Global| Sep 29 2017

Global| Sep 29 2017HICP Inflation Keeps Toothpaste in the Tube but Begins to Show Divergences

Summary

EMU gained only 0.1% in September and the year-on-year pace accelerated slightly to 1.6% from 1.5%. The core, however, rose by 0.1% and logged a drop in its year-on-year pace to 1.2% from 1.3% previously. On this report the ECB does [...]

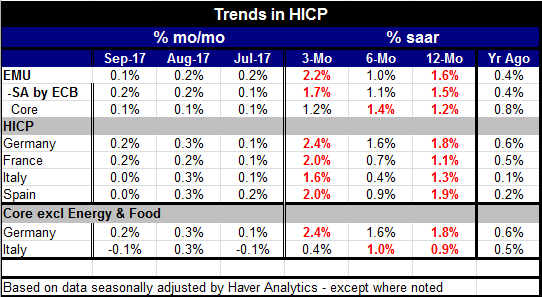

EMU gained only 0.1% in September and the year-on-year pace accelerated slightly to 1.6% from 1.5%. The core, however, rose by 0.1% and logged a drop in its year-on-year pace to 1.2% from 1.3% previously. On this report the ECB does not seem to be closer to meeting its inflation goal.

EMU gained only 0.1% in September and the year-on-year pace accelerated slightly to 1.6% from 1.5%. The core, however, rose by 0.1% and logged a drop in its year-on-year pace to 1.2% from 1.3% previously. On this report the ECB does not seem to be closer to meeting its inflation goal.

The sequential growth rates for inflation in EMU under core vs headline schemes show that over three months inflation is higher for the headline compared to six months but is lower for the core. Over six months all measures of inflation are quiescent and over 12-months all are well below the ECB target rate. Three month inflation is higher than 12-month inflation for the headline but it is at the same low, 1.2% pace, for the core.

Turning to the individual large country-reported inflation data we find that three of the four largest EMU economies have inflation on the borderline or at an excessive pace over three-months. German inflation is over the top at a 2.4% pace while Spanish and French inflation at a 2% pace are marginally above the target which is expressed as a pace just less than 2%. Italy in fact at a 1.6% pace is still undernourished. Over six months all the large country headline rates of inflation are too low. Germany logs the fastest gain at a 1.6% pace, Spain is next at 0.9%, followed by France at 0.7% and Italy at 0.4%. Obviously on a six month time line there are very weak inflation pressures here. Over 12-months Spain logs a near target 1.9% pace, with Germany at a 1.8% pace, but France falls well short at a 1.1% pace and Italy falls short, too, with a 1.3% pace.

Inflation simply does not seem to be building any consistent momentum in EMU. The economic data have been showing some firmness and that has been rewarding. But growth is not being accompanied by inflation to much of a degree. Another aspect to keep in mind is that the strongest growth signals have come from PMI data. The signals from conventional economic indicators have not been anywhere near as strong as from the PMI reports and other sorts of surveys. However, one thing is clear and that is that the Germany is doing better than the rest of EMU and that is reflected in its relatively higher rate of inflation for the most part. The German harmonized rate of unemployment is at 3.7% whereas for all of EMU it is at 9.1 percent as of July. The German advantage is even greater when compared directly to the largest EMU economies (France 9.8%, Italy 11.3% and Spain 17.1%) Germany today also reported another drop in its unemployment rate to a new reunification low. Its fresh retail sales gauge showed sales growing at a steady 2.8% annual rate.

There are early observations on core inflation for Italy and for Germany if we use the domestic CPI instead of the HICP for Germany. In Sept Italy's core rate logged a -0.1% change while the German core rose by 0.2% after gaining 0.3% in August. Over three-months Germany shows the core up at a 2.4% annual rate while the Italian core is up at a 0.4% pace. But over other horizons core inflation is better behaved. Over six-months the German rate is at a 1.6% pace with the Italian rate at 1.0%. Over 12-months the German rate is closer to ECB target pace at a 1.8% rate but in Italy the core is only up at a 0.9% pace.

There does seem to be some separation in the inflation rates emerging from EMU members. Interestingly among this group of countries Germany has tended to be the high inflation country while either France or Italy have been the low inflation countries. This is the opposite sort of result to what we have expected and observed over most of the EMU's existence it is what has happened since Italy and France have been under strong pressures to reduce or contain debt and its growth. Meanwhile, Germany has been the consistently strongest economy in EMU during this period of an economic lull. This might be considered as a less that optimal result for EMU from the standpoint of stability since Germany has the greatest fear of inflation and on this trend, as EMU-wide inflation creeps closer to target the German inflation rate will surpass 2% first and lead to criticisms in Germany and uneasiness at the Bundesbank. This pressure probably will manifest itself as more leverage on the ECB to pay attention to where inflation might be pointing rather than to where it is. In that respect it could cause the ECB to make policy more off of inflation forecasts as the Fed has been doing although with not much success.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief