Global| Mar 24 2005

Global| Mar 24 2005Good Gains in Japanese Service Sector: Genuine or Just Statistical?

Summary

Service sector activity in Japan advanced vigorously in January, according to the report on "Tertiary Industry Activity" published today by the Ministry of Economy, Trade and Industry (METI). The index for all industries rose from [...]

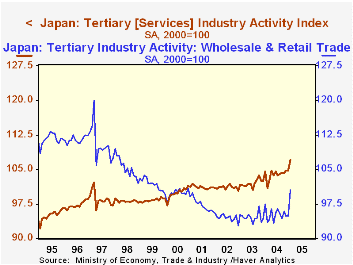

Service sector activity in Japan advanced vigorously in January, according to the report on "Tertiary Industry Activity" published today by the Ministry of Economy, Trade and Industry (METI). The index for all industries rose from December's 104.7 (2002=100) to 107.0, or 2.2%; the gain from the year-earlier level was 2.5%.

Participation by various industry groups varied widely, as illustrated in the table below. Wholesale and retail trade was up 5.9% and financial services by 2.9%, but information and communication dropped 7.9%. Most other sectors showed some increase, generating the rise in the overall total.

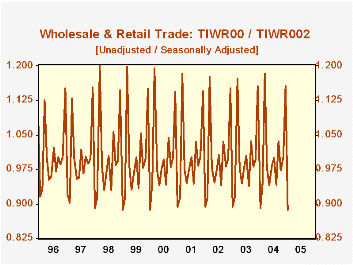

Before we conclude that the Japanese economy has shifted onto a new vigorous growth path, we need to take account of what might be called the "January effect" regarding seasonality. As in many countries, economic activity in Japan strengthens in December and weakens significantly in January, with a commensurate rise in the seasonal factor for December and a steep decline in January. This means that a seasonally adjusted "gain" in January could actually be a statistical construct; in fact, the unadjusted all-industry index fell 11.3% from December, at a time when the seasonal factor presumes a 13.3% drop, so that after seasonal adjustment, the index increased on the order of 2%. The trade industries are a sub-sector where this occurs most distinctly; that seasonal factor declines about 23% in January, so that any year in which January sales activity falls by "just" 22% will show a nice seasonally adjusted rise for January. ["Seasonal factor" in this discussion is the implicit seasonal derived from dividing the unadjusted by the adjusted data. See the second graph for an example.]

This extreme movement in seasonality can easily exaggerate the strength of an activity that simply doesn't fall as much as the seasonal statistics anticipate. The low level of the seasonal factors then mean that the unadjusted data are magnified more than in other months, yielding out-sized gains. These may indeed indicate genuine progress in economic activity, but they might also be a fluke; if so, they will wash out, generally during the spring months when the seasonals expect a normal growth pace that may not be matched by the actual performance. Growth, supported in the winter, might then weaken noticeably during the spring. Such patterns occur often in the US, as well, particularly with housing and construction data.

| Index, 2002=100, SA | Jan 2005 | Dec 2004 | Year Ago | 2004 | 2003 | 2002 |

|---|---|---|---|---|---|---|

| All Industries | 107.0 | 104.7 | 104.6 | 103.9 | 102.0 | 101.1 |

| Information & Communication | 111.3 | 120.9 | 114.6 | 114.3 | 114.5 | 113.1 |

| Wholesale & Retail Trade | 100.4 | 94.8 | 97.5 | 95.1 | 94.5 | 94.5 |

| Finance Services | 111.7 | 108.5 | 108.0 | 109.2 | 104.2 | 102.7 |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief