Global| Jun 05 2008

Global| Jun 05 2008German Orders Lose Their Froth Faster Than Day-old Beer

Summary

As the dollar fell and euro rose German authorities gloated about the resilience of their economy. German economic statistics have largely remained firm and vibrant in the face of ever diminishing competitiveness, as the euro rose. [...]

As the dollar fell and euro rose German authorities gloated

about the resilience of their economy. German economic statistics have

largely remained firm and vibrant in the face of ever diminishing

competitiveness, as the euro rose. Well the bloom is off the rose (or

the rise) now. Orders are now giving that erstwhile optimism is

rightful comeuppance. German orders have now fallen month-to-month for

FIVE straight months lead by five straight months of foreign orders

dropping. During this span, domestic orders fell in three months, were

flat in one and rose in another - the most recent month of April posted

a small gain for domestic orders. German foreign order weakness is

concentrated within the Euro Area rather than in transactions that more

explicitly cross exchange rate lines. Still, within the Zone German

‘exporters’ continue to face competition from other producers domiciled

outside of the zone and producing with other currency-based production

costs… like the dollar.

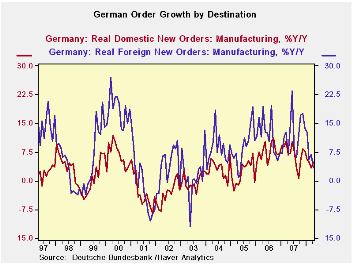

For the moment German own-country orders are holding up better

than foreign orders. Both sets of orders are still UP on the year (last

12-months), foreign orders by 3.4% and domestic orders by 4.8%, But

over three and six months foreign orders are dropping at an astonishing

-19% and -10% rate respectively. Meanwhile, over three and six months,

domestic orders’ annual rates of decline are the far more modest pace

of -1.7% and -0.9%. That’s so far. No country, especially within the

strong currency Euro-Area is an island, and Euro Area weakness abounds.

Still dogging Germany is the fact that domestic consumption

has not picked up. Orders for consumer goods lead the way lower.

Despite a sharp April bounced back in capital goods orders the series

remains mired in three-month and six-month negative growth trends with

weakness accelerating. Its fellow EMU members are fading fast, just as

growth is fading also in the UK.

The central banks in EMU and the UK are continuing to hold

firm to fight food and energy inflation. Meanwhile each looks set to

open up a larger GDP gap which will help to fight inflation along with

that strong euro, at least for EMU. Manufacturing sales are starting to

lose their zest in Germany. If the ECB was once worried about second

round effects if will now find its region populated by workers that are

going to be more concerned about jobs than about wages. Eventually that

development will breed different behavior on the part of the ECB but

that is still a long way off.

| German Orders and Sales By Sector and Origin | ||||||||

|---|---|---|---|---|---|---|---|---|

| Real and SA | % M/M | % Saar | ||||||

| Apr-08 | Mar-08 | Feb-08 | 3-Mo | 6-Mo | 12-Mo | Yr-Ago | QTR-2-Date | |

| Total Orders | -1.8% | -0.5% | -0.6% | -11.1% | -5.7% | 4.0% | 6.9% | -13.2% |

| Foreign | -3.8% | -0.3% | -1.1% | -19.2% | -10.1% | 3.4% | 6.8% | -23.4% |

| Domestic | 0.3% | -0.8% | 0.0% | -1.7% | -0.9% | 4.8% | 7.0% | -1.0% |

| Real Sector Sales | ||||||||

| MFG/Mining | -0.9% | -0.6% | -0.1% | -5.8% | -3.0% | 5.2% | 5.1% | -7.3% |

| Consumer | -1.8% | 0.2% | -1.8% | -12.9% | -6.7% | -0.9% | 2.0% | -13.0% |

| Cons Durables | 0.2% | -0.9% | -0.3% | -4.0% | -2.0% | 3.5% | -0.1% | -3.0% |

| Cons Non-Durable | -2.1% | 0.3% | -2.0% | -14.4% | -7.5% | -1.6% | 2.3% | -14.5% |

| Capital Goods | 2.4% | -2.6% | -0.8% | -3.9% | -2.0% | 9.5% | 4.5% | 2.3% |

| Intermediate Goods | -4.2% | 1.6% | 1.7% | -4.1% | -2.1% | 3.5% | 7.7% | -14.9% |

| All MFG-Sales | -0.8% | -0.6% | -0.2% | -6.2% | -3.2% | 4.8% | 4.8% | -7.3% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.