Global| Jan 19 2018

Global| Jan 19 2018German PPI Slows Its Year-on-Year Gain in the Face of Oil Price Strength

Summary

German inflation trends have flattened out despite what has been a period of rapid increases in the oil price. Ex-energy inflation is flat and very mild while the headline PPI shows some of the impact of sharply rising oil prices (see [...]

German inflation trends have flattened out despite what has been a period of rapid increases in the oil price. Ex-energy inflation is flat and very mild while the headline PPI shows some of the impact of sharply rising oil prices (see Chart on right for a tracking of Brent oil vs. the German PPI).

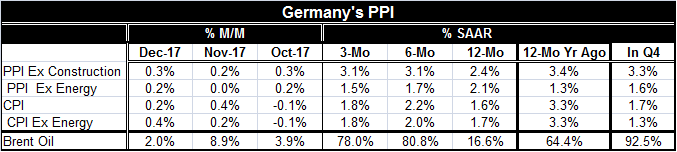

Inflation trends are now mixed and contrary. The headline PPI has accelerated from 2.4% over 12 months to a pace of 3.1% over three months and six months. The PPI excluding energy, meanwhile, is in full deceleration mode with inflation dropping from 2.1% over 12 months to 1.7% over six months to 1.5% over three months. The CPI and CPI excluding energy both are trendless with inflation in a 1.6% to 2.2% habitat for the headline and the core for horizons spanning 12 months and three months. Each of these price series shows a hint of acceleration because, for each, the three-month pace is above the 12-month pace.

In the quarter-to-date, the divisions are stark. The PPI headline is up at a 3.3% pace with the ex-energy reading at 1.6%. The CPI has a 1.7% pace with the ex-energy reading at 1.3%. In both cases, inflation measures excluding energy are significantly lower. But this is about history: what should we expect ahead?

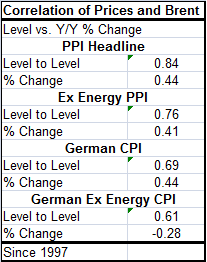

The correlation table below shows some interesting and curious results. Looking at the headline PPI, ex-energy PPI, CPI and ex-energy CPI, in all cases the headline has the higher correlation with Brent either in price level terms or looking at year-on-year changes. Price levels correlate higher to Brent than do year-on-year price changes. That might indicate some slipperiness or inconsistency in the pace of the inflation pass-through speeds from oil to consumer or producer prices. A lot of it is simply the impact of a correlation bias because prices grow over time while inflation doesn't (hopefully). The ex-energy PPI and headline CPI have almost the same correlation to Brent. But what is odd and most interesting is the negative correlation of the ex-energy German CPI to Brent even though the price levels correlate well.

The reason for this unexpected peculiarity is that so many oil prices spikes correlate with German economic downturns. And when the German economy turns lower, the CPI is damped and it slows creating a negative correlation to rising oil prices. The impact of the German downturn on the German ex-energy price level comes first and hits much harder than it hits Brent.

As the top table shows, oil prices are rising again. The pace of the rise in Brent is nearly at 80% over three months and six months compounded and annualized. In Q4, the pace on that basis is over 90%. OPEC and friends have finally been able to control output, but the IEA nonetheless estimates that this year oil production in the U.S. will outstrip production in Saudi Arabia. The U.S. fracking industry is still going strong and will be adding to supply. It is a question as to whether global growth is going to come on-stream fast enough to exert demand side pressure on energy prices. The supply balance is going to be fed by U.S. fracking. So while there has been some recovery in oil pricing, I think we need to remain somewhat suspicious of the extent of oil's rise and of its sustainability at these levels. I know I don't need to remind you of oil's tendency to overshoot. Oil does not go from low to high and stay there. It does go from way too low to way too high and then pulls back to find a lower trading range. This is the price discovery process oil currently is playing out in markets. And remember it is using artificial output restriction to achieve its objective. Once oil marks a trading range and the Saudis and Russians go back to their desired output levels, there is no guarantee that this range (whatever it turns out to be) will hold. The two key players in this output restriction game, the Saudis and Russians, really need their oil revenues. They may be able to sustain production caps for a period of time but not indefinitely- that is especially true for Russia. Both Russia and the Saudis are one-trick ponies when it comes to where their revenues come from. It's oil hands down. And that should make us wary of the staying power of output restrictions and of the potential for oil prices to remain 'high.'

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief