Global| Apr 06 2015

Global| Apr 06 2015Global Economy's Manufacturing Sector Struggles

Summary

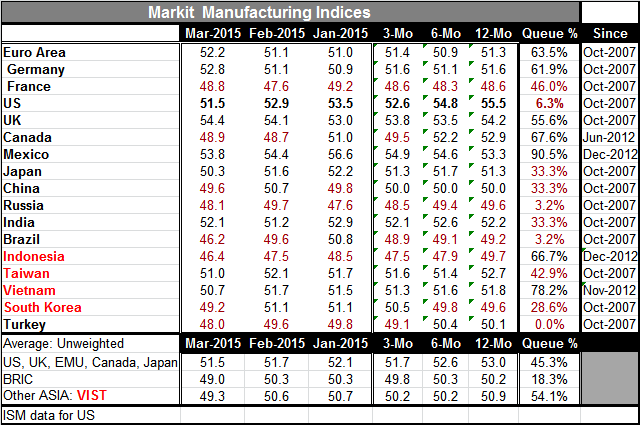

Globally the manufacturing sector is struggling. In March, 11 of the 17 countries/units in the table showed declines their respective manufacturing PMIs. Moreover, 8 of these 17 entities have PMI readings below 50, indicating [...]

Globally the manufacturing sector is struggling. In March, 11 of the 17 countries/units in the table showed declines their respective manufacturing PMIs. Moreover, 8 of these 17 entities have PMI readings below 50, indicating contraction.

Globally the manufacturing sector is struggling. In March, 11 of the 17 countries/units in the table showed declines their respective manufacturing PMIs. Moreover, 8 of these 17 entities have PMI readings below 50, indicating contraction.

In February, 9 of 17 readings fell month-to-month and six had PMI readings below 50. This is a good deal of sluggishness and weakness in manufacturing especially so far into an economic expansion period that continues to be weak by historic standards. The highest manufacturing PMI in this group is the U.K. in March at 54.4. Mexico at 54.4 was the highest in February. These are still rather modest readings.

Moreover, the queue standings are uniformly poor. In these we rank each country's PMI in its time series of historic values. The highest readings are for Mexico and Vietnam, two countries that only have compiled data since the fourth quarter of 2012. Among countries with observations back to late-2007, the euro area and Germany have the highest standings with each in their 60th percentile range. These are quite modest standings, especially so for the best in class. The U.S. sits in the bottom 6 percentile of its historic queue of data since October of 2007. The U.S. manufacturing PMI has been slipping steadily since August of last year. The strong dollar is not helping.

Japan, China and India all have manufacturing PMI readings at the edge of the lower one-third of their respective ranges. Turkey is at its low. Brazil and Russia are not far from their respective lows. These standings are all the more depressing since they are comparisons of current values with a period when these economies were in recession then transited into expansion. These are very weak readings for such a period.

Against this background, it is hard to understand the Fed's compulsion to hike rates. There are no capacity constraints in the U.S. or even in the global economy. Manufacturing everywhere is extremely weak. There has been a lot of monetary stimulus and the countries that did that early have fared better (the U.S. and the U.K.). But now that stimulus is wearing off and the stimulus launched in Europe is playing a part by driving the euro lower and the dollar higher.

The U.K. has the highest manufacturing PMI value in March followed by Mexico, Germany, the EMU, India and the U.S. The weakest scores are from Indonesia, Turkey, Russia and France.

The world economy faces a weak manufacturing sector. Europe is starting to pick up as EMU loan schemes are in play and QE has been announced and launched. But to the extent that these programs work through the exchange rate mechanism, they only rob Peter to pay Paul. No new growth is created globally by rearranging who is supplying the inadequate demand of the day.

The world economy finds itself with the same demographic features more or less globally as the world's population ages in the wake of two world wars more than half a century ago. There is also a legacy of excessive debt and a plan by central banks to control leverage and risk. This program restricts bank lending by using capital/asset ratios that bind and a stress test to enforce disciple. This approach doesn't just control; it also restricts lending and growth.

The fact is that the world economy has been reconfigured to have more of its output produced in Asia where savings rates are higher thereby blunting the multiplier effect on expansion. It is one of the reasons that the global economy is in a state of excess supply and still working out of a period of excess leverage. It is not exactly a prescription for stronger growth but economic conditions should become more solid under this plan as it plays out. But this is a plan to develop long-run stability not to enhance short-run growth. For now growth is slow and the threat of inflation rising is distant and it's being kept at bay through the tight regulation of banks. Do central banks truly understand the situation they have created? How is inflation at risk to low interest rates when central banks control lending so effectively? It's a question manufacturers will be asking themselves for a long time.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief