Global| Dec 08 2017

Global| Dec 08 2017German Surplus Steps Back As Exports Fall for the Second Month in a Row

Summary

German exports and imports are both off their recent peak year-on-year rates of growth. Exports have fallen for two months in a row. Imports are up in October and by more than their drop in September. There is no sequential [...]

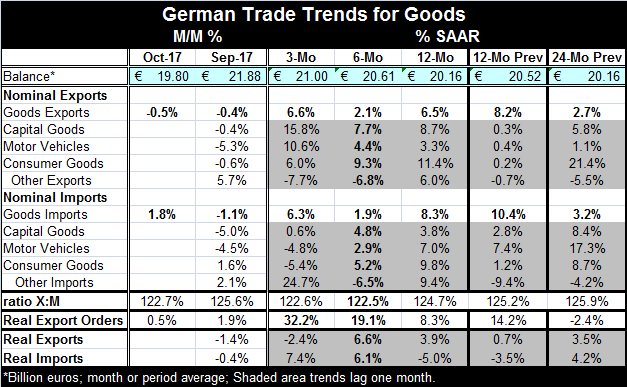

German exports and imports are both off their recent peak year-on-year rates of growth. Exports have fallen for two months in a row. Imports are up in October and by more than their drop in September. There is no sequential acceleration or deceleration for exports or imports. Both series show a relatively sizeable year-on-year gain followed by a slower, near 2% growth rate over six months and that is followed by a three-month pick up in the 6% growth rate range. That bit of oscillation leaves exports with about the same three-month pace for growth as over 12 months and finds imports with a weaker pace over three months than over 12 months.

German exports and imports are both off their recent peak year-on-year rates of growth. Exports have fallen for two months in a row. Imports are up in October and by more than their drop in September. There is no sequential acceleration or deceleration for exports or imports. Both series show a relatively sizeable year-on-year gain followed by a slower, near 2% growth rate over six months and that is followed by a three-month pick up in the 6% growth rate range. That bit of oscillation leaves exports with about the same three-month pace for growth as over 12 months and finds imports with a weaker pace over three months than over 12 months.

Recent German industrial reports have been somewhat disappointing. While German industrial real orders were strong, that report paired with news on real shipments that showed a decelerating to flat performance with particular weakness for capital goods. German industrial production also disappointed and showed a 1.4% drop in October, its second drop in a row. German IP also showed sequential growth rates of its three main sectors decelerating from 12-month to six-month to three-month.

Today's trade report shows a two-month drop in exports that is only a bit worrisome. While nominal German exports are growing at a 6.6% pace over three months, real exports are falling at a 2.4% annual rate. That is weaker than their 3.9% gain over 12 months. But there is a stronger growth rate for German exports over six months, so there is no sequential deterioration, just some volatility. Exports on capital goods are doing quite well with an accelerating three-month growth rate (on one month lagging data as always for trade sector results). On the other hand, German real imports do show sequential acceleration with a 5% decline over 12 months that shifts to a growth rate of 6.1% over six months and one of 7.4% over three months.

In the Markit PMI framework, German manufacturing is still strong, showing a gain to a diffusion reading of 62.5 in November after a cooling off in October. The German manufacturing sector has its highest PMI reading since at least January 2012. However, on services side, things are different with a PMI ranking only in its 56th percentile, much closer to its median on this timeline.

Still, German real imports are gaining pace, rising at a 7.4% rate over three months despite logging a 5% decline over 12 months. The softness in the German services sector does not seem to be a sign of weakening German domestic demand.

On balance, the German economy seems to be going through a bit of a rough path. But there is less weakness than there is irregularity. Real orders, which have been a reliable future indicator, are still quite strong. Some unevenness in shipments of goods by sector and in international trade is to be expected. The November German manufacturing PMI reading is reassuring that whatever hiccup was experienced in October it is over in November. The German trade surplus, while lower on the month, is still massive.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief