Global| Jun 05 2017

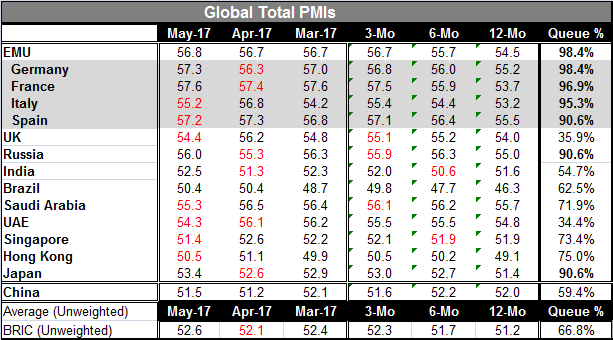

Global| Jun 05 2017Global PMIs Show Some Mixed Trends; All Composite PMIs in the Table Show Growth in May

Summary

All the composite PMI gauges in the table show growth in May. This is the second month in a row for which this is true. In March Hong Kong showed contraction; in February, Brazil and Hong Kong showed contraction. Still, out of the 14 [...]

All the composite PMI gauges in the table show growth in May. This is the second month in a row for which this is true. In March Hong Kong showed contraction; in February, Brazil and Hong Kong showed contraction. Still, out of the 14 entries in the table, seven show backtracking in May. This is up from six in April. This indicator of slowdown is relatively new since PMI data have been among the most upbeat in recent months. Over three months only three entries (U.K., Russia and Saudi Arabia) show a weaker three-month average reading than a six-month average reading. Over six months only India and Singapore are low compared to their 12-month average and for Singapore 'rounding' the PMI to one decimal place leaves it flat on the smoothed comparison. The rest of the entries show continual improvement based on their averages from 12-month to six-month to three-month. But six entries still do show a different type of slowing is in progress: Italy, the U.K., Saudi Arabia, the U.A.E., Singapore, and China each have a current reading lower than their respective three-month average.

All the composite PMI gauges in the table show growth in May. This is the second month in a row for which this is true. In March Hong Kong showed contraction; in February, Brazil and Hong Kong showed contraction. Still, out of the 14 entries in the table, seven show backtracking in May. This is up from six in April. This indicator of slowdown is relatively new since PMI data have been among the most upbeat in recent months. Over three months only three entries (U.K., Russia and Saudi Arabia) show a weaker three-month average reading than a six-month average reading. Over six months only India and Singapore are low compared to their 12-month average and for Singapore 'rounding' the PMI to one decimal place leaves it flat on the smoothed comparison. The rest of the entries show continual improvement based on their averages from 12-month to six-month to three-month. But six entries still do show a different type of slowing is in progress: Italy, the U.K., Saudi Arabia, the U.A.E., Singapore, and China each have a current reading lower than their respective three-month average.

The U.S. readings show some sense of cross currents. For the U.S. this month the Markit composite index improves slightly, but the ISM index weakens despite a very small uptick in manufacturing as the nonmanufacturing sector index falls by 0.6 tenths of a point. But the U.S. composite does break lower over three months compared to six months (looking at averages) for both the ISM and the Markit index. Yet, both composite gauges show that the current month's reading is above its three-month average, signaling still positive near-term momentum. But looked at by sector, the U.S. manufacturing sector is slipping in May relative to its three-month average in both the Markit and PMI frameworks.

Another interesting feature of the day's data is that the 90th percentile queue standings (of which there are seven in the table), all belong to highly developed economies not to the developing economies. The EMU, Germany, France, Italy, and Spain as well as Russia and Japan make up the countries in the top 10% of their respective queue standings or better. On this list, Russia is the only odd member. The weakest readings for now are in the mid-30th percentile decile and belong to the U.K. and the U.A.E.

The BRIC countries taken as a whole have an unweighted standing in their 66th percentile (barely top one-third of its historic queue). Brazil has a 62nd queue percentile standing. India has a 54th percentile standing. China has a 59th percentile standing.

Of course, the economic data do not exist in isolation. There are a number of geopolitical confrontations that make the world a more complicated place and may also be adversely affecting economic relationships. Russia is still under Western sanctions for its dealing with Ukraine and seizure of Crimea. Yet, the U.S. is trying to 'work with' Russian in the Middle East to solve the Syria problem while at the same time trying to resolve the question of Russian involvement in the U.S. elections as well as with some current or former Trump staffers. North Korea is working apace to develop and perfect a deliverable nuclear bomb. It periodically shoots test missiles all across the local seas. The U.S. has asked for China's help to stem this ambition. Yet, China seems to have had little success at that and has urged that no one destabilize the Korean peninsula. The U.S. and China have set their trade differences aside (at least for now), but the U.S. continues to challenge China's South China Sea claims, which it refuses to recognize. Several Middle Eastern countries have broken off ties with Qatar over its refusal to distance itself from terrorism. Iran is angry over this and blames the U.S., especially Donald Trump and his recent visit. Yet, the Middle Eastern countries still have a mutual interest through their membership in OPEC and mutual desire to steer energy prices. The U.K. is grappling with Brexit, oncoming British elections, a tough line from the EU and a recent terror attack. The U.S. is trying to get more participation out of its NATO allies but that has alienated them to some extent and also is engaged in trying to calm European nerves about where the U.S. stands. All of these relationships/events have the power to weigh on economic growth.

Looking at growth, what we see are slow-going but generally positive trends. There is some evidence of some near-term backtracking. Still, growth is in gear even if monetary policies remain stuck on stimulative and central banks continue to wonder what normalization will look like and when it might present itself. There are a lot of tangled economic and geopolitical issues that the global economy could stumble over. It's not a good time to take anything for granted.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief