Global| May 07 2009

Global| May 07 2009German Orders In Surprise Rebound

Summary

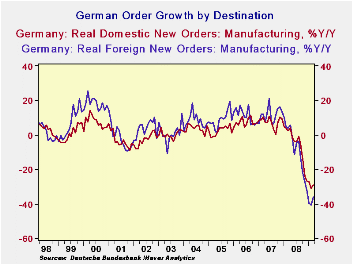

Foreign orders that had been falling a bit faster than those from domestic sources were up by a sharp 5.6% m/m in May compared to a rise of 1.1% for orders from domestic sources. German factory orders from outside the 16-nation euro [...]

Foreign orders that had been falling a bit faster than those

from domestic sources were up by a sharp 5.6% m/m in May compared to a

rise of 1.1% for orders from domestic sources. German factory orders

from outside the 16-nation euro region rose 5.1 percent in March from

February indicating that much of the orders strength was not just

foreign but outside the zone as well. Export orders for investment

goods rose 9.1 percent, driven by demand from within and outside the

euro area.

Data trends however have swallowed up the good news. Three

month growth rates of orders and sales are still declining faster than

they did over six-months. Order growth is still accelerating in the

downward direction. In the quarter the drop in sales and in orders

remains horrific.

Even so the rise in orders is an encouraging sign. Even if the

sharp rise this month has been crushed by the trends of past weakness,

it is step in the right direction. This is how the trip toward

stability starts. Germany is getting its break in terms of improved

demand from external sources. Germany’s domestic initiatives- as well

as initiatives from the e-Zone itself- are not yet bearing much fruit.

At least the ECB took some further steps today in monetary policy to

cut rates and to shoulder added policy moves.

| German Orders and Sales By Sector and Origin | ||||||||

|---|---|---|---|---|---|---|---|---|

| Real and SA | % M/M | % Saar | ||||||

| Mar-09 | Feb-09 | Jan-09 | 3-MO | 6-Mo | 12-Mo | Yr Ago | QTR-2-Date | |

| Total Orders | 3.3% | -3.1% | -6.7% | -23.9% | -12.8% | -33.1% | 3.2% | -46.5% |

| Foreign | 5.6% | -0.9% | -10.9% | -24.5% | -13.1% | -36.0% | 3.9% | -53.7% |

| Domestic | 1.1% | -5.5% | -1.8% | -22.6% | -12.0% | -29.4% | 2.2% | -36.9% |

| Real Sector Sales | ||||||||

| MFG/Mining | 1.5% | -4.7% | -6.6% | -33.7% | -18.6% | -21.9% | 3.3% | -45.0% |

| Consumer | -0.4% | -3.3% | -6.0% | -33.0% | -18.2% | -11.7% | -0.9% | -25.7% |

| Cons Durables | -1.4% | -7.8% | -2.2% | -37.4% | -20.9% | -22.9% | 0.1% | -40.2% |

| Cons Non-Durable | -0.3% | -2.6% | -6.6% | -32.4% | -17.8% | -9.7% | -1.0% | -22.8% |

| Captial Gds | 4.8% | -5.2% | -9.4% | -34.5% | -19.1% | -24.8% | 6.0% | -53.9% |

| Intermediate Gds | -0.7% | -3.3% | -4.6% | -29.6% | -16.1% | -24.6% | 4.0% | -44.0% |

| All MFG-Sales | 1.5% | -4.8% | -6.6% | -33.5% | -18.5% | -22.1% | 3.3% | -45.3% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief