Global| Oct 05 2018

Global| Oct 05 2018German Orders Rebound But Not Enough to Reinstate a Positive Trend

Summary

The graphic on German orders is quite clear. Domestic and foreign order growth saw German firms peaking in late-2017 or early-2018 with domestic orders peaking first. Since then there has been a slowdown in place that has progressed [...]

The graphic on German orders is quite clear. Domestic and foreign order growth saw German firms peaking in late-2017 or early-2018 with domestic orders peaking first. Since then there has been a slowdown in place that has progressed to a rather severe state.

The graphic on German orders is quite clear. Domestic and foreign order growth saw German firms peaking in late-2017 or early-2018 with domestic orders peaking first. Since then there has been a slowdown in place that has progressed to a rather severe state.

Blame it on the U.S. but not all of it...

While the German situation may be exacerbated by the U.S.-China and other trade fears and actions, the German order slowdown preceded all that. Domestic German orders had floundered through 2014 and 2015 then picked up in 2016, reached an effective peak in September 2017 in their year-over-year pace and then year-on-year growth turned negative as soon as December of that year. In the nine months from December 2017 to date, domestic orders are contracting year-over-year in five of them. Foreign orders are falling year-on-year only for two months in a row (July and August of 2018).

German total orders and foreign orders show sequentially deteriorating orders for 12-months to six-months to three-months. Domestic orders, while contracting on all those timelines, are slightly less weak over six months than they are over 12 months interrupting the sequence of persistent deterioration. However, domestic orders have a deeper 12-month decline than foreign orders.

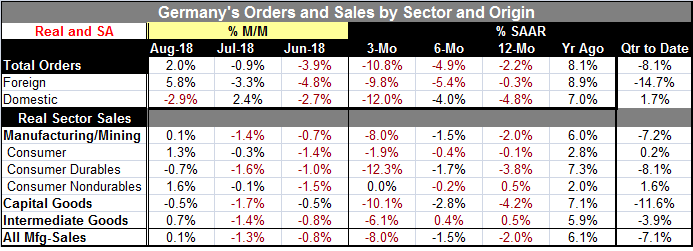

There is a clear slowing in place and a 2% rise in orders for August is wholly on the back of a 5.8% spurt in foreign orders that only blunts the 2.9% decline in domestic orders.

In the quarter-to-date (two months into the third quarter), overall orders are falling at an 8.1% annualized pace relative to their Q2 average. Foreign orders are off at a 14.7% pace and domestic orders are managing a small gain at a pace of 1.7%.

Broad weakness

Real sector sales show weakness up and down the line, as the table clearly demonstrates over sequences of 12-months, six-months and three-months. In the current month of August, all manufacturing sales rise by 0.1%, a very small rebound, after declines of 1.3% and 0.8% in each of the past two months. August shows a 1.3% rise in consumer goods orders on a gain of 1.6% by nondurables while capital goods orders decline and intermediate orders rise.

Sequential slowing if not declining

Turning back to the sequential sales trends over three months, orders fall and decelerate in each category with the exception of being flat for nondurable goods sales over three months. Over six months, real sales fall in all categories except for intermediate goods. Year-on-year all categories show declines except intermediate goods and nondurables, but all categories without exception show deceleration from their respective year-ago growth rates.

Looking at year-over-year growth rates, the weakness is being led by capital goods which generally is the leading sector for Germany while the consumer sector usually lags. Capital goods sales are falling by 4.2% over 12 months. The consumer durables sector is the next weakest category with sales falling by 3.8%. Intermediate goods sales actually are up by 0.5% over 12 months.

A lot of prevarication for so little optimism

These results fit perfectly with the PMI data from Markit. The German foreign orders series reaches its peak at the same time as German orders and they decline more or less in step. Germany and the EMU manufacturing index are also in step. There is a broad slowing in Europe for the industrial sector. And it all seems broader than just owing to trade wars. But then there is also the impact from trade wars, there is also the ECB preparing Europe for less accommodation, there is also a very deteriorated geopolitical back ground, there is also a coming shock from Brexit, there is also the OPEC situation and fast rising oil prices, and there is also the ‘Italian problem.’ I’m sure there are some positives hiding here somewhere, but I’m not exactly sure where to find them.

Goldilocks and the three bears- remember them?

Everyone seems hung up on the Goldilocks scenario. But remember what that means. The best case scenario I can think of here is Goldilocks: a slowdown that leaves growth in place but not too much of it. Weak enough so that inflation is not generated. Not too much growth not too little - just right. The problem with that is that the story of Goldilocks is a fairy tale. And Goldie was accompanied by three bears and that makes the odds bad; three to one for bad news against good. Too much growth, or inflation or a geopolitical flare up is all it would take I to unseat Goldie. I think the risk/reward ratio is going South fast, time to take stock. But also it’s time to handicap which of the risks will become an operative problem. On that score, I still think central banks are the biggest risk. The real risk is more to insufficient growth held back to soon by central bankers that handicap the future risks but have lost track of the lags from the policies they have implemented as well as other negative events they have discounted because they don’t wish to face them. This applies mostly to the U.S., of course. But all central banks are managing expectations to less accommodation ahead and none seem worried about the environment. They worry too much about inflation and expend too much energy fighting what does not exist. As central banks are engaged to fight the wrong battle, in the end not only will they lose but so will the economy.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief