Global| Sep 02 2020

Global| Sep 02 2020German Retail Sales Unexpectedly Slip

Summary

Germany's retail sales slipped in July falling by 0.3% despite substantial government efforts to support growth and consumer spending. Some had the hoped that with stimulus Germany might become a bit of a locomotive for European [...]

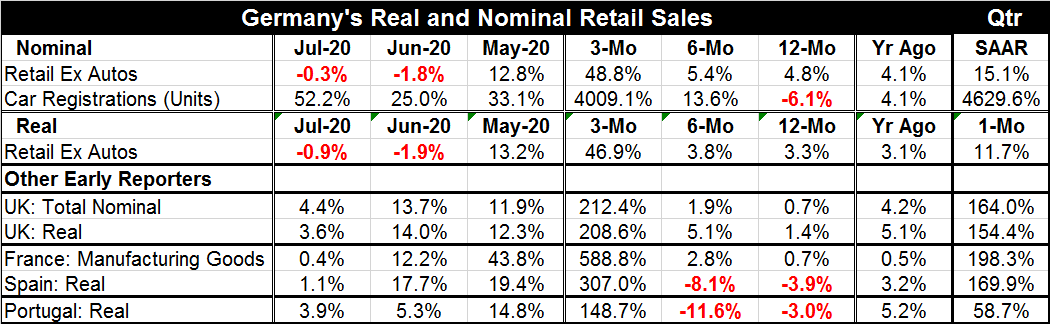

Germany's retail sales slipped in July falling by 0.3% despite substantial government efforts to support growth and consumer spending. Some had the hoped that with stimulus Germany might become a bit of a locomotive for European growth as Germany backed away from its program of running fiscal surpluses to meet the challenge of the coronavirus. But consumers are not cooperating as retail sales have fallen for the second month in a row. Real retail sales are lower for the second month in a row as well.

Germany's retail sales slipped in July falling by 0.3% despite substantial government efforts to support growth and consumer spending. Some had the hoped that with stimulus Germany might become a bit of a locomotive for European growth as Germany backed away from its program of running fiscal surpluses to meet the challenge of the coronavirus. But consumers are not cooperating as retail sales have fallen for the second month in a row. Real retail sales are lower for the second month in a row as well.

However, car registrations are responding as they gained by 52.2% in July after a 25% rise in June. Sequentially from 12-months to six-months to three-months, German annualized retail growth rates excluding autos rise from 4.8% to 5.4% to 48.8%. There is a similar escalation with similar magnitudes in play for real retail sales (excluding autos as well). The figures for autos are off the charts- literally. German vehicle registrations still fall by 6.1% year-over-year. Over six months, they rise at a 13.6% annual rate. But over three months, the pace is a massive 4,009.1% annual rate and that is where spending has been focused. But it is also true that German vehicle registrations had fallen off very sharply previously and that is why sales are still net lower over 12 months despite a moon-shot-like growth rate over three months.

There had been a downturn in German passenger car sales in 2018 in the wake of the emissions scandals in Germany. While sales did rebound from that and make some nice net gains, they did not fully make up for lost ground. Then the pandemic hit and retail sales and vehicle registrations all imploded together. Despite recent weakness, retail sales are growing again year-on-year. And despite a massive surge, vehicle registrations are still below their year ago levels.

German stimulus as a bulwark

On balance, the German stimulus is sort of holding things together, but consumer spending is no bright spot for the German economy or for the EMU. In March, Angel Merkel's government launched stimulus measures, financed with record borrowing of €217.8 billion, to help companies and consumers get out of the coronavirus crisis. The stimulus package included a temporary cut in the value-added tax, set to run from July 1 through December 31. The VAT tax cut is worth up to 20 billion euros and gauged to give domestic demand an added thrust ahead. But these recent German retail sales figures cast some doubt on whether the measures are really working. However, this is only the first month of the VAT cut. There seems to be a substantial impact on vehicle sales but not so much for the rest of retailing which is nonetheless coming off a very strong gain in May- but with no follow-through. Apparently, some companies are not passing on the VAT tax cut to consumers. Shoppers generally have been spending modestly in the wake of their splurge in May.

Retailing around EMU and Europe

If we look at other early retail sales reporters in the EMU, we see very similar patterns. The U.K., France, Spain and Portugal all reported surging sales in May. But unlike Germany, most of them also recorded double-digit gains again in June. Sales slowed but continued to make gain in July in these countries while Germany experienced sales reductions in June and July. Germany does not appear to be leading anything on the retail front. Its 12-month sales are the best in Europe among this group of countries, but then there is the momentum lost on more recent sales. A look at the sequential growth rates confirms that Germany's near 50% sales gain (annualized) over three months is dwarfed by triple-digit compounded gains over three months for the U.K., France, Spain and Portugal. Similarly, in the quarter-to-date, these other European countries are experiencing faster growth than Germany. Germany has a solid 15.1% gain in sales compared, again, to triple digits for the U.K., France and Spain with Portugal's sales up at a 58.7% pace.

Summing up

Europe is reviving. And despite taking steps to stimulus, Germany is lagging the other countries (that also have taken stimulus steps) and it is failing to build on past success. This is the most feared scenario when a country has a rapid start to recovery then something cuts it short, it stumbles, and momentum is lost. Germany seems to be sleep-walking through such a series of events. Fortunately, the rest of Europe is not. But unfortunately, the virus is not contained and there has been a new set of issues for Spain recently. Germany and the U.K. have seen reinfections rise and slow their economies as well. Europe is still dealing with the reality of the virus and its consequences. While the U.S. is in the middle of its silly season on the run up to November elections, all that you read here about is how Trump made mistakes in dealing with the virus. But this is political hash. Europe shows us clearly that virus goes around and comes around and that it is very hard to contain. Nations that once were applauded for their handling of the crises have found themselves back in a thick viral soup again. Countries that were criticized (like Sweden) are now in favor. The only revelation in Europe is that, after its rough start, Sweden is getting good grades for its economic performance and by letting the virus spread it is gaining on herd immunity. Everyone else has all their eggs in the vaccine basket. One of them better work, and work well, or 2021 will repeat much of what we all have been through in 2020 – except for Sweden.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief