Global| Apr 01 2010

Global| Apr 01 2010German Retail Sales Back-Track In February But Still Show An Uptrend Can It Last?

Summary

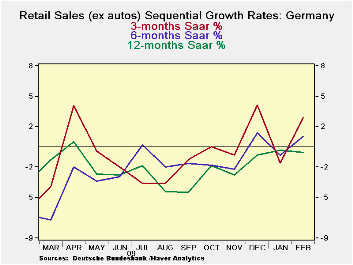

In terms of its broad trends German retail sales are beginning to do a bit better. The three-month rate of growth is better than the six-month rate of growth which exceeds the twelve month rate of growth. So the sequential growth [...]

In terms of its broad trends German retail sales are beginning to do a bit better. The three-month rate of growth is better than the six-month rate of growth which exceeds the twelve month rate of growth. So the sequential growth rates for German nominal sales are turning higher.

Still January and February are not very strong months for German consumers. Retail sales ex autos were flat in February and off by 0.4% in January. Inflation-adjusted sales are off for two months running. The sequential growth rates for Real ex-auto retail sales are not as bright as for nominal sales either. Still they are not bad registering acceleration for 12-months to six months and growth over three months even if a bit slower than it was over six months. But at this rate we’ll have to see if the trend holds up.

In the quarter-to-date German retail sales are falling for all but two categories. Food beverage and tobacco sales are up in the quarter-to-date and car registrations are flat. Still nominal retail sales are falling at 0.2% annual rate and real ex auto retail sales are falling at a 1.6% pace.

As Europe’s biggest economy Germans are doing very little to provide the domestic demand to boost the euro-zone into recovery. Instead Germany’s tactic is to sit back and let its export growth benefit from increases in domestic demand elsewhere and let that pull Germany into an export-led recovery. It’s not a very leading role for Europe’s largest economy and it goes a long way to explain why Europe simply lacks economic dynamism.

| German Real and Nominal Retail Sales | ||||||||

|---|---|---|---|---|---|---|---|---|

| Nominal | Feb-10 | Jan-10 | Dec-09 | 3-MO | 6-MO | 12-MO | YrAgo | QTR Saar |

| Retaill Ex auto | 0.0% | -0.4% | 1.1% | 2.9% | 1.0% | -0.5% | -3.5% | -0.2% |

| MV and Parts | -0.4% | -0.5% | 1.0% | 0.4% | 0.8% | -0.9% | -3.3% | -1.6% |

| Food Bev & Tobacco | -2.3% | 0.0% | 2.2% | -0.4% | -7.1% | 0.0% | -2.5% | 1.1% |

| Clothing footwear | 1.6% | -3.1% | 5.3% | 15.1% | 10.3% | -1.2% | -4.5% | -11.4% |

| car registrations (units) | 1.8% | 2.7% | -16.7% | -42.6% | -43.3% | -29.9% | 28.5% | 0.0% |

| Real | ||||||||

| Retail Ex auto | -0.4% | -0.5% | 1.0% | 0.4% | 0.8% | -0.9% | -3.3% | -1.6% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief