Global| Jul 06 2017

Global| Jul 06 2017German Orders Make Partial Rebound in May

Summary

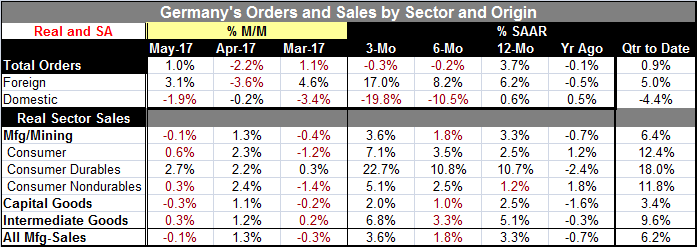

German factory orders gained 1% in May as foreign orders surged by 3.1% against a drop of 1.9% in domestic orders. Domestic orders are now lower for three consecutive months. Domestic orders are some 7.7% lower than their peak in this [...]

German factory orders gained 1% in May as foreign orders surged by 3.1% against a drop of 1.9% in domestic orders. Domestic orders are now lower for three consecutive months. Domestic orders are some 7.7% lower than their peak in this cycle reached back in December of last year.

German factory orders gained 1% in May as foreign orders surged by 3.1% against a drop of 1.9% in domestic orders. Domestic orders are now lower for three consecutive months. Domestic orders are some 7.7% lower than their peak in this cycle reached back in December of last year.

In May, foreign orders increased by 3.1% on the previous month. This is a rebound from April's 3.6% order drop which itself was a fall off from a 4.6% gain in March. Foreign orders have been extremely volatile. But in the context of volatility, orders have generally been growing. Still, in the wake of even the large gain in May, foreign orders are 0.6% off their cyclical peak which is just a few months old, having been reached in March of this year. As for order allocation, new orders from the euro area were up 1.7% in May while new orders from other countries increased 4.0% compared to April.

Sector orders were mixed in May. Manufacturers of intermediate goods saw new orders fall by 0.7% compared with April. The manufacturers of capital goods showed increases of 2.6% on the previous month. For consumer goods, a decrease in new orders of 2.9% was posted.

Sequentially orders are deteriorating with 12-month growth at a 3.7% pace, six-month growth at a -0.2% pace and three-month growth at a -0.3% pace. But this pattern which obviously is not very strong or definitive given the volatility in orders recently is undercut by a foreign profile of strong acceleration against a domestic profile of aggressive deceleration. In the quarter-to-date as well, foreign orders are up at a 5% pace while domestic orders are falling at a 4.4% pace.

Sector sales show overall manufacturing sales drop by 0.1%. In May, there are monthly declines in all sectors except for consumer durable goods where sales spurted and have been on a tear. Sequential growth rates of real sales show no clear pattern. By sector, consumer sales are on an accelerating path with consumer durables strongly accelerating and nondurable also on a milder acceleration path. Capital goods show expansion on all horizons but with no clear acceleration/deceleration. Intermediate goods sales also show no clear acceleration/deceleration patterns but show solid growth on all profiles.

On balance, sector sales point to ongoing growth but at a speed that is not easy to pin down. Orders show deceleration overall but show a true tug-of-war between strong foreign orders and weak domestic orders.

The foreign/domestic order split is hard to rationalize for a German economy that seems to be doing quite well with a record low post unification unemployment rate. It may not be surprising to see that the industrial sector has export-led growth, but the sort of domestic order weakness portrayed here is quite a surprise. It raises some questions about what is really going on in Germany and certainly raises questions about how much domestic demand Germany is offering in a world of slack demand where Germany is running the largest current account surplus as a percentage of GDP and helping itself to scarce demand all around the world while apparently offing up little of its own at home and instead pursuing a program of fiscal austerity.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief