Global| Apr 08 2015

Global| Apr 08 2015Germany Shows Unexpected Weakness and Divergence

Summary

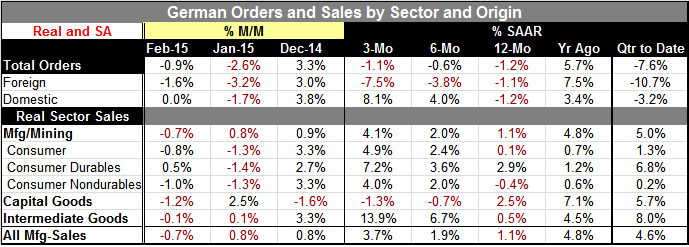

Recent German and EMU data have been on an upswing. This month's German orders report is a divergence from that. Its weak results are unexpected with orders falling for the second month in a row and lower on balance over a broad [...]

Recent German and EMU data have been on an upswing. This month's German orders report is a divergence from that. Its weak results are unexpected with orders falling for the second month in a row and lower on balance over a broad horizon. The report shows internal inconsistencies as well. Obviously this is not the report anyone was waiting for. What is controversial here?

Recent German and EMU data have been on an upswing. This month's German orders report is a divergence from that. Its weak results are unexpected with orders falling for the second month in a row and lower on balance over a broad horizon. The report shows internal inconsistencies as well. Obviously this is not the report anyone was waiting for. What is controversial here?

- German orders fall for two months running.

- Foreign orders show sequential weakness (12-month to 6-month to 3-month) despite falling euro.

- Despite foreign sector weakness, German domestic orders are accelerating sequentially.

- Real sector sales are mixed in February.

- More broadly, real sector sales are sequentially accelerating except for capital goods.

- Capital goods orders are sequentially weakening.

- Intermediate goods orders are sequentially accelerating.

- Overall manufacturing orders are sequentially accelerating.

These patterns are not what we expected to see from Germany with Europe heating up, a new ECB program having impact and the euro exchange rate engaged in a long and deep fall. Germany traditionally is an export-led economy. Its consumer rarely leads the economy ahead. So it is surprising to see domestic economy strength and accelerating momentum in the presence of such foreign order weakness.

Indeed, because of the ongoing drop in the euro, German competitiveness, already in top form, has been even further enhanced. Germany has a huge current account surplus. While much of its trade does occur within the EMU (where currency rates are a non-factor), Germany is the most competitive nation within the group. There is a significant bloc of trade with Russia, but by this time its effect on German order growth should be muted. Weak German export orders are an unexpected development. The weakness makes even less sense if you believe that the euro area is starting to improve as some recent reports have suggested.

Real sector sales echo some of these trends. The ongoing growth and acceleration of sales in consumer durable goods as well as for consumer nondurable goods speaks to the better performance of the domestic economy. Since German exports are concentrated in capital goods, the weakness in capital goods does mesh with the weakness in foreign orders. But this sector also tends to be the backbone of German industry so weakness in this sector with consumer sector output so strong is surprising. In that same vein, the strong acceleration in intermediate goods orders is unexpected. Manufacturing order strength overall suggests that the weakness in capital goods is simply being dominated by other sectors which is unusual.

Of course, these all are conclusions based on emerging trends and sequential growth rate patterns on data of one year and less, and that may be the problem. These may be ephemeral characteristics of volatile trade flows rather than true shifts in strength -even though the trends are quite impressive. Since January 2010, year-over-year percentage gains in consumer sector orders have exceeded capital sector orders only 16% of the time. Generally the consumer sector is stronger when the economy is faced with hard times. For example, from September 2008 through December 2009, capital sector orders fell year-over-year in each month (for 16 months) and consumer sector orders were stronger than capital goods orders in each of those months except one. This `negative signal' is not in place presently despite the surging strength in the consumer sector relative to capital goods. Year-over-year consumer goods orders are up by only 0.1% while capital goods orders still are stronger, rising by 2.5% over 12 months. But this may be another trend to keep an eye on.

European data are hardly clear cut. But there have been some indicators of improvement. As we saw in the Markit PMI data release, the services sector (generally a domestic-oriented sector) is doing the best for most countries in the EMU. The manufacturing sector (the sector more exposed to internationally traded goods) is still lagging despite a considerable legacy of euro-exchange rate weakness. German data are in their own way consistent with these trends (which for EMU transcend the German economy and its impact on aggregate EMU data). This weakness could be the lull before the explosion of growth if the weak euro exchange rate effect has yet to kick in. Or it could be evidence that in this weak global environment exchange rate-derived competiveness advantages don't deliver much growth. Having the lowest prices in a poor neighborhood does not always boost sales all that much. These are things we will be watching for in the months ahead: How much exchange rate stimulus is still lodged in the pipeline? When will the manufacturing sector step up? Can the services sector successfully lead Europe ahead if manufacturing continues to lag? Will Germany's sector orders return to historic patterns or is a new relationship emerging?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.