Global| Oct 23 2018

Global| Oct 23 2018German PPI Makes Sharp Gain on Rising Energy Costs

Summary

The German PPI rose by a strong 0.6% in September, but the PPI excluding energy gained just 0.1%. The sequential inflation forces over shorter horizons show more pressure for headline PPI and CPI measures while the ex-energy measures [...]

The German PPI rose by a strong 0.6% in September, but the PPI excluding energy gained just 0.1%. The sequential inflation forces over shorter horizons show more pressure for headline PPI and CPI measures while the ex-energy measures show diminishing inflation forces at work. This division could be a big problem for policymakers depending on how they view what they see.

The German PPI rose by a strong 0.6% in September, but the PPI excluding energy gained just 0.1%. The sequential inflation forces over shorter horizons show more pressure for headline PPI and CPI measures while the ex-energy measures show diminishing inflation forces at work. This division could be a big problem for policymakers depending on how they view what they see.

Fortunately, in the EMU, Mario Draghi, President of the European Central Bank, has adopted the stance of looking more at ex-energy prices during periods when energy prices are moving abruptly. The table below shows that Brent oil prices are up by 42% over 12 months, up at a 40% pace over six months and still rising at a nearly 18% pace over three months. Energy is giving headline inflation fits, but little of its pressure is filtering down into non-energy prices. The ex-energy PPI and CPI both are showing very contained inflation and inflation momentum with both well below the ECB’s target pace of a bit less than 2% for inflation. Formally, the ECB target applies to the HICP prices and not to CPI or to PPI prices and never to any price index at the local level. But it is also useful to look at local level inflation since local inflation is the building block of EMU-wide inflation. And in the case of Germany, it is a very important building block since Germany carries a substantial weight in the EMU economy.

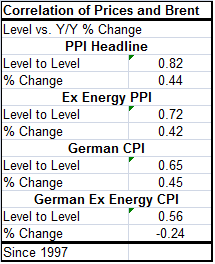

The table on the left delivers some information about inflation and how oil prices relate to the headline price indexes in Germany as well as how well-correlated is energy to other various inflation metrics in terms of their year-on-year percentage changes. Evaluating year-to-year changes is what the ECB does when it looks at prices and assesses inflation relative to target. The Brent price level has a relatively high correlation with price index levels. But in terms of year-over-year percentage changes, the correlation is much lower. For year-on-year inflation, the correlation between the German ex-energy CPI and Brent is negative. When energy prices rise, other non-energy consumer prices in Germany fall.

The table on the left delivers some information about inflation and how oil prices relate to the headline price indexes in Germany as well as how well-correlated is energy to other various inflation metrics in terms of their year-on-year percentage changes. Evaluating year-to-year changes is what the ECB does when it looks at prices and assesses inflation relative to target. The Brent price level has a relatively high correlation with price index levels. But in terms of year-over-year percentage changes, the correlation is much lower. For year-on-year inflation, the correlation between the German ex-energy CPI and Brent is negative. When energy prices rise, other non-energy consumer prices in Germany fall.

This correlation, while odd-seeming to non-economists, reflects the way that economists see oil prices impacting the economy. It is typical for people to say that rising oil prices are inflationary. And they do send of pulse of inflation into whatever headline price index is monitored. But if monetary policy does not accommodate the inflation pulse, it gets squeezed out of the economic system by the process we see memorialized in the German ex-energy inflation correlation: other prices fall to make room for higher energy prices in the context of a fixed budget and steady monetary policy.

To understand why this happens, consider a person on a fixed income. What do they do- what can they do- when energy prices rise? Energy use is relatively inelastic - in the short run anyway. You drive X miles to work; you heat or air-condition your home; you cook food, etc. There is little room to economize in the short run. In the long run, you can buy an energy efficient vehicle or move closer to work or install solar panels on your roof or do a hundred things to lessen your dependence on energy. But not in the short run; there you pay the piper. So when energy prices go up, your total energy bill rises leaving fewer funds to be spent on non-energy items. Because of this, a rise in energy prices acts like a reduction in income for other goods and it is deflationary for them as a whole. The household budget to buy non-oil items goes down and that puts downward pressure on non-oil item prices. Over time, energy prices themselves may cause some non-energy prices to rise since merchants must cover all their costs. But in the short run, there are very different energy/non-energy economic forces playing out.

Under such conditions, keeping a hard-headed target on headline inflation might not be the best thing to do since oil prices will likely cause headline inflation to balloon initially as the economic system digests the higher prices and eventually deals with them. With the higher oil price persisting the after the fact of a price hike the CPI index likely to be (forever) higher as well but after the impact of higher oil prices work into the headline and through the system the pace of inflation is unaffected if the central bank has not accommodated it. It is only during the period when the relative price of oil is still rising that even headline inflation is affected. So a policy that targets headline inflation strictly in the short run might raise rates during an oil price hike episode only to have to cut them later. The process of raising oil prices by itself puts some stress on an economy by forcing consumers to change their spending habits to deal with the higher relative prices of oil. It is not a good idea to raise rates during such a period and put the economy under even more stress unless that is absolutely necessary. But it is important to send a message that monetary policy is not going to accommodate the oil price rise. If consumers are not inculcated to the belief that the central bank will hold the line and will be containing inflation, they may act differently and promote the spread of inflation. This is a question both of how the central bank acts and how it is perceived; what its credibility is.

Euro area countries had adopted different ways of dealing with theses tensions prior to the formation of the currency union. Southern European countries were less concerned about the price level and price ‘stability.’ They were more likely to let higher inflation play out to deal with a hike in the relative price of oil. On topical correlations back to 1998, the highest positive correlations between core HICP inflation and Brent oil price increases are (in order from highest to lowest) Spain, Italy, Portugal, France, and Greece. Negative correlations (inversely ordered) are from Belgium, the Netherlands, Germany, Finland, and Austria. Old habits die hard. Even though the Southern European economies are in the EMU and face the same monetary conditions as the hard currency countries, the reactions to energy prices have been different and remain to some extent different among members in the same currency union. And this stems from the legacy of when Southern European nations used to let rising oil prices boost inflation and then allowed their currencies to drop to restore competiveness. The countries of Northern and Western Europe generally did not do that.

Behaviors remain ingrained in the EMU and continue to affect the way that economies operate. Still, inflation in the EMU has stayed below target and now a greater proportion of members are conforming to the region’s target on their own. For the early years of the EMU, the ECB hitting its target was mostly because Germany ran a very low inflation rate and had a large weight while smaller economies often ran higher inflation but that did not contribute much to overall inflation in the EMU where economic data are size-weighted. However, that sort of price and inflation divergence in the EMU tended to exacerbate competitiveness issues. Prior to the Great Recession, the standard deviation of inflation across EMU members was greater than 1%; since 2015, it has averaged 0.6%.

Has German medicine been a cure-all or snake oil?

Still, the hard currency countries of the EMU have longer traditions of keeping a lid on inflation and have the discipline to do it that is reflected in consumer behavior. Countries in Southern Europe still are learning this lesson. German medicine did a lot to pull into line Greece, Spain, Portugal, and Italy. However, in Italy, there has been a great cost of lost growth. Real GDP in Italy is still below its precession level of about one decade ago and Italians do not view austerity as having ‘worked’ for that reason. And for that reason, they now are unwilling to continue with it and instead seek budget flexibility to restart growth – flexibility that is prohibited under EU Commission rules under the Maastricht criteria. So Europe may yet come to blows over that.

While inflation in Germany is tempered, oil prices as always make waves. Some countries ride the waves better than others. Oil prices themselves do not cause a stability threat in the EMU and for now neither does inflation. But the after effects of the inflation medication have been debilitating in Italy and we will have to see where that realization takes us.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief