Global| Mar 09 2018

Global| Mar 09 2018German Output Slows; European Trends Are Mixed

Summary

German industrial production edged down 0.1% in January, marking the second monthly drop in a row. However, none of the sector components have dropped twice in a row and the three-month growth rate for total IP is at a 9.1% annual [...]

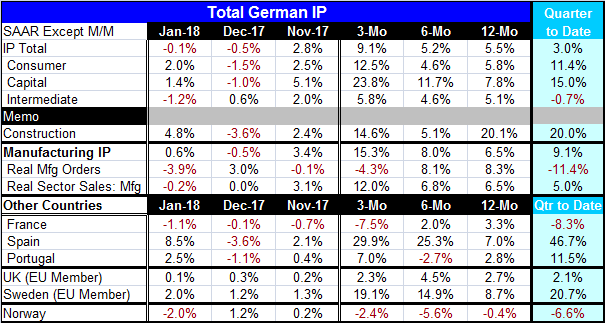

German industrial production edged down 0.1% in January, marking the second monthly drop in a row. However, none of the sector components have dropped twice in a row and the three-month growth rate for total IP is at a 9.1% annual rate with capital goods at a 23.8% pace leading all sectors higher.

German industrial production edged down 0.1% in January, marking the second monthly drop in a row. However, none of the sector components have dropped twice in a row and the three-month growth rate for total IP is at a 9.1% annual rate with capital goods at a 23.8% pace leading all sectors higher.

The overall IP trend shows a gain at a pace of 5% to 6% over 12 months and six months that steps-up to a 9.1% pace over three months. Consumer goods output is on a 4.5% to 6% growth range over 12 months and six months then steps-up to a 12.5% pace over three months. Intermediate goods growth is simply in a 4.5% to 6% range over all three horizons. Capital goods is not just the leading growth sector over three months, but it has been accelerating from a pace of 7.8% over 12 months to 11.7% over six months to 23.8% over three months,

Construction output has been more variable, but IP for that industry group is up at a 20.1% pace over 12 months and only somewhat slower over three months.

Manufacturing IP shows a drop in December and a nearly identically-sized gain in January. Sequential growth for manufacturing moved up steadily from a 6.5% pace over 12 months to an 8% pace over six months to 15.3 % over three months.

EMU members France, Spain and Portugal also have their IP results out on the early side. But there is little here to learn about trend. French IP is sinking sequentially and has three straight months of output declines. Spain shows strong double-digit growth that accelerates over six months and three months. Portugal's growth path is erratic but seems to be improving. Among other European reporters in the table, U.K. output growth seems steady below a 3% pace. Sweden shows IP accelerating well into double digits. Norway logs a string of sequential negative rates of growth and posts a decline in output in January to top it all off.

Over the quarter-to-date (QTD), German growth is at the 3% mark, being pulled down by intermediate goods. France and Norway log output declines in the QTD. Spain, Sweden and Portugal log double-digit growth in the QTD. Meanwhile, growth in the U.K. is up at barely a 2% pace on a QTD basis.

German output shows some recent weakness in this report. German exports also have foundered, falling in January after being flat in December. Even so German exports log a 15% growth rate over three months and export growth is still accelerating. But real export orders actually are falling over three months. So there is a crucial mass of orders, output and exports data that read 'weak' for Germany, although there is no fundamental reason to expect German growth to back off.

Globally, the ongoing sluggishness has been in Asia vs. the EMU where growth is on an upswing showing some degree of strength. It is reasonable that the European revival would not continue at this pace and would slow. One missing piece is still that the European consumer sector has not looked strong. But there are no grounds for any concern about growth. The ECB met this week and swept away its bias for stepping up securities purchases in the event of unexpected weakness. In Japan, the Bank of Japan announced that fiscal 2019 would probably be its end game for inflation stimulus. The U.S. continues to raise rates; today's employment data for February will keep the Fed rate hike cycle alive or even push it ahead a bit.

Winter has been harsh and it's possible that the German data are reflecting this, but usually when weather is the culprit it's the construction sector that does not perform and so far it is doing well. However, both French and German IP were hit in January and that could be a common weather impact. There were some severe snow storms in Europe in January; in fact, bad weather is continuing. It is harder to explain how weather might be to blame for weaker orders. It is more likely that this period of revival in output is a shifting of the gears to a pace that is more sustainable and that the process of slowing down is not entirely smooth. For now that is my working hypothesis of what the German data are telling us.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief