Global| Oct 31 2016

Global| Oct 31 2016German Retail Sales Drop Is Largest in Two Years; Meanwhile HICP Pressures Edge Up As EMU-Area Growth Steadies

Summary

German retail sales (excluding autos) fell off sharply in September as the largest drop in two years was logged. This came on the same day when EMU-area GDP growth was reported to have steadied on the quarter and amid a rise in [...]

German retail sales (excluding autos) fell off sharply in September as the largest drop in two years was logged. This came on the same day when EMU-area GDP growth was reported to have steadied on the quarter and amid a rise in inflation that showed the EMU HICP continues to run below its policy path.

German retail sales (excluding autos) fell off sharply in September as the largest drop in two years was logged. This came on the same day when EMU-area GDP growth was reported to have steadied on the quarter and amid a rise in inflation that showed the EMU HICP continues to run below its policy path.

German retail sales month-to-month

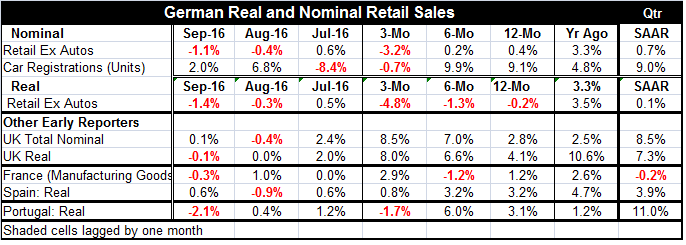

The year-on-year gain in nominal German retail sales is at 0.4% while real sales ex-autos show a drop of 0.2% over 12 months. Both real and nominal sales show sequential growth rates that are getting progressively weaker on shorter horizons. The German retail sales pattern is not encouraging. Last week, GfK in its look-ahead consumer confidence rating for October projected a drop in German confidence in September. Nominal and real German retail sales figures have both slowed sharply from posting gains of about 3.5% over 12 months over the year earlier period.

German car registrations

However, car registrations in Germany have been holding up. They expanded by 2% in September (month-on-month) and are up by 9.1% over 12 months. Registrations, however, are still contracting on balance over three months.

Quarter-to-date performance

In the quarter-to-date (just completed Q3), German real retail sales are up by the thinnest of margins at 0.1%. Vehicle registrations are still strong as they are up at a 9% annual rate.

Retail sales in Europe

Other early European retail sales reporters include the U.K., France, Spain and Portugal. Sales are weak or lower in September of each of these countries except Spain where real sales rose by 0.6% in September (but after a 0.9% drop in August). Still, the sequential growth rates of real retail sales in these countries generally shows growth and firming with the exception of Spain and Portugal. In Spain sales slowed on balance over three months while in Portugal sales dropped over three months. Still, sales are growing year-over-year in each of these countries with the slowest annual growth in France at just 1.2% over 12 months.

In the quarter-to-date, sales are generally strong as well. In the U.K. sales are up at a 7.3% pace in Q3 compared to an 11% pace for Portugal and a 3.9% pace for Spain. Sales in France, however, are the exception; they are falling in Q3 at a -0.2% annualized rate.

European GDP

Other early releases to today that are out on a preliminary basis and without a lot of background details include European GDP. It showed a 1.4% Q3 annualized gain in the EMU, a slight uptick in the quarter-to-quarter pace (up from 1.2%, previously). The U.K., reporting earlier last week, logged a 2.3% rise, a solid number but a slight deceleration from its 2.7% pace in Q2. Spanish GDP gained at a 2.8% pace, a bit slower than its 3.4% rise in Q2. Belgian GDP rose at a 0.8% annualized pace in Q3, slowing from its 2% pace in Q2.

Year-on-year rates of growth saw the EMU's Q3 gain at 1.6%, the same as in Q2. France, the second largest economy in the EMU, posted a four-quarter rise of 1.1%, a bit slower than the 1.3% gain in Q2. GDP also slowed in Spain with the euro area's fourth largest economy seeing GDP rise by 3.2% over four quarters compared to 3.4% in Q2. The U.K. and Belgium each accelerated over four quarters while the U.K. pace at 2.3% bettered its Q2 gain of 2% and Belgium's gaining 1.3% just beat its second quarter's four-quarter rise of 1.2%.

European inflation

The early read on euro area inflations saw a gain of 0.2% month-to-month after flat performance in October and in August. That took the year-on-year gain up to 0.5%, still well below the ECB target of just under 2%. Core inflation rose by 0.1% month-to-month after being flat for two months. Its 12-month gain is 0.7%. Inflation trends show German and Spanish inflation at or above a 2% pace over three months and six months. France and Italy continue with gains in the 0.3% to 0.4% pace (annualized) over three months and both are under a 1.5% pace over six months. Over 12 months German inflation is up by 0.7% and French and Spanish inflation gains are at 0.5%. In Italy prices are falling by 0.1% over 12 months.

Other market-related news: OPEC to the new U.S. FBI investigation

In addition to these trends, we have important inflation-related news from OPEC this weekend telling us that it could not cobble together a deal with non-OPEC members to restrict output with the goal of underpinning prices. On that news, oil prices are weakening again. Rising energy prices have been one of the main forces behind firming prices in recent months. Separately, U.S. news from Friday that the FBI has reopened the investigation into presidential candidate Hillary Clinton's emails from when she was Secretary of State and used a private email server. New information pertaining to her has come to light from the pursuit on another investigation unrelated to her. News of the investigation's re-opening is affecting equity and foreign exchange markets and has created a stir in the U.S. This news is now something to watch as much as economic data. It is affecting markets as well as election polls.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief