Global| Aug 19 2005

Global| Aug 19 2005Growth Continues through July in Russia's "Five Basic Indicators"

Summary

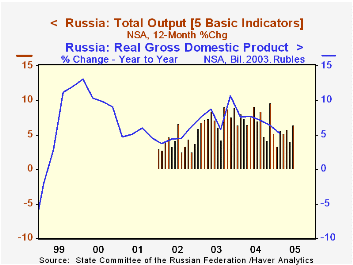

The Russian economy has maintained a firm uptrend through the summer, according to the "Five Basic Indicators", measures of output in leading goods-related sectors. In June, the combined output gauge was up 6.4% from a year earlier, [...]

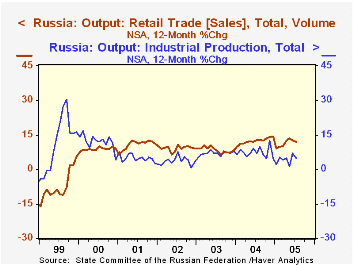

The Russian economy has maintained a firm uptrend through the summer, according to the "Five Basic Indicators", measures of output in leading goods-related sectors. In June, the combined output gauge was up 6.4% from a year earlier, stronger than May's 4.1% and last year's 5.2%. The component items for July, although not the total index, were reported this week, several of them today by the Federal Service of State Statistics, and they suggest that the momentum may have slowed somewhat. These indicators cover agriculture, industrial production, retail trade, construction and transportation. The data, contained in Haver's EMERGECW database, are not seasonally adjusted and are reported as year-on-year percentage changes. The industrial production segment gained 4.9% in July, compared with 6.9% in June and 4.6% in 2004. Retailing kept up double-digit gains, although these are a bit slower than they were during 2004. Construction and agricultural activity, by contrast, picked up considerably in July after a sluggish pace in the spring. Transportation was quite vigorous in 2002 and 2003, but has had only modest increases since then.

The volume increases in retail trade are perhaps most impressive. Russian consumers are evidently able to raise their purchasing, despite double-digit increases also in consumer prices. And since retailing is expanding so much more rapidly than industrial activity, we'd surmise that inventories are tight and that imports are continuing to flow in rapidly. Through the second quarter, total imports of goods were up 28.5% from their year earlier pace (before adjustment for inflation).

The rapid inflation makes it difficult to be unabashedly optimistic about a sustained expansion for the Russian economy, but the persisting advances in goods-producing sector output volume are encouraging. Russia's status as an oil exporter also means that rising energy costs are partially offset by the support energy sales give to incomes and profits for those employed in that sector.

| Russia: Year/Year % Changes |

July 2005 | June 2005 | May 2005 | December/December|||

|---|---|---|---|---|---|---|

| 2004 | 2003 | 2002 | ||||

| Output | -- | 6.4 | 4.1 | 5.2 | 8.9 | 3.8 |

| Industrial Production | 4.9 | 6.9 | 1.4 | 4.6 | 7.9 | 3.2 |

| Retail Trade | 11.8 | 12.5 | 13.3 | 14.2 | 8.4 | 9.2 |

| Construction | 12.9 | 7.4 | 5.3 | 10.6 | 16.6 | 3.8 |

| Transportation | 2.8 | 2.0 | 4.1 | 3.4 | 9.4 | 9.5 |

| Agriculture | 4.5 | 0.4 | 0.8 | -0.7 | 0.6 | -0.2 |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief