Global| Oct 15 2013

Global| Oct 15 2013Germany's ZEW Index Advances Strongly

Summary

The two ZEW indices for Germany, one for current activity and the other for expectations, were mixed in October. The current index edged lower to a still strong 29.7 reading, while the expectation index, the most focused on, rose to [...]

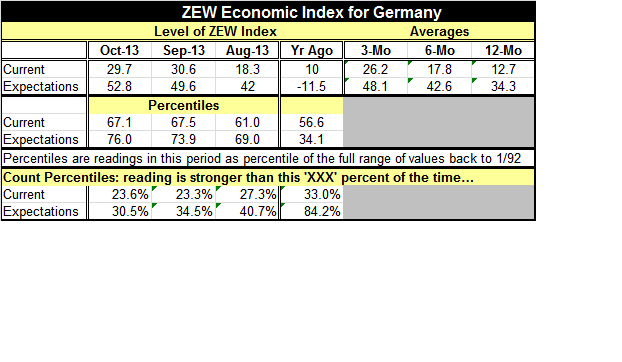

The two ZEW indices for Germany, one for current activity and the other for expectations, were mixed in October. The current index edged lower to a still strong 29.7 reading, while the expectation index, the most focused on, rose to 52.8 from 49.6.

The two ZEW indices for Germany, one for current activity and the other for expectations, were mixed in October. The current index edged lower to a still strong 29.7 reading, while the expectation index, the most focused on, rose to 52.8 from 49.6.

The chart shows the relative strength of both ZEW measures. Expectations are stronger only 30% of the time and the current assessment is better only 23% of the time. These are very solid conditions that are the envy of other EMU members.

However, the optimism found for Germany is not supported for other countries by the other economic statistics of this week. Japan's industrial production in August is now reported to have fallen by 0.9% in the month and is falling at a nearly 3% annual rate over the last three months, but is still up by nearly 1% year-over-year.

In the US, the recently released regional Fed district survey from the New York District, the Empire State Index, fell off sharply, posting a reading of +1.5 in October, down from +6.5 in September. Since the US government is in a partial shutdown, the government's usual economy-wide data are not available and the other piecemeal readings that we do get are more important in nature. The Federal Reserve is still generating its data including five regional surveys, the monthly report on industrial production and other less closely watched regional reports issued by district Federal Reserve banks. However, news reports suggest that legislation is in the works to end the partial shutdown of the US government. We may soon be getting an avalanche of back-data from the US.

The news from Germany continue to improve or show strength. The news for the rest of Europe continues to be mixed. The global data remain on balance on the weak side. Germany is not a harbinger for the EMU area nor is its economy a locomotive. Germany is simply Germany and it is doing better.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief