Global| Dec 09 2015

Global| Dec 09 2015German Trade Flows Continue on Sinking Trends

Summary

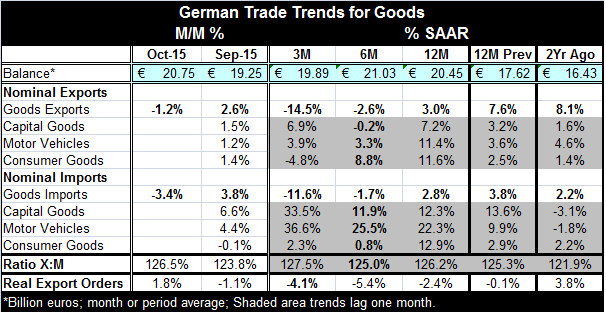

German export and import flows continued to compress in October. Imports in October plunged by 3.4% as exports fell by 1.2%. Exports and imports each are falling over three months and six months; sequential growth rates in the table [...]

German export and import flows continued to compress in October. Imports in October plunged by 3.4% as exports fell by 1.2%. Exports and imports each are falling over three months and six months; sequential growth rates in the table from 12 months through three months show ongoing deceleration. The sharp rebound in trade flows in September has been offset by October's drops and a declining profile is now firmly in place.

German export and import flows continued to compress in October. Imports in October plunged by 3.4% as exports fell by 1.2%. Exports and imports each are falling over three months and six months; sequential growth rates in the table from 12 months through three months show ongoing deceleration. The sharp rebound in trade flows in September has been offset by October's drops and a declining profile is now firmly in place.

The ratio of export values to import values is above its level of one year ago and above its levels of 24 months and 36 months ago. Exports continue to be stronger than imports even when they both are falling.

German real export orders are up in October but also falling on balance over three months, six months and 12 months. While they are not progressively weaker, orders are falling faster over three months and six months than they are over 12 months.

Global growth remains on edge. As we saw in yesterday's OECD LEIs, there are no major countries or country groups that show much strength on the OECD format. Everyone is on that same razor's edge of growth or no growth.

We see record numbers of mergers as companies struggle to find ways to reduce costs and make profits in this weak global environment that some central banks want to construe as `normal.' Much of what these companies do does not turn out to be that successful for the economy at large since cutting employees weakens the economic fabric even if it lowers a company's costs. Between international competition and technology, labor has been under a great deal of pressure.

Some laud the drop in the unemployment rate in the EMU and in the U.S. But for the EMU, much of the drop is Germany alone. Falling labor force participation rates generally dress up unemployment statistics. This is a major factor in the U.S. If you calculate unemployment in the U.S. and hold the participation rate steady at its pre-recession level, the current U.S. unemployment rate (yes, the U3 rate) comes in around 10%. I do not argue that this is the right way to calculate it; I just mean to focus on how important the participation rate is to our understanding of what unemployment really is. If central banks focus on the labor market, are they getting the right signal?

German exports and imports both are weak. While the German economy is doing relatively well (including having its lowest unemployment rate since the EMU was formed), domestic demand is still not pulling in much in the way of imports. Three-month import growth was last weaker in January 2012. German trade data echo old concerns about global growth with export weakness and raise new concerns about German domestic demand on import weakness.

France has reworked its GDP outlook to account for the damage caused by the Paris terror attack. We do not know about knock on effects or even if the French authorities have their estimates right. But there is plenty of reason to look at each growth disappointment coming out of Europe and wondering if it is real or if it will magnify. Germany's export weakness is one such development; but import weakness is another. We can hope that this is just trade volatility. But both German exports and imports sketch out a path of weakness that is compelling in its message. Now we must watch to see how the situation develops. There is not a lot of reason for optimism. Every firm and country has been doing its best to squeezes blood out of a stone. At some point all the efficiencies and growth have been squeezed out the system and a new fundamental push is required. Where will it come from?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief