Global| Sep 25 2017

Global| Sep 25 2017Germany IFO Survey Edges Lower... but Remains Very Strong

Summary

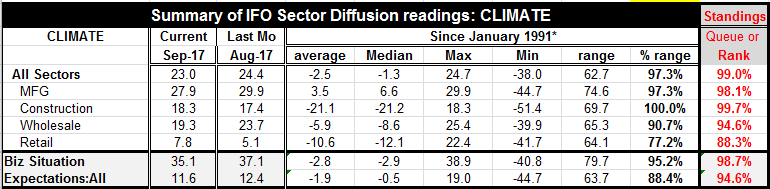

The IFO business situation diffusion index backed off to 35.1 in September from 37.1 in August. Expressed in index terms it fell to 115.2 in September from 115.9 in August. Any way you slice it, the survey shows some weakening in the [...]

The IFO business situation diffusion index backed off to 35.1 in September from 37.1 in August. Expressed in index terms it fell to 115.2 in September from 115.9 in August. Any way you slice it, the survey shows some weakening in the German economy in September. But the index levels are still exceptionally strong and that is the true underlying message here. The German economy remains strong...but despite extremely strong readings it still fails to churn out worrisome inflation pressure.

The IFO business situation diffusion index backed off to 35.1 in September from 37.1 in August. Expressed in index terms it fell to 115.2 in September from 115.9 in August. Any way you slice it, the survey shows some weakening in the German economy in September. But the index levels are still exceptionally strong and that is the true underlying message here. The German economy remains strong...but despite extremely strong readings it still fails to churn out worrisome inflation pressure.

Headlines perform but politics intrude

The headline business situation index has strong 97.7 percentile queue standing while expectations also backtracked to an 11.6 diffusion reading in September from 12.4 in August to hold to a 94.6 percentile standing. These are both extremely high readings. Of course, the German national election results are out now and the IFO survey was conducted ahead of the election. But the election results ran in the direction expected which was to return Angela Merkel's government to a position of primacy in the next coalition. But it does this by showing encroaching division in the German political system as well. Businesses may already be thinking that policymaking in the period ahead is going to be more difficult and more fractious than it has been. Parties unhappy with the expanded introduction of immigrants in Germany saw electoral gains. This fits with a theme seen across Europe that is best represented by the UK giving up its EU membership and being willing to suffer economic hardship in order to gain control of its own borders, something it felt it had lost in its continuing membership in EMU. And despite the EU's apparent harsh treatment of the UK in the exit process, it seems that many of the people in countries that are still EU members share the UK citizen's concerns.

German sector trends

The German sectors show some split conditions across sectors in terms of changes month-to-month. Manufacturing and wholesaling each slipped from August to September with the manufacturing diffusion index dropping two full points month-to-month and wholesaling shedding more than four points in diffusion value. But retailing and construction each saw improvements in August with retailing gaining 2.7 points and construction gaining back nearly one point.

German sector standings

Apart from the monthly changes, all the sectors exhibit a strong showing in terms of their respective standings (or levels) in their historic queue of values. Retailing is the weakest sector with a standing in its 88.3 percentile; wholesaling is next weakest at a strong 94.5 percentile standing. Everything in this report is strong. Manufacturing at its 98.1 percentile is extremely strong and construction is this strong or stronger only 0.3% of the time as it is at its highest value on record.

Strength with a moderate PPI

Despite the good performance of the German economy and the strong across-the-board IFO standings the German PPI to-date through August is up by only 2.4% over 12-months and its 6-month and 3-month rates of expansion each are below a one percent per year pace. The German CPI is up at a 1.8% pace over 12-mo and is accelerating at 2.8% pace over three-months. But EMU wide inflation is stuck more at the 1.5% mark over 12-months and at a 1.6% pace over 3-months with the core rate of expansion at similar growth rates. France and Italy show substantially slower HICP inflation than Germany and EMU, while Spain shows a bit more. Core inflation across the big four EMU members is more mixed but below the EMU target.

Policy hangs in the balance

On balance inflation still is not hot enough to trigger action by the ECB, however, various ECB members (such as Mersch today) talk about it. The ECB will be putting aside some of its special stimulus programs when inflation is more established. The Federal Reserve's decision to begin its balance sheet tapering may also convince the ECB that the time is right for to join in the action. Since the ECB is concerned about the impact of any perceived tightening of policy on the exchange rate (boosting it) taking action in the wake of the Fed's move to get tighter might seem like just the right cover. In its meeting last week the Fed also expressed the collective opinion that there probably would be another rate hike this year and three-more next year. While we have learned that the Fed is not always able to make good on its so-called SEP projections, it has laid out a path to higher rates that has been in place for some time. It should give the ECB ample opportunity to begin its own tapering or tightening in concert. And although inflation in the US, like in EMU, is still not behaving, the Fed is not letting the lack of inflation get in its way of making the policy its members seem to think is the right one despite not touching all the bases it has established for raising rates. Could the ECB get away with that?

The policy environment

It is fair to say that policy is in an unusually difficult environment now. And in Germany the political environment will be a little more mixed and little less unified. Minority parties in Italy seem to gain in popularity as well. In Japan PM Abe has called for snap elections to try to consolidate his hold especially with the new threat of North Korea on his doorstep. In the US Donald Trump continues to be rhetorically aggressive toward North Korea and divisive in his economic and other comments (tweets!) at home. Despite some relatively well-functioning markets we would have to judge the geopolitical background to have become a bit less hospitable. It remains a good time to be vigilant and to keep investment options as fluid as possible. There is no sense of any flight to quality in markets. But then there is no clear and present danger - just nagging danger and "hot-spots". There is a general erosion of international civility and sense of community. In the Middle East the Russians just used war planes to strike at members of a militia in Syria supported by the US. The Kurds finally have laid down their demands for a separate state to be carved out of Iraq. Hot spots seem to abound. So far crude oil and gold are seeing only modest price pressures. But everything is in play.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief