Global| Oct 26 2009

Global| Oct 26 2009Germany’s Consumer Climate Improves

Summary

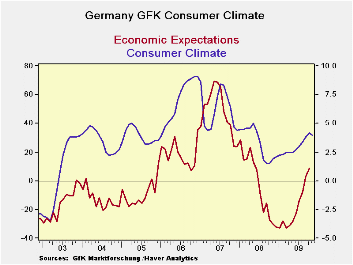

Germany’s GFK survey rose in October. It was a month-to-month rise of 0.4 for the third month in a row. The economic index rose by 5.2 points its smallest rise since May but on the heels of a 10.9 point spurt in September. Income [...]

Germany’s GFK survey rose in October. It was a month-to-month

rise of 0.4 for the third month in a row. The economic index rose by

5.2 points its smallest rise since May but on the heels of a 10.9 point

spurt in September. Income expectations fell by 3.1 points, the first

drop in five months but after two large gains. The propensity to buy

dropped back by 10.4 points a huge drop and the largest since a drop of

15.7 in May 2008.

Still the Climate index at +4.2 is above its average of 3.3.

All of these components are above their average values since 2002. The

‘income’ and ‘propensity to buy’ percentiles are stronger for the count

percentiles than for the range percentiles; the standing among past

observations is stronger than their range standing between the highs

and lows. This means that while the current readings are still well off

peak they are in the upper part of the distribution of readings and in

the upper region of normal.

The GFK index shows that confidence is still improving in Germany. Germans are relatively more worried about the economy in generally than they are impacted by expectations for income or buying power problems. Still the fact of the matter is that German consumption has not been very strong. And Germany’s Chancellor is out warning that in 2011 there will be another crisis and that unemployment will rise from current levels. I guess that Obama’s pessimistic approach to assessing the economy is spreading abroad.

| Germany Consumer Climate Survey GFK | ||||

|---|---|---|---|---|

| Climate | Expectations | Propensity to | ||

| Economic | Income | Buy | ||

| Oct-09 | 4.2 | 8.7 | 12.9 | 26.1 |

| Sep-09 | 3.8 | 3.4 | 16.0 | 36.5 |

| Aug-09 | 3.4 | -7.5 | 8.8 | 31.1 |

| Jul-09 | 3.0 | -14.0 | 1.8 | 25.1 |

| Jun-09 | 2.7 | -22.6 | -3.3 | 14.5 |

| Average | 3.3 | 0.9 | -3.8 | -9.6 |

| Max | 9.1 | 69.5 | 33.6 | 64.4 |

| Min | -3.5 | -32.9 | -24.5 | -55.4 |

| % range | 61.1% | 40.6% | 64.4% | 68.0% |

| Count% | 59.6% | 66.0% | 92.6% | 87.2% |

| % range is current reading as a percentile of Hi/Low range | ||||

| Count % is current reading ranked as a %-tile among all readings | ||||

| GFK survey dates from January 2002 | ||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief