Global| Apr 18 2008

Global| Apr 18 2008German PPI Spurts in March

Summary

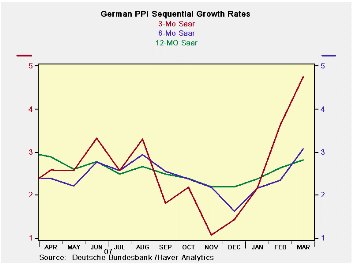

Germany’s manufacturing PPI surged by 0.5% in March elevating the 12-month inflation rate to 4.2% and keeping inflation accelerating from 12 months to three months, as the three-month rate climbed to 6.4% (saar). Ex-energy the [...]

Germany’s manufacturing PPI surged by 0.5% in March elevating the 12-month inflation rate to 4.2% and keeping inflation accelerating from 12 months to three months, as the three-month rate climbed to 6.4% (saar). Ex-energy the inflation acceleration is even clearer: from 2.8% over twelve months, to 3.1% over six months, to 4.7% over three months. In Q1 2008 the PPI is also too high for comfort. The manufacturing PPI is up at a 6.2% annual rate compared to a 3.5% annual rate for manufacturing excluding energy.

This result is, of course, for one of the low-inflation EMU nations. The non-energy PPI has risen by 0.4% in each of the past three months in Germany. We know that the ECB has just reset forecasts to account for a longer period during which inflation will supersede its ceiling of 2% (HICP inflation, not PPI inflation). The pressure at the producer level in Germany mirrors a similar situation in the US. Producer level prices are soaring but consumer level prices have been better behaved even when we compare apples-to-apples (core goods PPI to core goods CPI). Are these pressures that are building up at the producer level going to spring forth in the coming quarters in the CPI (HICP)? Or, has productivity kept the pressures off the CPI and will these PPI pressures remain largely at bay? The ECB is worried about second round effects and is monitoring wage agreement as well as firms hiking prices to recoup past energy/food price gains. For the moment the results are unclear but the expected date for inflation’s return to below its ceiling is being pushed out and the ECB is remaining vigilant. The ECB expresses concerns about inflation as well as about slowing growth but has set policies only to keep inflation at bay. In the US the policy tact is the opposite. Since Germany gives us some of the better inflation trends in EMU, it’s no wonder that the ECB is so worried.

| Germany PPI | ||||||||

|---|---|---|---|---|---|---|---|---|

| %m/m | %-SAAR | |||||||

| Mar-08 | Feb-08 | Jan-08 | 3-mo | 6-mo | 12-mo | 12-moY-Ago | IN Q1 | |

| MFG | 0.5% | 0.6% | 0.5% | 6.4% | 6.5% | 4.2% | 2.5% | 6.2% |

| Ex Energy | 0.4% | 0.4% | 0.4% | 4.7% | 3.1% | 2.8% | 3.0% | 3.5% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief