Global| Dec 06 2017

Global| Dec 06 2017German Orders: Despite Solid/Strong Orders Gain, Is There Trouble Brewing?

Summary

Germany now has a real string of order increases in train. There are increases in orders in October after gains in September and August. In addition, both foreign and domestic orders have a string of gains for three consecutive [...]

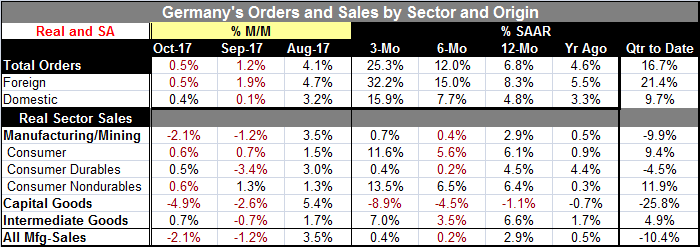

Germany now has a real string of order increases in train. There are increases in orders in October after gains in September and August. In addition, both foreign and domestic orders have a string of gains for three consecutive months. That is unusual. The last time total orders, domestic and foreign orders were all up for three straight months together was November 2006 through February 2007 - over a decade ago. And this string builds on a strong base as the August order increase was a gain of 4.1%.

Germany now has a real string of order increases in train. There are increases in orders in October after gains in September and August. In addition, both foreign and domestic orders have a string of gains for three consecutive months. That is unusual. The last time total orders, domestic and foreign orders were all up for three straight months together was November 2006 through February 2007 - over a decade ago. And this string builds on a strong base as the August order increase was a gain of 4.1%.

Partly as a result of that string of gains, orders are on a real tear with expansion rates rising sequentially from 12-month to six-month to three-month. However, over three months, domestic orders are topping out at a 15.9% rate of growth, compared to more than double that for foreign orders.

New orders by source

In October 2017, domestic orders increased by 0.4% as foreign orders increased by 0.5% on the previous month. New orders from the euro area were down 1.2%; new orders from other countries increased 1.6% compared to September 2017. The acceleration in German orders is coming largely from outside the euro area.

New orders by sector

Manufacturers of intermediate goods saw new orders fall by 0.4% in October compared with September 2017. The manufacturers of capital goods showed increases of 0.9% on the previous month. For consumer goods, an increase in new orders of 0.6% was logged. The sector order pattern is somewhat reassuring, but the sector sales pattern is not.

Sector real sales trends

Sales trends show a loss of manufacturing sales momentum from 12-month to six-month to three-month. Unlike orders that are ramping up on that same timeline, manufacturing sales post a 2.9% growth rate over 12 months; that slips to 0.2% over six months then remains weak at 0.4% over three months. Consumer goods and intermediate goods sales show some life in their sales as for each the three-month growth rate is above the 12-month growth rate despite some slippage over six months. But for the all-important capital goods sector, growth rates are imploding, falling from a pace of -1.1% over 12 months to -4.5% over six months to a -8.9% pace over three months.

The tailing off of capital goods orders is the part of this report that is not good news. Of course, the steady drumbeat of order advances, especially the consistency of their expansion over the past three months, is very good news. But Germany relies on its capital goods sector and the weakness in sales there is somewhat vexing. Consumer nondurable sales are strong over 12 months, but sales of consumer durables, too, have weakened over six months and flattened out at a puny growth rate over three months.

The fact that so many more sales come from outside the euro area also is not a great sign for euro area growth, but at least Germany is not poaching domestic demand as much from its common market and currency area associates. Is that because they are more competitive or because demand elsewhere in the euro area is weakening? The PMI data do not show that so much, but recent retail sales reports for the EMU have been decidedly weak. I'd have to call EMU growth signals at this point somewhat mixed despite the euphoria I detect in the markets.

In the quarter-to-date, the differences between real orders and real sales trends are particularly acute. On this odd horizon (October sales growth annualized over the Q3 average), total orders are up at a 16.7% pace. Foreign orders are up at a 21.4% pace and domestic orders are up at a 9.7% pace - these are all impressive numbers. But manufacturing real sales are falling at a 10.4% annual rate as consumer goods sales rise at a 9.4% pace and intermediate goods advance at a 4.9% pace. Capital goods sales in the quarter-to-date are collapsing at a 25.8% annual rate- yikes!

On the whole, the expanding orders are good news as is the consistency of the expansion which itself is quite unusual. But the fall off in sales is also something of note. The order strength should trump the sales weakness; however, the sales weakness is so pronounced it can't help but make you wonder how there could be such a sales/order divergence, especially when it is the key capital goods sector is where sales are so weak.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief