Global| Jun 09 2021

Global| Jun 09 2021German Surplus Ticks Higher As Exports and Imports Revive

Summary

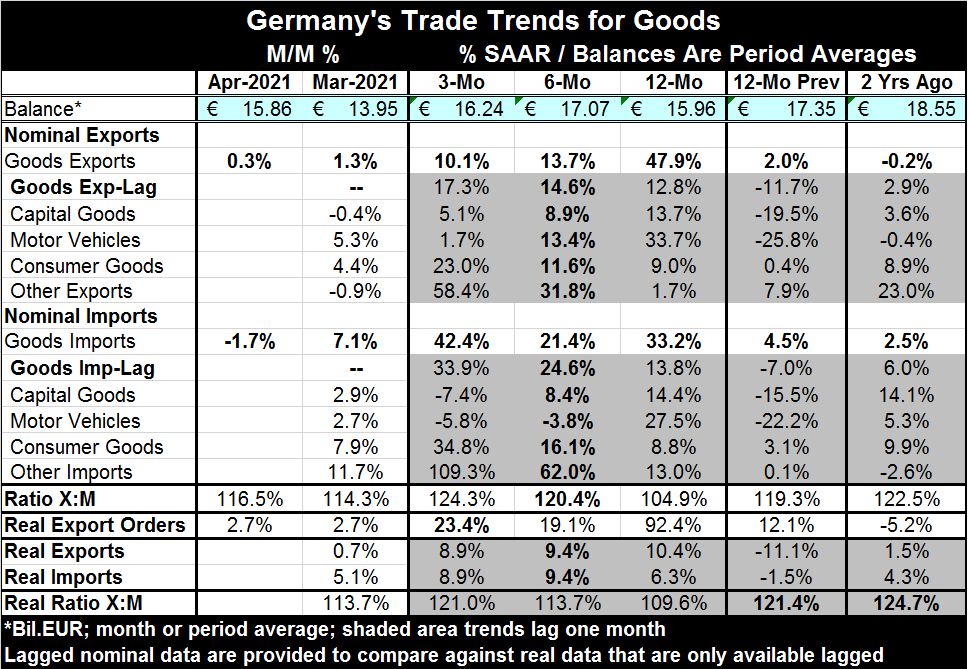

German exports disappointed, ticking higher by just 0.3% in April after a 1.3% gain in March. Still, German imports fell by 1.7% after a 7.1% rise in March and those results pushed the German surplus to €15.8bln in April up from [...]

German exports disappointed, ticking higher by just 0.3% in April after a 1.3% gain in March. Still, German imports fell by 1.7% after a 7.1% rise in March and those results pushed the German surplus to €15.8bln in April up from €13.9bln in March.

The sequential growth rates show exports slowing. But the 12-month growth rates are being artificially boosted over 12 months because of a weak base of results generated by the start of the Covid-19 crisis one year ago. Still, the 12-month growth rate of 47.9% gives way to a sharply lower 13.7% pace over six months and to 10.1% over three months (47>13>10); this is classic deceleration.

Imports manage to fight off trend deterioration as their year-on-year growth logs a 33.2% gain which withers to a 21.4% pace over six months then snaps back to a 42.4% gain over three months. This sequence has no clear trend.

And these results are very sensitive to the choice of a base. If we look at the components for German trade as well as the lagged exports headline and lagged imports headline, we see that pushing back the calculations for sequential growth by one month leaves both exports and imports in a state of acceleration (17>14>12) for exports; for imports (33>24>13)- these refer to the sequential growth rates on the lagged totals for exports and imports. Having the trend results reversed so easily makes the calculation of trends less useful.

Because of the year ago Covid mess, there is no sense that these trends will last. However, putting the 12-month gains aside, German imports have revived faster than German exports. But that too is a function of the Covid and the reinfection cycle more than the original Covid hit. In short, we really have no good way to vet the current trends in trade; everything is flawed.

The Baltic dry goods index, an index of global shipping volumes, has recovered strongly from its May 2020 low but has recently begun to retreat from its May 2021 peak. The degree of backtracking is significant, but the thrust of the uptrend still seems to be in place.

The Baltic dry goods index, an index of global shipping volumes, has recovered strongly from its May 2020 low but has recently begun to retreat from its May 2021 peak. The degree of backtracking is significant, but the thrust of the uptrend still seems to be in place.

However, because all of these series on imports exports trade volume by country or region or globally all share the same vulnerability to the impact of past Covid shutdowns on the flows being measured and therefore rendering that flow’s trend less useful for projection into the future. As you know, any two points generate a straight line and so moving the point of origin will shift the trend just as will moving the endpoint. That means that the trend is affected by not just current performance but by where we measure the trend for the start and that in turn will be affected by the virus situation at the time. Look at the difference between running a trend on the Baltic dry goods index from the May 2020 low to the May 2021 high versus running one from the July 2020 peak to the May 2021 low. Both will slope up, but one would be very steep and the other would be much flatter.

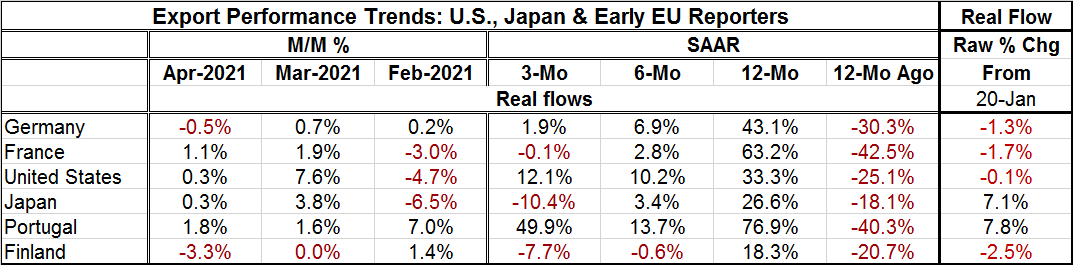

It is useful to vet the German trends with reference to other global and European trends. Here we focus on exports. In doing this we mix together more virus-impacted data but where the cycles of infection were different. In doing this, we see a lot of commonality. Sequential exports are decelerating from 12-months to six-month to three-months everywhere except for the U.S. and Portugal; the U.S. is a very minor exception to the trend. The real flows on data back to the pre-Covid base of January 2020 show net export contraction everywhere except Japan and Portugal.

These trends together; the German data- current and lagged, the cross-country exports data and the Baltic dry goods chart, are testaments to this still being a period in which demand, output, growth and trade are working out the kinks from Covid. There have been some eye-popping GDP growth numbers to be sure. But they follow from what have been eye-popping setbacks as well.

Navigating uncharted waters

As we navigate through this period of unexpected data shifts, we are looking for the deep water between the rocks. We are trying to find where the trend will have smooth sailing, on which gradient? Yet, the virus is still in play and some are trying to conjure up a picture of extreme risk from a growing presence of a more virulent form of the virus. Are they right? Or are they people with an ‘agenda?’ Rochelle Walensky, head of the CDC in the U.S., issued a blistering warning over two months ago citing her feeling of ‘impending doom’ (here, on March 29). Instead, the states opening up did not fuel higher infection rates. Instead, infections have continued to fall to extremely low levels. Instead, there has only been unfolding joy and no impending doom at all. But Anthony Fauci in the U.S. appears to be trying to conjure that boogeyman again as pieces have been aired that reveal his past errors and perhaps his own lack of objectivity is dealing with the Covid crises especially as regards its origins. His response is to double-down on fear.

We are in a place where it is hard to know who or what to trust. Partisans are turning to their own figure heads for guidance even as their past actions appear to have been flawed. The stymying of open discussion over Covid under the rubric of ‘fake news’ will forever live as a low point in American free speech and a reminder that it is not just the government that can squelch free speech especially not in an information age where the portals of information exchange are controlled by corporations with an agenda of their own. Not having the truth or the right facts make it had to arrive at an educated conclusion. Halting discussion over scientific issues when science itself is not really established is a horrific mistake. And it’s a mistake we made…

These mistakes have feedback effects. And these effects are baked into the economic data that we are now trying to use to make good decisions about our future from data that are flawed. What we need is good clear analysis of the issues and not politicized spin by this one who hates that one. Science is not about personalities. But scientists have personalities and there are spheres of influence and thought in any scientific field. There are the top dogs and renegades-and sometimes it is the renegades who are right. Having information has never been more important and we have far too little of it despite being smack dab in the middle of a period where people talk of information overload and engage in ‘Big Data’ research. We need to get our politics out of our science, for once and for all. It does not help when a prime public figure attempts to cast attacks against him as an attack on science. They aren’t. If the glove fits, wear it. If a scientist has been wrong, he or she should admit it. Even scientists need to belly up to the bar and admit when they were wrong. But their desire for walk-on-water credibility prevents it. Too bad, we expect mealy mouthed denial from our politicians since that is their stock in trade, not from our scientists.

Commentaries are the opinions of the author and do not reflect the views of Haver Analytics.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief