Global| Dec 14 2017

Global| Dec 14 2017Highest EMU and German PMI Readings Since 2011

Summary

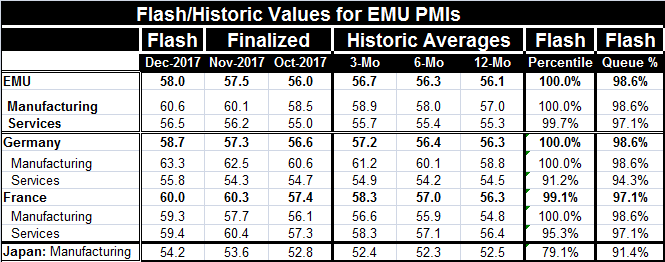

Both sectors are rising but manufacturing is clearly on a tear The Markit PMIs are strong again as all headline and sector readings in the table are in the top 10% of the group of readings released since January 2012. Headline, goods, [...]

EMU and Germany Gain While France Takes Small Step Back; Central Bankers Conclude Their End-of-Year Jubilee and Shine a Light on the Future

Both sectors are rising but manufacturing is clearly on a tear

Both sectors are rising but manufacturing is clearly on a tear

The Markit PMIs are strong again as all headline and sector readings in the table are in the top 10% of the group of readings released since January 2012. Headline, goods, services, EMU, German, French, or Japan manufacturing - all cuts at growth assessment- all are in exquisite form. French, German and EMU manufacturing are all on their highest readings since January 2012. The sequential moving averages for the EMU PMI as well for its two sectors are showing steady advancement with stronger readings over sequentially shorter periods. All headline and sectors in the EMU and its two largest members show this same sequential push to higher ground with the exception of the German services sector that does sag with weaker reading over six months than over 12 months but then recovers its momentum as its three-month average rises above even its 12-month average.

Europe does appear to be gaining momentum and solidity to its expansion. A report from the European Automobile Manufacturers' Association showed Thursday that passenger car registrations grew 5.9% year-on-year in November, the same rate as in October. This is a good solid gain and an important aspect of consumption.

China also added some data to the mix today as its retail sales in November gained by 10.2% over November 2016 and China's industrial production rose by 6.1% also over its year-ago value. Both series logged the sorts of gains that had been expected of them.

Central bankers meet

It was day for central banks to put a cherry on top and finish off their year's work. European stocks are off on the day in the wake of all the actions and bond yields are mostly higher, too. Yesterday stocks has reacted well to the news of the expected 25-basis-point Federal Reserve rate hike and to the report that the Republicans had an agreement on their pending tax deal.

The two main central bank actions today by the European Central Bank and the Bank of England saw bankers marking time. The Swiss National Bank also met and stayed on hold along with central banks of Turkey, the Philippines, Norway and PBOC.

BOE and BOJ: In its last meeting the BOE had hiked rates for the first time in a decade back in November. Despite that, in this meeting, the BOE stood down from a rate hike agenda and kept all aspects of policy on an even keel. The BOE faces one of the most difficult tasks of any of the major monetary center banks at this time as current data show there is and has been an inflation overshoot. But the U.K. is engaged in ongoing Brexit negotiations and the U.K. economy is expected to be weaker in the wake of its Brexit deal. What should the BOE do? Perhaps the only central bank with any sort of similar challenge is the Bank of Japan that is fighting powerful structural forces of demographics and a huge debt load while it is trying to put the risk of deflation down for good and, like every other central bank, hit its inflation target. In the meantime, the U.K. faces data that have continued to be strong with inflation overshooting and unemployment at its lowest mark since the mid-1970s. Retail sales, apparently, are on solid footing and with a good Christmas shopping season in hand. However, also giving the BOE some latitude is the fact that wages continue to lag inflation. Despite what might appears to be full employment, wage pressures are not an issue and the actual labor market condition in the wake of Brexit and what will be substantial jobs losses is also a matter of some uncertainty. Faced with all those issues, risks and choices, the BOE decided to mark time.

ECB: The ECB, too, had announced at its previous meeting in November that it would be reducing its asset purchases beginning in 2018; it has followed that move with a decision to stand pat in December on its past policy path. The ECB Governing Council, headed by ECB President Mario Draghi, left the key interest rates unchanged in its final policy-session for this year. The main refi rate is currently at a record low 0% and the deposit rate at -0.40%. The marginal lending facility rate is 0.25%. The ECB reiterated its statement that it expected key interest rates to remain at their current levels for an extended period of time and for that to run 'well past' the ending of its program of net asset purchases. Most private forecasters are not looking for rate hikes until 2019.

The PBOC...can we call this a rate hike? China's central bank unexpectedly lifted its rates in its open market operation on Thursday after the Federal Reserve tightened its policy rates. Chinese economic data released on Thursday showed that industrial production growth weakened in November (as expected) as measures taken to control pollution took a toll. Meanwhile, retail sales grew as expected at pace near 10%. The People's Bank of China raised its 7-day and 28-day reverse repo rates by 5 basis points to 2.50% and 2.80%, respectively. A similar action was last taken in mid-March. The bank raised the rate on its medium-term lending facility by 5 basis points to 3.25%. I cannot fathom what a 5bp rate hike means or why a central bank would bother with such a miniscule move. Possibly it is meant to signal that more aggressive hikes are possible. There is no doubt that the PBOC lives in its own world and does things its own way.

Central bank forecasts?

The ECB did raise its growth and inflation forecasts on Thursday. Growth next year is now seen at 2.3% versus an earlier 1.8% forecast. Growth in 2019 is expected to slow to 1.9% and then slow further to a pace of 1.7% in 2020. Inflation is expected at 1.5% in 2017 and to stay below target even slowing to 1.4% in 2018. The 2019 pace is expected to pick up to 1.5% and then to step up again to 1.7% by end-2020 (ECB forecast table here). Today the German research institute, the IFO, also presented an outlook for Germany that sees a significant bump up in growth for the year ahead; the IFO is shifting its forest for German growth up to 2.6% from 2% where it had been previously. Yesterday the Fed had released its SEP (summary of economic projections) which I refer as 'policycasts' instead of forecasts. The SEP process is peculiar. Fed members have to submit their outlooks which contain each member's views of how rates will respond over the period out to 2020. I don't so much call these forests because they somewhat oddly force each member to keep the Fed on its policy track so that by 2020 each forest has to end up with 'low' unemployment and about 2% inflation. It is a bit of backwards way of making a forecast, but it fits the Fed's purposes. Still, the trimmed median of the submitted policycasts of Fed members showed about the same rate profile as in the past, the same inflation tracking, but like the ECB, stronger growth

On balance, between the Fed, and the ECB the world is projected to be a pretty tranquil place over the next few years. Of course, the BOE is dealing with the most bumps in the road with inflation that is much higher than in the U.S. or in the euro area and with some real question marks about how growth will evolve. However, the U.S. and EMU are well settled on their low inflation outlook and also on a period in which growth is going to pick up significantly. That environment should help the U.K. and the BOE.

Summing up

It is interesting that the view on inflation has remained so contained despite this now-synchronized global growth cycle and despite the pick-up in growth that is underway rather broadly in the context of that cycle. But the U.S. has been raising rates (albeit slowly) for about two years now; the BOE has just begun to withdraw at least some stimulus and the ECB plans to start its trimming of securities purchases beginning in 2018. All of this amounts to some degree of leaning against the improved thrust of global growth. At the same time, despite excellent unemployment conditions in the U.S., the U.K., and Germany, as well as, improving trends in the EMU area, wages generally have continued to lag inflation and continue to be less affected by the state of the local labor market and by the local environment for inflation than in the past. The global forces of technology and the force of stepped up trade competition are still at work after all. Despite a very positive tranquil and reassuring set of projections from the Fed and the ECB, for the period ahead what remains to be seen is what really will happen. With central banks even the best laid plans sometimes go awry. For now we can bask in the glow of a warm and friendly outlook. But with so many trends shifting and so many geopolitical relations under stress it's also a good time to remain wary of what the future will bring.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief