Global| Jul 20 2009

Global| Jul 20 2009Industrial Orders Trends Begin To Turn...Ever So Slowly

Summary

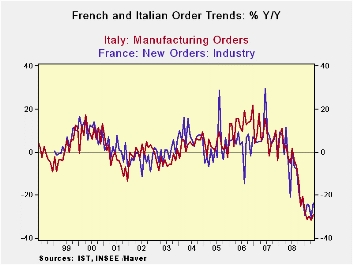

Industrial orders in Italy made a slight bounce in May. French orders fell after a slight bounce in April. Neither shows any sign of upward momentum and the downward momentum has only just been trimmed if we compare 3-month growth [...]

Industrial orders in Italy made a slight bounce in May. French

orders fell after a slight bounce in April. Neither shows any sign of

upward momentum and the downward momentum has only just been trimmed if

we compare 3-month growth rates to 12-month growth rates.

What is interesting is the very different performance in foreign

orders as between Italy and France and Germany. Germany is showing some

very substantial recovery in foreign-sourced orders. But it Italy,

foreign order are falling at an accelerating pace through May. In

France, foreign orders have shown a clear patterns of progress with the

three-month growth rate reduced to an annual pace of -9.7% compared to

-24% Yr/Yr.

Whatever progress is being experienced in Europe, it is irregular.

Clearly some economies in the Zone are doing better than others despite

the common currency regime - and that is true for sales overseas

underlining the that exchange rates are not the only factor in the

success of foreign sales efforts. The more variance there is across

e-Zone countries in their respective economic performances, the more it

will wear on the fragile e-Zone area where talk of integration is tough

despite member countries efforts to continue to go it alone on fiscal

policy. Europe still has a recession and still has some divisive

political forces to weather. And yet more European ‘integration’ lies

ahead.

| Saar exept m/m | May-09 | Apr-09 | Mar-09 | 3-mo | 6-mo | 12-mo |

| Total | 0.4% | -3.6% | -2.6% | -20.9% | -24.3% | -29.0% |

| Foreign | 0.2% | -2.9% | -9.3% | -39.4% | -27.5% | -33.0% |

| Domestic | 0.5% | -3.9% | 1.0% | -9.3% | -22.7% | -26.7% |

| Sales | -1.1% | -0.1% | -0.7% | -7.3% | -22.3% | -21.9% |

| French Orders | ||||||

| Saar exept m/m | May-09 | Apr-09 | Mar-09 | 3-mo | 6-mo | 12-mo |

| Total | -1.1% | 0.6% | -5.7% | -22.3% | -9.2% | -23.9% |

| Foreign | 0.4% | 6.5% | -8.8% | -9.7% | -12.4% | -27.0% |

| IP xConstruct | 2.4% | -0.6% | -1.4% | 1.4% | -15.1% | -15.0% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief