Global| Jul 27 2018

Global| Jul 27 2018Germany's Inflation Shows Mostly Foreign Inflation Sources

Summary

Inflation rates are on the rise in Germany almost any way you slice them and almost regardless of which metric you use. Almost… All the trends from one year and in by that I mean the usual horizons in the table from 12-month, six- [...]

Inflation rates are on the rise in Germany almost any way you slice them and almost regardless of which metric you use. Almost…

Inflation rates are on the rise in Germany almost any way you slice them and almost regardless of which metric you use. Almost…

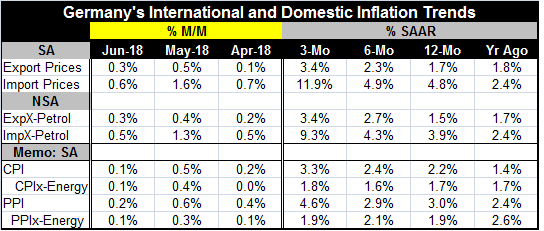

All the trends from one year and in by that I mean the usual horizons in the table from 12-month, six-month and three-month show inflation is trending higher. It is higher on all those progressions except for the ex-energy CPI and headline PPI where inflation sags just a bit from 12-month to six-month before rising again over three months.

Even so...

12-month CPI excluding energy inflation is only a tick higher over three months (1.8%) than it is over 12 months (1.7%). And for the PPI excluding energy, the three-month and 12-month inflation rates lock horns at a 1.9% pace.

There is much more upward push to export and import prices whether seasonally adjusted or not. Despite Germany’s concern about over heating with the lowest unemployment rate on the books since German reunification, Germany’s inflation impulse is coming on in through the trade channel not through the domestic channel. Of course, there is the same policy prescription for both conditions since a higher interest rate would slow the economy and fend off inflation as well as strengthen the exchange rate and put downward pressure on both export and import prices.

Central banks are more prone to look at inflation as a 12-month (yes, at a lagging) growth rate and to set aside the other tenors as simply too volatile (even if more topical) for policy under most circumstances. So we look at the current 12-month inflation rate and compare it to the 12-month inflation rate of 12-months ago. Once done, there is a shocking realization that inflation trends are about as mixed as they are accelerating.

12-month inflation patterns

Both seasonally adjusted and not seasonally adjusted (excluding petrol) export prices are lower on the basis of comparing 12-month inflation to the 12-month pace of 12-months ago. Import prices are higher as headline (total) import prices are accelerating in concert with not-seasonally-adjusted import prices excluding petrol. Both the CPI and the PPI headlines are higher over the last 12-months than the 12-month growth of 12-months ago. But excluding energy, the CPI has the same expansion pace of 1.7% for both periods and the PPI excluding energy drops from a gain of 2.6% 12-months ago to a gain of only 1.9% over the past 12-months.

Core inflation rates in the PPI and CPI reports are remarkably stable. The same result plays out for exports overall and excluding oil leaving only import prices - both (1) headline and (2) excluding petrol- as possessing bad trends or 12 month vs. year-ago inflation.

Of course, the story in Germany is that headline inflation is over 2% -man the lifeboats- and that is the end of that story. If the Bundesbank were making policy, German rates would be higher and would be headed higher as well. But the ECB makes policy for the whole of the euro area and that is a different story. The ECB is looking to end its special securities purchases and to begin to draw rates back up, but it is also marking time and on a very different playing field than the Fed in the U.S. Japan may be on the verge of a policy shift too as BOJ open market operations have taken markets by surprise ahead of the upcoming BOJ meeting.

The EMU area has too many countries for its signals to be clear cut. And aggregate EMU data are swung about largely by conditions in its four largest economies, Germany, France, Italy and Spain. But on that score growth is not in the bag or strong. France reported a same pace 0.2% gain in GDP today (Q/Q) for the second quarter. Meanwhile, French consumer spending in June over May rose by just 0.1%. In Spain retail spending is up by 0.1% year-over-year in June, but that reverses a drop in May. In Ireland, retail sales were announced to have fallen today. The consumer is leading no charge forward in the euro area. However, the overarching Eurocoin indicator for July gained to 0.49 from 0.48 in June and that keeps a positive signal for euro area expansion in play.

Meanwhile, across the pond US GDP expanded by a brisk 4.1% pace Q/Q annualized in Q2. But it did so on some quirks. And inflation expectations for five years ahead in the University of Michigan survey of consumer sentiment actually went down in the face of protectionism and in the wake of a series of Fed rate hikes. The ECB reports today that forecasters are looking for weaker growth and slightly higher inflation there, but they still look for inflation at the 1.7% mark, below the ECB’s target or rate-hiking threshold.

The global economy still looks tight as a drum. Inflation is still largely at bay. Keynesians are either passé or worried like crazy about the inflation to come. But crying ‘wolf’ over inflation persistently doesn’t get you anywhere when a bunny rabbit keeps showing up at your door step. Markets and central bankers seem to have very different views on inflation and on inflation risks. The yield curve, which the Fed Chair seems desperate to ignore, has a very different take on this that apparently hints that it thinks rates can’t continue to ratchet up as they have been if growth is to be maintained. But the Fed is dead set to hike rates ABOVE what it deems to be ‘neutral’. The Fed and the yield curve recession signal (curve inversion – genuflect) are on a collision course. Still, large portions or sectors and myriad relationships in the economy are not behaving as they classically have in the past. Anyone who thinks they know what is really going on is only fooling themselves. Europe’s cautious approach to policy seems appropriate. The Fed’s aggressive ‘set a target and go for it’ approach seems arrogant and reckless in comparison.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief