Global| Oct 04 2018

Global| Oct 04 2018Global Services Show Wear and Tear

Summary

While attention is riveted on trade wars and manufacturing sector results, the global service sector has been gradually losing momentum. And while it has not slipped by unnoticed, the geopolitical scene is worsening importantly as [...]

While attention is riveted on trade wars and manufacturing sector results, the global service sector has been gradually losing momentum. And while it has not slipped by unnoticed, the geopolitical scene is worsening importantly as well, and in ways that do not seem to be fully appreciated. It is important not to lose sight of the forest because you are inspecting the trees too closely.

While attention is riveted on trade wars and manufacturing sector results, the global service sector has been gradually losing momentum. And while it has not slipped by unnoticed, the geopolitical scene is worsening importantly as well, and in ways that do not seem to be fully appreciated. It is important not to lose sight of the forest because you are inspecting the trees too closely.

Forgiven but not indemnified...

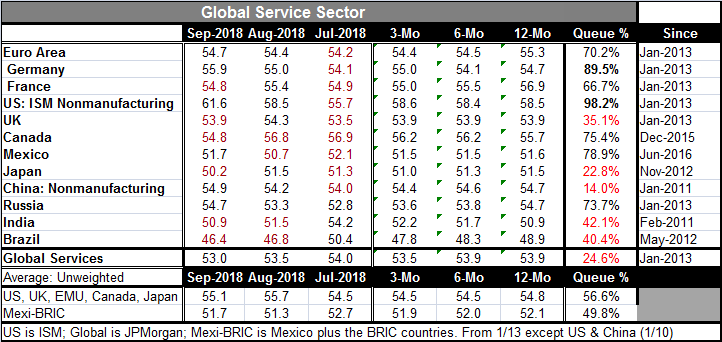

You are forgiven if you live in the U.S., wear blinders, and mostly see U.S.-side reports. The U.S. ISM nonmanufacturing index, released yesterday for September data, was a knock-your-socks-off explosively strong report that came out of the blue. It is not representative of global growth in any way, shape, or form. U.S. markets are still in a state of shock from it. Still, it’s only one month and the signaling value of such an unexpected one-month report remains unclear (especially that one for a report that maps poorly into every statistic we have related to the nonmanufacturing sector). What is clear is that globally services are in a funk and that U.S. economic performance is no bellwether for the global economy.

The JPMorgan global services PMI at 53.0 in September has a 24.6 percentile rank standing. That means it has been weaker since 2013 only about one-quarter of the time. And this five-year period we use for evaluation was no golden age of growth.

Moreover, the current level of the global services index at 53.0 is weaker month-to-month and has weakened month-to-month for three months running. The index’s six-month and 12-month averages are identical. But its three-month average is weaker than both and the September reading is also below the three-month average.

The chart shows the different paths of the services PMIs for the U.S., EMU, Japan, and China. Only the U.S. index (nonmanufacturing, like China) has moved up and even there, without the spurt in September, there would likely be some legacy of weakness judging from the trend of the months prior to September. From the chart, we have reason to have some concerns about the global economy, especially Asia, where weak readings have proliferated beyond just China and Japan for months.

The services sector is the backbone for most economies even those with very important industrial sectors. Manufacturing productivity has advanced so far and technology is becoming even more important, so that increasingly jobs are the province of the services sector. And jobs mean income and income fuels spending. So a slowdown in services is an important phenomenon globally and not one associate with economic pickup.

At the same time, a new risk has emerged as U.S. sanctions on Iran are creating pressure on the international oil market; here talk has turned to the prospect for $100/barrel oil again.

And with all the economic data jostling back and forth, central banks making plans then re-loading, Brexit in full bloom, business cycle readings shifting, there are geopolitical events that bring important issues to bear on the economic future just as U.S. sanctions on Iran are helping to lift oil prices.

In this regard, huge stories on the day include a Bloomberg (here) story about how Chinese subcontractors have implanted on a mother board, eventually used by Amazon, Apple and the U.S. Defense Department (yes, THAT U.S. Department of Defense), a chip that allows it to circumvent the security of any system in which it is used. Separately, the Dutch caught the Russian hackers trying to use cyber methods to break into the Organization for the Prohibition of Chemical Weapons. The U.S. government on Wednesday warned U.S. firms of another group linked to China that has been launching cyber security attacks geared to steal information.

This is not a very favorable back ground against which to think that the U.S. and China are going to easily patch up their trade differences. And yesterday’s close call between a U.S. ship in the South China Sea with a Chinese vessel is just another way the U.S. and China are making their hardened uncompromising opposite positions on the South China Sea known. Yesterday, U.S. Vice President, Mike Pence, issued a statement saying that the U.S. will not be intimidated in the South China Sea.

It is hard to see how negotiations with China proceed smoothing in the wake of these disclosures and the Trump Administration’s demand that China stop stealing U.S. technology and making technology turnover a condition of doing business in China when it is clear that China has been infiltrating all sorts of technology on such a wide and deep scale already.

While the global bond markets are still feeling the reverberations from the heavy weight dropped on them and the reaction to yesterday’s nonmanufacturing report, it should be clear that as important as that sector is, it’s only part of the story and only one month’s observation. To the extent that the U.S. ‘exports’ higher interest rates due to a market reactions to its wholly domestic ISM report, it puts further downward pressure on a global economy that is not in much of a position to stand up under that pressure. If ever there were a case for global transmission forces to short-circuit, this would be one. But the global linkages seem to be more ‘Pavlovian’ than perceptive.

We appear to be going headlong into a very difficult disequilibrium. It is distortive for U.S. rate hikes to push up rates overseas under these conditions. It may be disruptive for U.S. rates themselves to rise in a situation where U.S. inflation is not going up and where an overreaction to one report puts the bond market back on its heels. Federal Reserve Chair Jerome Powell may have a ‘remarkably positive outlook’ for the U.S. economy, but I remain critical for all my usual reasons. These are that one cannot analyze the U.S. economy by stopping at the border. The global economy matters. Ignoring the tensions on the global economy to focus on a one-month ‘trend’ in the U.S. economy simply does not make any sense. It is a good time to issue a warning about this. I offer this observation: if it seems too good to be true, it may only be temporary. And I also offer this: international linkages eventually rationalize themselves. So you have to ask yourself: are they are now rationalizing foreign rates to accord with the U.S. experience and will they later realign to the needs of the global experience?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief