Global| Mar 26 2008

Global| Mar 26 2008Germany’s IFO Index Turns Up…Again

Summary

The IFO headline index rose to 104.08 in March from 103.1 in February. This rise marks the third straight increase from a low of 103 in December 2007. It comes at a time that the euro is moving relentlessly higher and policymakers are [...]

The IFO headline index rose to 104.08 in March from 103.1 in February. This rise marks the third straight increase from a low of 103 in December 2007. It comes at a time that the euro is moving relentlessly higher and policymakers are complaining about that. The quick rebound in the IFO index and apparent health it signals sires questions about the rest of Europe.

Germany’s current situation is improving for the second month in a row with the index up to 111.5 from 110.3 in February. Expectations also notched higher, rising for the second time in four months. Expectations are having a bit of a harder time of it. The expectations index edged higher to 98.4 in March from 98.2 in February

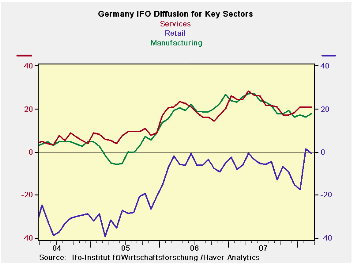

Germany’s sectors look fairy solid as the IFO diffusion gauges show in the table below. Construction is the weakest sector and it is in the 56th percentile of its range of values since 1991. Manufacturing is still the strongest sector in the 84th percentile of its range and services are strong in the 83rd percentile of their range. Wholesaling and retailing are in the mid 75th or so percentile of their respective ranges. This leaves Germany’s overall sector index in the 83rd percentile, hardly a weak showing.

If Germany is this resilient, is the rest of EMU going to have

more trouble? A strong Germany will tend to the keep the ECB tighter

longer. But Italian data have been decidedly weak with orders fading

and both consumer and business morale measures from ISAE on very weak

trends. EMU countries share a common currency but national inflation

rates have been quite different across EMU member countries ever since

the currency union was formed; it may be that competitiveness levels in

the EMUe are not on level playing field. That could cause a real

policy-making dilemma and worse political trouble within the union.

| Summary of IFO Sector Diffusion readings: CLIMATE | ||||||||

|---|---|---|---|---|---|---|---|---|

| Current | Last Month | Since Jan 1991* | ||||||

| Mar-08 | Feb-08 | Average | Median | Max | Min | range | % range | |

| All Sectors | 8.7 | 7.3 | -8.7 | -9.5 | 16.7 | -30.7 | 47.4 | 83.1% |

| MFG | 17.9 | 16.3 | -0.6 | 0.2 | 27.4 | -35.6 | 63.0 | 84.9% |

| Construction | -21.8 | -24.9 | -30.0 | -32.2 | 0.1 | -50.5 | 50.6 | 56.7% |

| Wholesale | 7.8 | 5.8 | -14.8 | -16.5 | 23.4 | -39.5 | 62.9 | 75.2% |

| Retail | -0.9 | 1.3 | -15.9 | -15.0 | 11.3 | -39.7 | 51.0 | 76.1% |

| Services | 21.0 | 21.0 | 9.5 | 8.9 | 28.5 | -15.7 | 44.2 | 83.0% |

| *May 2001 for Services | ||||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief