Global| Feb 18 2010

Global| Feb 18 2010Industrial Trends In UK Continue Turning Higher

Summary

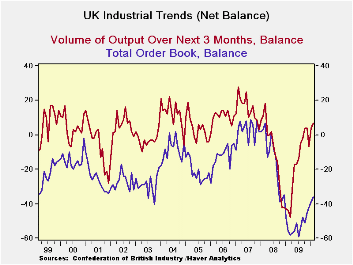

Industrial orders in the UK rose to a reading of -36 in February from -39 marking their best result Since December 2008. The plus-seven reading for expected output volume is the best reading since March of 2008. Orders reside in the [...]

Industrial orders in the UK rose to a reading of -36 in February from -39 marking their best result Since December 2008. The plus-seven reading for expected output volume is the best reading since March of 2008.

Orders reside in the 20th percentile of their range a still-low standing. But export orders stand above the mid point of their range at a percentile of 51.6%. Similarly expected output volume is in the 52nd percentile of its range and average prices expected are in the top 35% of their range. The ranges are from early 1989 to date.

Two observations from these results lead us to the conclusion first, that conditions are still severely impacted. Second, expectations are in place that foresee or expect that the economy is headed for normalcy. Having the three-month outlook variables above their range mid-point is a sign that things are expected to get back to normal in ‘three-months or so.’ Yet the still very weak readings for overall and export orders remind us that current conditions still are under a lot of stress.

The UK industrial sector is making progress. Elsewhere the housing sector is recovering and the budget deficit is ballooning. The UK is making progress but still has some great challenges. For now the news is that the progress continues.

| UK Industrial Volume Data CBI Survey | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Reported: | Feb 10 |

Jan 10 |

Dec 09 |

Nov 09 |

Oct 09 |

12MO Avg | Pcntle | Max | Min | Range |

| Total Orders | -36 | -39 | -42 | -45 | -51 | -52 | 34% | 9 | -59 | 68 |

| Export Orders | -23 | -33 | -41 | -37 | -46 | -45 | 53% | 3 | -52 | 55 |

| Stocks:FinGds | 12 | 13 | 15 | 20 | 10 | 21 | 42% | 31 | -2 | 33 |

| Looking ahead | ||||||||||

| Output Volume:Nxt 3M | 7 | 4 | -7 | 4 | 4 | -16 | 72% | 28 | -48 | 76 |

| Avg Prices 4Nxt 3m | 8 | -6 | -7 | -5 | -4 | -10 | 52% | 34 | -20 | 54 |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief