Global| Apr 20 2015

Global| Apr 20 2015German PPI Still Under Downward Pressure But Abating?

Summary

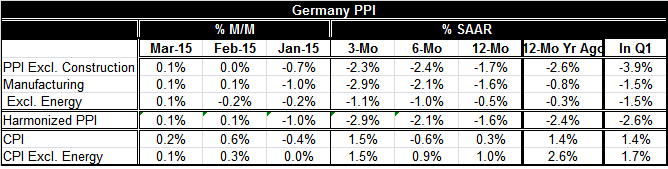

Germany's PPI rose by 0.1% in March, still dropping by 1.7% year-over-year. The chart shows that the year-over-year drop is slightly less than it was a month ago and that the downward progression in the PPI trend may be abating. This [...]

Germany's PPI rose by 0.1% in March, still dropping by 1.7% year-over-year. The chart shows that the year-over-year drop is slightly less than it was a month ago and that the downward progression in the PPI trend may be abating. This tendency is present in the three major rates of change plotted in the chart.

Germany's PPI rose by 0.1% in March, still dropping by 1.7% year-over-year. The chart shows that the year-over-year drop is slightly less than it was a month ago and that the downward progression in the PPI trend may be abating. This tendency is present in the three major rates of change plotted in the chart.

The declining PPI is largely an artifact of weak oil prices. Oil prices on world markets slipped again today as the Saudis announced plans to keep their oil output at a relatively high level. Meanwhile, in China a special cut in reserve requirements has been made to try to support growth after China's weak Q1 GDP reported last week. Global demand is not underpinning oil prices and, while the downtrend in the German PPI seems to be abating, the truth is that the future path of the PPI and of world oil prices remains too elusive to pin down.

Today in an outlook by the Bundesbank, that institution noted that demand in Germany would be underpinned by the consumer, an unusual driver of German growth. The Bundesbank is expecting first quarter growth to come in below fourth quarter growth.

The euro has been plunging on world markets for some time. The nominal euro is lower by some 21% over the past 12 months. In real terms, the broad euro exchange rate is lower by 15% over the same period. That has been good enough to send Spanish exports to an all-time high. Yet, Germany, the most competitive country in the euro area, is not seeing its industrial sector faring so well. Many German exports are oriented toward Russia where sanctions bite, and to China, where growth has recently been stunted.

In their recent meeting as a part of the IMF-World Bank meetings, world finance ministers have noted the continuing risk to the global recovery. Despite ongoing and extreme monetary stimulus - some just re-upped in Europe on a new QE program- and more just launched in China today with a fresh cut in bank reserve requirements, the global economy will not shift out of first gear, a gear in which it continues to flounder and sputter. In this environment, price weakness continues in both CPI and PPI prices.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.