Global| Sep 17 2009

Global| Sep 17 2009Housing Starts Show Turns Across Regions

Summary

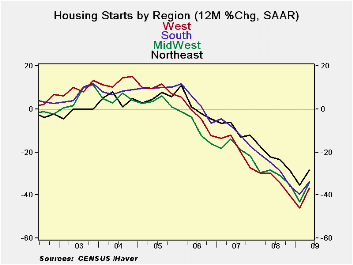

Yr/Yr regional housing markets all are still declining, of course, but the pace of the drop is diminishing across each of the main regions. The turn is clear but to keep it in gear will require more growth. With the first time home [...]

Yr/Yr regional housing markets all are still declining, of

course, but the pace of the drop is diminishing across each of the main

regions. The turn is clear but to keep it in gear will require more

growth. With the first time home buyer incentives coming off, home

purchases will find a greater challenge to hold the uptrend. It is a

good time to hold our breath and to wait and see how much of this turn

remains in place. Hopefully with the incentives off, a stronger economy

will provide the incentive for a lasting rebound in housing starts.

The table shows that the strength of the housing rebound is in

the single family sector where these purchase incentives play strongly.

For single family units, current strength is building momentum and

permits are steadily strengthening as well, despite the date with the

expiration for incentives.

The 2-4 unit sector is falling at an accelerated pace. Permits

are showing some lift nonetheless. Multifamily starts are still very

weak and despite that permits are improving.

Still the story of housing this month is that it was buoyed by

gains in the multifamily sector even though that sector has weak

trends. Single family starts fell sharply in the month. The small 2-4

unit sector also fell. This month growth was propped up by the sector

that has showed the least promise. The homebuilder survey released on

Sept 16th showed a one –point rise in that index. For the time being

housing retains its upward momentum, however slight.

| Housing Starts/Permits By Unit Size | ||||||||

|---|---|---|---|---|---|---|---|---|

| Analytical Comparisons (Pct. Changes-Not Compounded) | ||||||||

| Aug.2009 | ||||||||

| Total | One Unit | 2-4 Units | 5 or more | |||||

| In 000's of Units | Starts | Permits | Starts | Permits | Starts | Permits | Starts | Permits |

| This Month:Saar | 598 | 579 | 479 | 462 | 4 | 19 | 115 | 98 |

| Jul.2009 | 589 | 564 | 494 | 463 | 10 | 18 | 85 | 83 |

| Jun.2009 | 590 | 570 | 478 | 433 | 11 | 23 | 101 | 114 |

| 3-month avg. | 592 | 571 | 484 | 453 | 8 | 20 | 100 | 98 |

| 1-month % chg. | 1.5% | 2.7% | -3.0% | -0.2% | -60.0% | 5.6% | 35.3% | 18.1% |

| 3-month % chg | 8.5% | 11.8% | 17.1% | 13.8% | -55.6% | 5.6% | -13.5% | 4.3% |

| 6-month % chg | 4.2% | 5.3% | 34.2% | 21.3% | -69.2% | 11.8% | -43.6% | -35.5% |

| yr/yr % chg. | -29.6% | -32.4% | -21.7% | -15.7% | -73.3% | -44.1% | -48.2% | -64.4% |

| Drop from Max | -73.7% | -74.4% | -73.7% | -74.3% | -95.2% | -82.1% | -73.6% | -81.6% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief