Global| Jun 20 2017

Global| Jun 20 2017German PPI Backtracks in May as Oil Falls to 7-month Low in "Real Time"

Summary

Virtually all major swings on this time line in the German PPI are caused by swings in oil prices. But now Brent is falling. In the most topical daily data venue Brent has hit a 7-month low in price. An oil glut is eviscerating OPEC. [...]

Virtually all major swings on this time line in the German PPI are caused by swings in oil prices. But now Brent is falling. In the most topical daily data venue Brent has hit a 7-month low in price. An oil glut is eviscerating OPEC. We certainly have to view the Saudis in this environment as sitting back and waiting for the pain felt by other members to become so great that they will be willing to take the next step which would be to not just to extend current quotas but to lower them. Inflation watching in this environment has not much to do with macroeconomic policy or monetary policy as with OPEC watching.

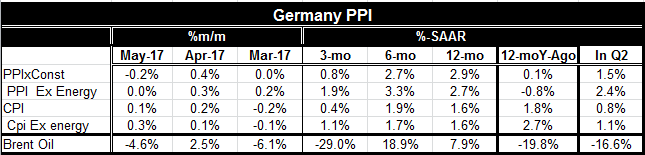

PPI trends are withering

PPI inflation trends for the German headline are working lower from a 2.9% pace over 12-months to a 2.7% pace over 6-months to a 0.8% pace over three-months. The ex-energy PPI does not step down quite as smoothly but the three-month pace is much lower than the 6-month or 12-month pace. The CPI and CPI ex energy each have the same properties as the PPI ex-energy- not trend weakness- but a sharp fall-off in the pace over three-months. And, in that, the price patterns follow Brent which has a "modest" 7.9% gain over 12-months, an 18.9% annual rate surge over 6-months and a 29% annual rate plunge over three-months. Brent continues to call the tune on inflation even over relatively short periods.

PPI and CPI show same vulnerabilities

The chart below plots the ex-energy PPI VS Germany's ex-energy CPI. There you see what small import PPI inflation has for German CPI prices and trends. The CPI trend does sway to and fro as the PPI swing wildly up and down but the transmission of influence is weak.

Not that much more growth...

For OPEC and oil prices there may be some help from growth, but in truth that looks to be still too weak and too far down the road to wait for. Here is what we have learned about the growth outlook today and recently:

- Today the Federation of German Industries (BDI) said it looks for 1.6% growth in the year ahead but warns on the importance of the exchange rate which helped to boost growth last year by 1.9%.

- The IFO raised its growth outlook for Germany in 2017 to 1.8% and projected 2% for 2018.

- Commerzbank expressed confidence that German growth would continue solid

- In the UK the Confederation of British Industry (CBI) projected 1.6% growth for the UK in 2017 and a weaker 1.4% in 2018. The CBI is clearly concerned about how the Brexit talks go.

- BOE head, Mark Carney, spoke up today saying that the time was not right for the UK to be hiking rates. He referred to mixed signals for the consumer and investment activity and weak wage growth which is lagging behind inflation.

- In Switzerland the State Secretariat for Economic Affairs looks for a growth slowdown to 1.4% instead of 1.6%.

- In the US, Federal Reserve officials released forecasts of their own recently (known as their SEPS, survey of economics projections) which foresee more or less the same 2% growth in the US for this year and next year.

- In Asia, there may still be slowing in China; Japan appears to be marking time with no inkling of an idea when its excess stimulus might stop or be reversed.

Still...policy changes loom

While the German outlook is a bit more upbeat the recent forecasts that have been issued do not brighten the outlook for global growth all that much. However, we are close to seeing policy changes afoot as, despite the Carney comments, at the BOE meeting this month the policy decision was decidedly split. In the US the Federal Reserve is engaged in tightening and seems determined to carry on for more as well as to start to shrink its balance sheet. The ECB has warded off the demons of tightening but even the ECB's own language has been morphing as pressure from Germany has stepped up. The ECB may not be far from undertaking its own policy of lesser accommodation and eventual balance sheet shrinkage.

The 64 Trillion dollar question...

The big question in this environment for an OPEC concerned about oil prices, and for central banks concerned to keep growth and inflation each on path is what happens to growth once central banks take the training wheels off policy. The sense we have that growth may be stirring is one gotten with still stimulative policies in place. And despite some light at the end of the tunnel this light is not bright. Some see a growth that has a bit more of a global element to it. But, the fact that inflation can flare then recede and may only have flared on the back of rising oil prices creates a different back story for growth and inflation risk. In truth central banks globally have misjudged inflation and growth repeatedly in this cycle. They set excessive expectations for growth and for the horizon and scope for inflation to rise several times in this cycle. Central bankers generally were slow to mount defense of growth in the recession and have been too quick to begin to back off. Several central banks began monetary tightening programs that they had to rescind. In the US a tightening program was started way too early in 2015 and was so far out of step with what the economy could swallow that it took the Fed a year to bring a second rate hike in behind the first move. When Ben Bernanke was the Fed Chair (Bernanke an expert on the Great Depression era) he had noted on several occasions that after a significant downturn and financial crisis the most consistent policy mistake was to try to get back to normal too soon. So are we making that same mistake again? Or have we all waited long enough? That is the essential question. And watching to see if inflation can or will evolve is one way to help answer it - that is watching inflation apart from oil.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief