Global| Jun 20 2018

Global| Jun 20 2018German PPI Sees Pressure, But Core Rate Is Much Less Affected

Summary

Germany has a history of being ‘unreasonable’ about inflation. In the interwar period with the development of hyper-inflation, Germans developed a strong aversion to even a whiff of inflation. So Germany, nationally and down to [...]

Germany has a history of being ‘unreasonable’ about inflation. In the interwar period with the development of hyper-inflation, Germans developed a strong aversion to even a whiff of inflation. So Germany, nationally and down to populist roots, has less tolerance for inflation than just about any other European nation. While many central banks are willing to shift their focus to core prices when odd oil or food price events ‘distort’ headline inflation, Germany is less likely to do that. Of course, the just-released index at hand in May is the PPI and the PPI is not the price index that used to be targeted by the Bundesbank and it is not the one targeted by the ECB today. In fact, it’s important to remember that ECB targets the headline HICP for the entire euro area. So if Germany is seeing price distortions that the rest of Europe is not experiencing, the ECB will not be giving it that much weight in its policy-setting. And yet German inflation angst could rise.

Germany has a history of being ‘unreasonable’ about inflation. In the interwar period with the development of hyper-inflation, Germans developed a strong aversion to even a whiff of inflation. So Germany, nationally and down to populist roots, has less tolerance for inflation than just about any other European nation. While many central banks are willing to shift their focus to core prices when odd oil or food price events ‘distort’ headline inflation, Germany is less likely to do that. Of course, the just-released index at hand in May is the PPI and the PPI is not the price index that used to be targeted by the Bundesbank and it is not the one targeted by the ECB today. In fact, it’s important to remember that ECB targets the headline HICP for the entire euro area. So if Germany is seeing price distortions that the rest of Europe is not experiencing, the ECB will not be giving it that much weight in its policy-setting. And yet German inflation angst could rise.

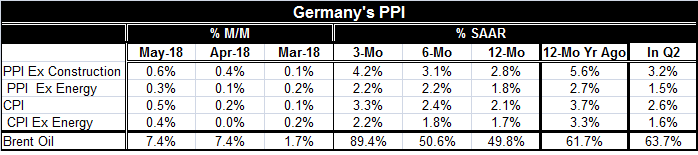

German trends show sequential inflation rising on all fronts from 12-month to six-month to three-month. Year-on-year inflation leaves headline inflation on the PPI and CPI in excess with respect to the ECB’s target for the euro area HICP. But ex-energy inflation in Germany on both counts is still well below the 2% mark. And the chart shows that technical calculations aside, there is not much upward momentum in any of these inflation measures.

The ex-energy PPI and the ex-energy CPI both do show rising progressions inside one year, but are more on technical calculations than they appear to be ‘worrisome’ trends.

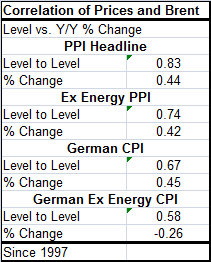

The table to the left shows that when oil prices are rising, there tends to be more inflation imparted to all these measures except to the ex-energy CPI expressed as percentage changes; there, the correlation is low and also negative.

The table to the left shows that when oil prices are rising, there tends to be more inflation imparted to all these measures except to the ex-energy CPI expressed as percentage changes; there, the correlation is low and also negative.

These correlations suggest that the rise in German ex-energy CPI inflation is not because of oil.

Still, Brent prices have been rising very strongly. They too are accelerating from 12-month to six-month to three-month. And Brent prices are rising at an 89% annual rate over the last three months compared to 50% over 12 months. That’s a lot of energy ‘juice’ to dismiss.

While Mario Draghi is still speaking of being measured with policy, there is a bit more of an inflation drumbeat in the background. However, in this recovery we have seen inflation, especially PPI inflation, come and go all on its own or in reaction to oscillating oil prices and oil prices are very much in play again.

At the moment, there is also a new risk in town as tariffs are being put on back and forth. The EU is ready to impose countervailing tariffs on U.S. products this Friday. While tariffs do raise import prices and to that extent heighten inflation risk, they also disrupt trade and can reduce economic activity and result in the opposite impact, weaker growth with even lower inflation eventually. So central banks have to be careful how they play their cards and what they gear their policy reactions to with a trade war in progress. It remains to be seen if this trade war will be a series of skirmishes or if it will become a hardcore growth-distorting war.

Europe will want to focus on the ‘unfairness’ of aluminum and steel tariffs and calling import reliance a national security risk. The U.S. will want to look at a broader legacy including Germany with the highest ratio of current surplus to GDP in the world as evidence of ongoing unfair trade. Whether the two sides ever get beyond the pot calling the kettle black will be the key. But the EU is a difficult block to negotiate with because there are so many national interests that underlie European policy.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief