Global| Jul 27 2015

Global| Jul 27 2015In EMU, No Acceleration in Real Money or Credit...and Global Growth Has Its Issues As Well

Summary

Year-over-year trends show both EMU money and credit on better growth paths after a lull from late-2011 to late-2013 for credit and from 2013 to mid-2014 for money. But the growth rates from the table of one year or less tell a story [...]

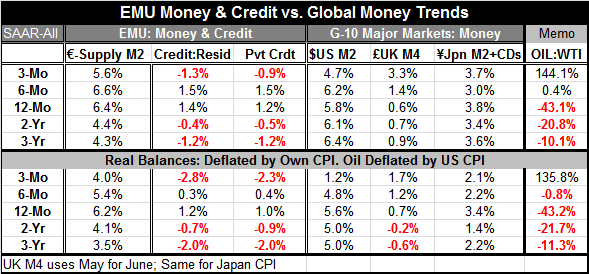

Year-over-year trends show both EMU money and credit on better growth paths after a lull from late-2011 to late-2013 for credit and from 2013 to mid-2014 for money. But the growth rates from the table of one year or less tell a story of relatively more stagnation. Money and credit growth may be broadly better than they were a year ago, but the pace is not picking up or some cases even being maintained.

Year-over-year trends show both EMU money and credit on better growth paths after a lull from late-2011 to late-2013 for credit and from 2013 to mid-2014 for money. But the growth rates from the table of one year or less tell a story of relatively more stagnation. Money and credit growth may be broadly better than they were a year ago, but the pace is not picking up or some cases even being maintained.

Private credit has a three-year growth rate of -1.2%. But the declines have been shed and credit is up by 1.2% over 12 months. At the same time, credit is now down at a 0.9% pace over three months. Overall credit to residents shows the same sequence of events: improvement followed by a recent lapse. Looked in CPI deflated terms (real credit), the recent rebound is minimized and the three-month decline is exaggerated. For money growth, the nominal growth rate is higher over three months, six months and 12 months than over 2-3 years. But in real terms, money growth progress is only in place for 12-month and six-month horizons.

In the rest of the money center countries, we see some slight to substantial pick up compared to the past 2-3 year trend. Between the U.K. and Japan, the U.K. shows the most money growth pick-up of late. In the U.S., nominal money growth has slowed over three months and real money growth has slowed sharply.

Apart from money and credit in Europe:

The European negotiations with Greece are put on hold for `technical reasons', but there are real undercurrents of disagreement about what will happen next. Greece has rolled over and played dead for the bulk of European demands, but there still are sticking points. Greece is just trying to minimize them. One of the back ground issues is debt forbearance (It's a foreground issue for Greece and the IMF- you can see it is such a sticking point that is hard to discuss). Today ECB board member Benoit Coeure has claimed that the euro area is well aware that Greece will need restructuring. There is no sense of whether that awareness will lead to action or it will lead to any forgiveness or if it will square with Greece's needs. Nor is it clear that Mr. Coeure has really captured Europe's thoughts correctly or if he is trying to steer them in his direction.

Economic reports on the day show a stronger German Ifo, but Finland's confidence for consumers and business is eroding and Dutch businesses are reporting declining confidence. The economic environment really is mixed although Germany's Ifo survey was impressive.

Meanwhile in Asia...

Hong Kong and Thailand report weaker exports, but the big news is for China where the largest stock market decline since 2008, an 8%-plus drop in China stocks has occurred on Monday. I guess government intervention works until it doesn't. We have been skeptical of this government's intrusion since it emerged. We think revisionism about China is in order.

Several years ago people were saying how astute Chain's leaders were and how they knew what their economy needed. But it was just a fast growth thing spiraling out of control with too much corruption and too much debt, piggybacking on foreign investment that wanted to produce with cheap labor and weak exchange rate. China was not well-managed; it was riding the tiger. That game is over and now all the excesses of that period are coming home to roost. The debt bomb has yet to explode. China's `astute' leaders are finding it hard to operate in this new model where they can't just cram cheaper goods into the export market and down westerner's throats. China now must develop its own domestic demand. That means striking a balance between what people are paid and what they earn. You can't stimulate demand on wages fit for gruel. Before this weekend the hedge fund Bridgewater had pulled the plug on its optimistic tilt on China calling the previous stock market rout an end to China has a safe haven for investment. In retrospect, that was a prescient understatement.

China now has years of misalignment, pollution, distrust, graft and simple incompetence to try to clear up in order to develop a reasonable environment for future growth. No wonder it has gone boldly to the South China Seas to saber-rattle with Japan and the U.S. and to try to take attention from its severe problems back home.

When we look at Europe, we see evidence of another great economic experiment gone-wrong. Both China and Europe are trying to fix something that went amiss. Of course, we can throw Japan and the U.S. in that same stew with slightly different ingredients. There has been a lot of economic mismanagement exposed by the great recession. It has taken on different guises in different places. Part of the pain of slow growth now comes from all these areas at once trying to restore balance and doing so using less than expansive polices- all at the same time. I think the common lesson here is to be careful what you believe in. Unfortunately, in economics it is hard to do double blind tests. That makes it more important to think things through than to just jump in determined to make something work that is not well-designed. We are now seeing examples of how hard that can be to fix.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief