Global| Sep 24 2020

Global| Sep 24 2020IFO Sectors Rebound... But With Restraint

Summary

The IFO index and its two principal components, the current index and expectations index, all improved in September. The sector responses showed an improvement in manufacturing and some weakness in services but not quite as much [...]

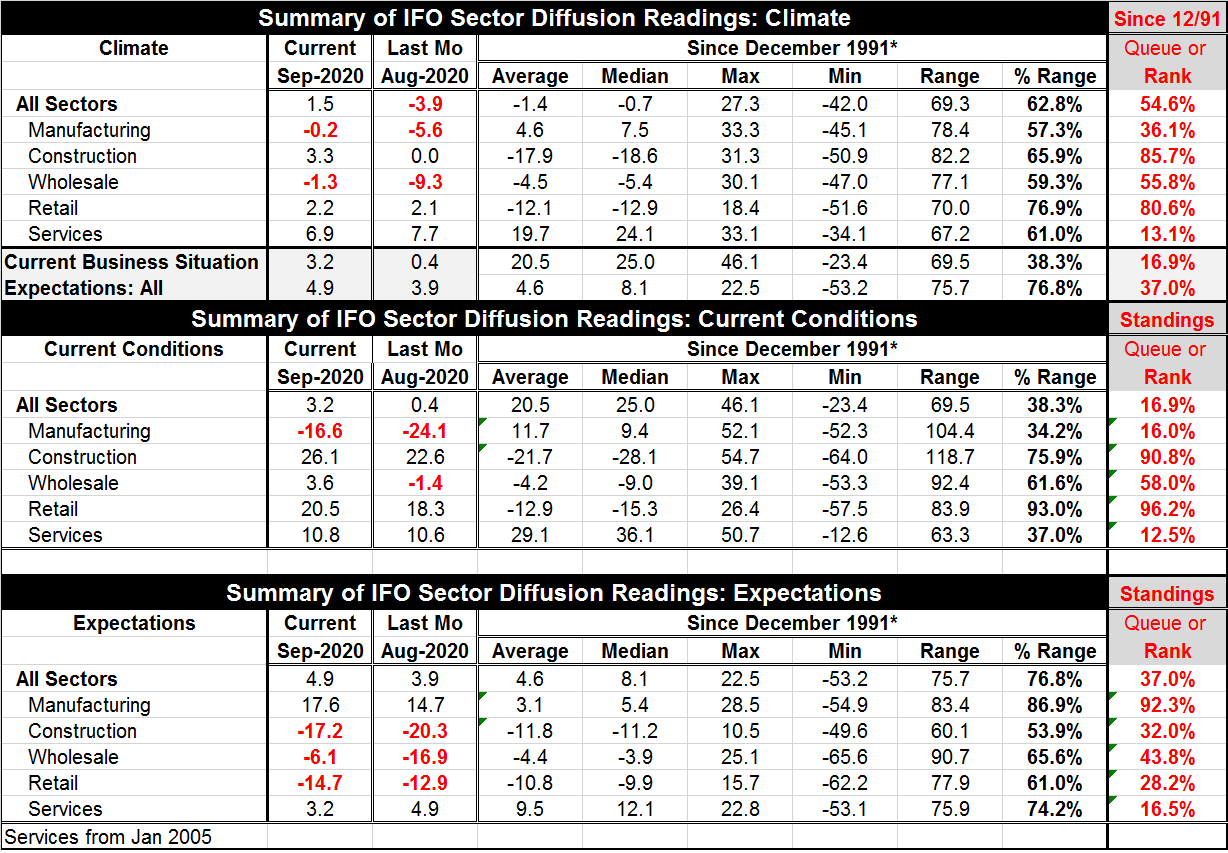

The IFO index and its two principal components, the current index and expectations index, all improved in September. The sector responses showed an improvement in manufacturing and some weakness in services but not quite as much weakness in services month-to-month as seemed to be indicated in the Markit survey from yesterday. Still, the IFO and Markit surveys seem to be broadly on the same page for the German economy in September. If we rank the IFO market indexes on the same timeline, the Germany ranking for manufacturing is stronger in the Markit survey and the ranking for the services sector is about the same in both surveys.

The IFO index and its two principal components, the current index and expectations index, all improved in September. The sector responses showed an improvement in manufacturing and some weakness in services but not quite as much weakness in services month-to-month as seemed to be indicated in the Markit survey from yesterday. Still, the IFO and Markit surveys seem to be broadly on the same page for the German economy in September. If we rank the IFO market indexes on the same timeline, the Germany ranking for manufacturing is stronger in the Markit survey and the ranking for the services sector is about the same in both surveys.

Ranked on data since 1991, the climate readings are above their medians (rank >50%) in all sectors except services (13.1%) and manufacturing (36.1%). The construction sector followed by retailing continue to be the two strongest sectors with reading standings in the top 20% of their respective queues of readings. Wholesaling has a 55.8 percentile standing. For climate overall, the standing is in its 54.6 percentile. The overall reading for the current business situation has only a 16.9 percentile standing while expectations overall have a higher 37th percentile standing. Expectations are leading the way higher.

Expectations show the brightest reading for manufacturing which has a standing in its 92.3 percentile. Its expectations diffusion value is 17.6 in September, a sharp contrast to its -16.6 value in the current survey for September. Manufacturing has been lagging; now it is expected to be catching up. All the other sectors have expectations values that lie below their respective historic mean values (all below 50%). So while there are high hopes for manufacturing, that might be only to see it out of the doldrums rather than to turn the corner for real strength.

Right now Germany and much of Europe are seeing another wave of coronavirus infections. That could be playing a role in suppressing German expectations.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief