Global| Mar 16 2004

Global| Mar 16 2004Housing Starts Fell Again

by:Tom Moeller

|in:Economy in Brief

Summary

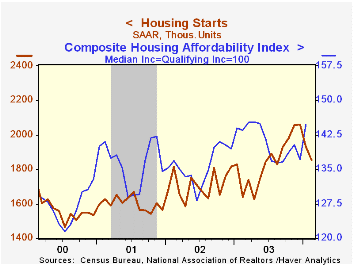

Housing starts fell 4.0% last month and added to the 6.3% drop in January. February starts of 1.855M were the lowest since last August. Consensus forecasts had been for 1.93M starts in February. Single family starts fell 4.1%, the [...]

Housing starts fell 4.0% last month and added to the 6.3% drop in January. February starts of 1.855M were the lowest since last August. Consensus forecasts had been for 1.93M starts in February.

Single family starts fell 4.1%, the third consecutive monthly decline.

Multi-family starts fell 3.4% and are off 9.9% during the last two months.

Starts were mixed across the country's regions last month. Housing starts fell hard m/m in the South (+10.5% y/y) and also were down in the West (+4.1% y/y). Starts rose 25.3% m/m in the Northeast (32.4% y/y) and rose in the Midwest (+25.1% y/y), recovering from the January cold snap.

Building permits fell a moderate 1.5% m/m (+6.6% y/y) for the second month.

| Housing Starts (000s, AR) | Feb | Jan | Y/Y | 2003 | 2002 | 2001 |

|---|---|---|---|---|---|---|

| Total | 1,855 | 1,932 | 13.1% | 1,848 | 1,711 | 1,601 |

| Single-family | 1,489 | 1,553 | 13.5% | 1,501 | 1,364 | 1,272 |

| Multi-family | 366 | 379 | 11.6% | 347 | 347 | 330 |

| Building Permits | 1,903 | 1,932 | 6.6% | 1,831 | 1,750 | 1,637 |

by Tom Moeller March 16, 2004

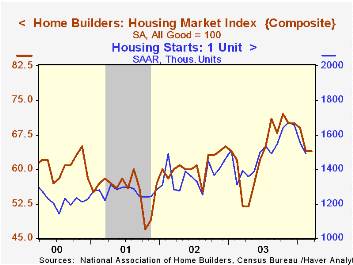

The Composite Housing Market Index reported by the National Association of Home Builders (NAHB) was unchanged in March at 64 versus February which was revised down slightly. It was the lowest level for the index since last June.

During the last fifteen years there has been a 79% correlation between the y/y change in the NAHB index and the change in single family housing starts.

The sub index which measures expected home sales in six months fell to the lowest level since June.

The index of current market conditions for home sales fell 2.8% m/m to 69 (+16.9% y/y).

Traffic of prospective buyers rose slightly m/m in March but still was off 12.7% from the August peak.

The NAHB index is a diffusion index based on a survey of builders. Readings above 50 signal that more builders view conditions as good than poor.

Visit the National Association of Home Builders using this link.

| Nat'l Association of Home Builders | Mar | Feb | 3 '03 | 2003 | 2002 | 2001 |

|---|---|---|---|---|---|---|

| Composite Housing Market Index | 64 | 64 | 52 | 64 | 61 | 56 |

by Tom Moeller March 16, 2004

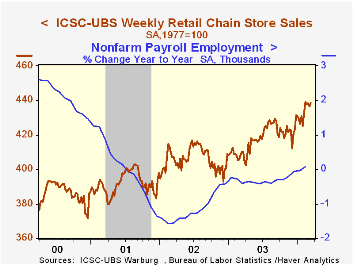

Chain store sales rose a modest 0.5% last week and recovered all of the prior week's 0.3% dip, according to the ICSC-UBS survey.

Sales so far in March are up 0.2% versus the February average.

During the last ten years there has been a 59% correlation between the year-to-year percent change in the ICSC-UBS measure of chain store sales and the change in non-auto retail sales less gasoline.

The ICSC-UBS retail chain-store sales index is constructed using the same-store sales reported by 78 stores of seven retailers: Dayton Hudson, Federated, Kmart, May, J.C. Penney, Sears and Wal-Mart.

| ICSC-UBS (SA, 1977=100) | 03/13/04 | 03/06/04 | Y/Y | 2003 | 2002 | 2001 |

|---|---|---|---|---|---|---|

| Total Weekly Retail Chain Store Sales | 438.6 | 436.6 | 7.0% | 2.9% | 3.6% | 2.1% |

by Tom Moeller March 16, 2004

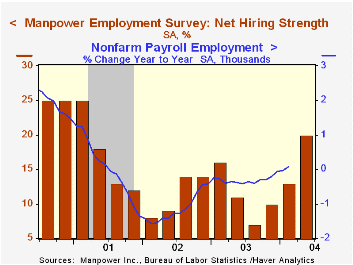

The Manpower survey of hiring intentions in the US for 2Q04 improved sharply. A seasonally adjusted net 20% of 16,000 employers expect to increase hiring activity. It was the highest level for hiring intentions since 1Q 2001.

The latest reading is up from 13% in 1Q and from 7% in 3Q03. Hiring typically picks up in 2Q, therefore seasonal adjustment factors damped the increase in the seasonally adjusted index.

Since 1980 there has been a 75% correlation between the Manpower index and the y/y change in non-farm payrolls.

The latest press release from Manpower Inc. covering employment prospects in North America can be viewed here.

| Manpower Employment Survey | 2Q04 | 1Q04 | 2Q03 | 2003 | 2002 | 2001 |

|---|---|---|---|---|---|---|

| All Industries - Net Higher (SA) | 20 | 13 | 11 | 11 | 11 | 17 |

by Tom Moeller March 16, 2004

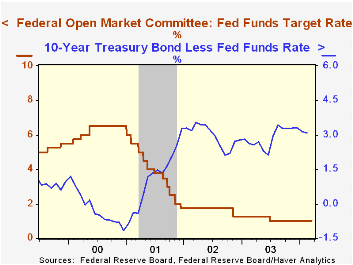

As expected, the Federal Reserve left the target rate for federal funds unchanged at 1.00%. The discount rate also was left unchanged at 2.00%.

The decision was unanimous.

The press release which accompanied the Fed's action indicated that "The evidence accumulated over the intermeeting period indicates that output is continuing to expand at a solid pace. Although job losses have slowed, new hiring has lagged."

Regarding inflation, the Fed indicated that "The probability of an unwelcome fall in inflation has diminished in recent months and now appears almost equal to that of a rise in inflation. With inflation quite low and resource use slack, the Committee believes that it can be patient in removing its policy accommodation."

The complete text of the Fed's latest press release can be found here.

"How the Fed Affects the Economy: A Look at Systemic Monetary Policy" from the Federal Reserve Bank of Philadelphia is available here .

"Macroeconomic Principles and Monetary Policy" from J. Alfred Broaddus, Jr., President of the Federal Reserve Bank of Richmond can be found here.

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief