceleration than final demand core overall with services and construction factored in. For the core goods measure, inflation transits from 2.4% over 12 months dropping to a 2% pace over six months then gaining to an elevated but more modest 3.2% pace over three months compared to the 4% pace of the overall core. Still, services, trade, and transportation & warehousing are sectors showing inflation building momentum at the PPI level. Construction is an exception.

Intermediate goods trends do not demonstrate sequential gains generally but do show that three-month inflation rates are higher than 12-month gains, except for construction.

Policy impact

As always, policy in the U.S. at the Fed is going to be conducted based on judgement and this Fed has been anything but 'rules oriented.' A pop in the PPI, however, fits into the scare scenario that several FOMC members embrace. The Fed is already on the rate-hiking path. With one meeting left under the direction of Janet Yellen, all eyes are on one more rate hike in December. Then the torch will pass to Jerome Powell, the new Chairman. And we have yet to find out how he will read the tea leaves. As I digest this report and you read this, economists are in the process of reassessing growth for 2018; more sentiment is gaining traction as the growth outlook is improving. More are hiking their projections for growth than are cutting them or holding their outlook steady. Some inflation forecasts are ticking higher for 2018. In addition, more firms on Wall Street are moving into the 'four rate hike' camp for Fed policy for the year ahead. And maybe that is the eventual transition that we will finally have in 2018 because it has been so long since real growth has set in and since any expectation of higher inflation has been fulfilled.

The economic framework

But the global facts remain the same. Despite some tick up in growth rates, China is still a low-wage behemoth and technology continues to gnaw away at the fabric of what might have been a wage increase. Even in the most recent jobs report, we see that wage inflation is not setting in. True, in today's NFIB survey, expectations and plans for wage and price hikes are beginning to drift to higher readings in that report. We will have to see if those plans are implemented. The NFIB also shows us that expectations are improving faster than current conditions are and that despite all this optimism, plans for capital investment are being pulled back not expanded. The world is filled with trends and counter-trends. Each investor has to make what he or she will of the divergences in data. Which are the real trends? Which are the 'fake' trends? ...to use a popular paradigm of the day. The notion of inflation acceleration does have some appeal and some place in the data. But with unit labor costs actual falling over the last two quarters, I just can't bite the bullet on hiking my inflation forecast yet. I remain unconvinced, and especially unconvinced by this report.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief