Global| Aug 15 2018

Global| Aug 15 2018Germany's Retail Sales Rebound- Is It for Real?

Summary

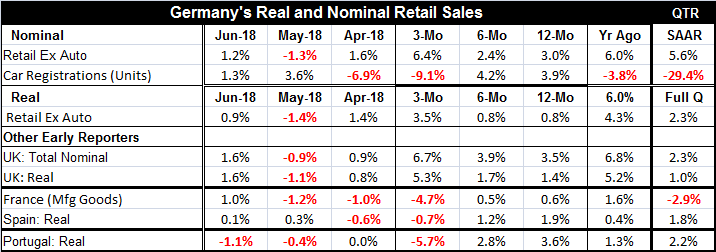

The chart on German real retail sales tells the story of some revival in the three-month trend as the six-month and 12-month trends continue to sag at a pace less than 1% when annualized. Still, there is some near-term revival and [...]

The chart on German real retail sales tells the story of some revival in the three-month trend as the six-month and 12-month trends continue to sag at a pace less than 1% when annualized. Still, there is some near-term revival and that may prove to be the more meaningful tenor but at this point we do not know that but we do know that the short-term growth rate is the most volatile. So the jury remains out on German retail trends.

The chart on German real retail sales tells the story of some revival in the three-month trend as the six-month and 12-month trends continue to sag at a pace less than 1% when annualized. Still, there is some near-term revival and that may prove to be the more meaningful tenor but at this point we do not know that but we do know that the short-term growth rate is the most volatile. So the jury remains out on German retail trends.

The up-to-date real three-month growth rate of 3.5% is solid enough but not impressive for an annualized three-month statistic plus it is the result of real gains in April and June with a drop in May. On top of that, the pace is driven by the gain made in April of 1.4% (m/m) and April drops out of the three-month calculation next month. So on closer look, maybe we should be more skeptical about Germany. Any way you slice it, German retail sales are not impressive and do not look like they are driving anything- at least not at a pace worthy of the autobahn.

There are other European reporters and interestingly the U.K. shows real and nominal sales acceleration despite the issues it faces related to Brexit uncertainty.

Apart from the U.K., France, Spain and Portugal (Italy has not yet reported) show sales are decelerating on a sequential horizon going back 12 months. Three of the four largest EMU economies are reporting data and two of them, France and Spain, show sales decelerating with growth contracting over the most recent three months. That's not reassuring.

The monthly retail sales patterns in the EMU remain choppy. Germany has one decline in the last three months for both real and nominal sales. France and Portugal each have two declines in the last three months while Spain has only one decline and that will be out of its three-month calculation next month. All in all, the EMU members do not show a pattern of gains that is reassuring although it is not yet enough to be concerned about.

Beyond retail sales trends

Europe's growth metrics continue to move to and fro. And even with some recent deceleration in GDP in the EMU, there is nothing disturbing afoot in the data. It is the environment that we are worried about and wondering if there will be contagion enough to undermine the growth that has been in train. The contagion risk (naturally) comes as stimulus has overstayed its welcome and as central banks are actively withdrawing it or making plans for its removal. This has been the risk of removal all along that while stimulus was being taken away, that growth would founder and not be able to survive the transition to less support. And if there are active anti-growth forces in place at that time, so much the worse. Well, not surprisingly, so much the worse it is…

A global market sell-off or crash or dive to recession may yet be in the cards- or not. There is no reason why the global economy should have to transition to hard landing from this position since it is still true that growth has been much more steady and glacier-like than it has been overwrought. The pace of growth has been moderate and balanced and that should give it more staying power. But even car in first gear may not get traction on slippery ice. There are signs of excess. There is too much debt here and there, and interest rates still too low everywhere. Household use of credit is too heavy. Businesses' use of credit is too light at least in the U.S. where even new investment incentives have not spurred a lot of new commitments. Government use of credit is excessive- that goes especially for the U.S. (always) and China where new injections of credit are being used to combat a trade-war related slowing as debt has mounded up very rapidly in recent years.

And, of course, China has chosen to fight the U.S. over its trade demands instead of being more introspective about what it has done, how far it has come on ‘special treatment' and what it can reasonably expect in the future. China has always wanted to play two hands at the global table, one of a large powerful growing industrial economy with growing military might and the other of the poor developing economy needing to pull peasants of the countryside into the modern economy to raise their standard of living and requiring extra ‘considerations.' I think in its own mind, China still can't really come to grips with what it is, and that gets in the way of it finding its place.

Still, China is a big risk factor. Turkey is an active risk factor. Other hot-spots are emerging. Market participants are looking at some markets and at activities that had become routine to them and are beginning to lose their risk appetite… and that is always how it starts. Only time will tell how far it progresses.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief