Global| Apr 20 2018

Global| Apr 20 2018German PPI Accelerates

Summary

The German year-on-year PPI has generally been decelerating since early 2017. Technically, the year-on-year PPI has decelerated for six months straight with this month’s acceleration being the first in the period. This is despite the [...]

The German year-on-year PPI has generally been decelerating since early 2017. Technically, the year-on-year PPI has decelerated for six months straight with this month’s acceleration being the first in the period. This is despite the month’s PPI rise being only a gain of 0.1%.

The German year-on-year PPI has generally been decelerating since early 2017. Technically, the year-on-year PPI has decelerated for six months straight with this month’s acceleration being the first in the period. This is despite the month’s PPI rise being only a gain of 0.1%.

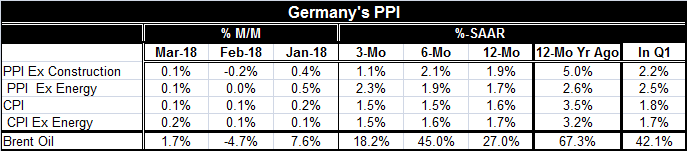

The PPI headline (excluding construction) and the PPI excluding energy each rose by 0.1% in March. Over three months, the PPI is rising at a 1.1% annual rate. The ex-energy PPI also rose by 0.1% in March and is rising at a 2.3% annual rate over three months. The headline does not have a clear end, but the ex-energy PPI is accelerating.

The 12-month PPI increase show a rise of 1.9%; the core is up by a lesser 1.7%. The CPI has reverse trends with the headline rising 1.6% and the CPI excluding energy’s gain at a 1.7% pace.

Oil prices have been rising for a while. They are up over 12 months at a 27% annual rate and over six months at a 45% annual rate. The pressure is less over three months at an 18.2% annual rate. That pressure obviously makes keeping a lid on inflation more difficult.

However, on this timeline the PPI core is clearly accelerating. The CPI has actually trended a bit lower and so has the CPI excluding energy. The PPI chart clearly shows that there was a bit of an inflation scare in 2016. But throughout 2017, inflation pressures dissolved.

The PPI chart is now showing a confluence of trends. While the year-on-year path is still gradually moving lower, both the three-month and six-month rates of change show rising trends. PPI acceleration is clearly underway despite the ambiguous message from the sequential growth rates. And still the trends are just coalescing around the 2% mark.

Only a few European nations have reported their March PPI results. Among them, the U.K. shows a PPI drop in March along with Portugal and Austria (WPI). Denmark shows a 0.1% increase. Denmark and Austria show sequential decelerations in the pattern of their price gains. There are no clear accelerations in train for the period among the current reporters. Denmark, the U.K. and Germany have unclear patterns in their respective PPI gains.

Inflation is not yet clearly taking hold in Europe. But as with U.S. trends, price declines are no longer a clear and present risk. Inflation is still generally below the ECB’s 2% ceiling. It is uniformly below 2% on all horizons for the CPI gauges; only the more volatile PPI is showing some excessive gains over spans of one year or less. Inflation is not yet at the forefront of policy, but fears of inflation are driving policy globally.

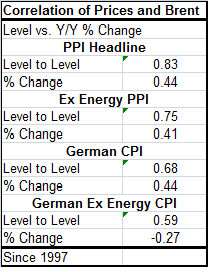

Energy remains an important part of the inflation picture and as always the energy picture is clouded by technical factors as well as politics. Fracking in the U.S. has added to supply and to downward pressure on oil prices. But problems in peripheral global suppliers as well as new hostilities in the Middle East have pressured oil higher. Output restrictions by OPEC members and Russia have added to the oil price stress. The new Saudi Crown Prince has said his new objective for oil is $100 per barrel. U.S. President Donald Trump has been quick to tweet that high oil prices would not be tolerated. Of course, oil is always complicated, but with the Saudis planning to sell shares in Aramco, higher oil prices would raise the value of these sales to the Kingdom. However, since the Saudis have massive oil reserves, they have always been champions of more modest pricing so that oil maintains its value over the long run. Too-high oil prices would encourage more conservation and the development of more unconventional supply methods. So the position of the new Crown Prince is actually very hard to put in context. It would represent a break with history. It may only be a marketing ploy to increase stock prices for Armaco sales. Still, higher oil prices would make the inflation situation more difficult to control and could prompt central banks to more readily raise rates.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief